A Parkinson’s diagnosis, long Covid or a serious motorway accident? Strokes of fate can hit us all. They’re not easy issues to face, but you need to protect yourself against them and make provisions. We’ve summarised the key information on disability and death protection for you.

Unforeseeable accidents or diagnoses of illnesses can have severe consequences for you and your entire family. Who will pay your mortgage or rent if you are no longer able to work? And who will support you financially if you have a death in the family?

We answer the most important questions concerning disability and death and show you how to protect yourself against them so you can continue to lead as self-determined a life as possible even if you are struck down by fate.

Disability

Disability means that a person is incapable of working for an extended period of time (more than one year). Disability follows a physical, psychological or mental impairment to health. This may have been caused by an accident or illness or may have existed from birth.

What is the difference between incapable of working and disabled?

If a person is no longer or only partially able to carry out their contractual employment duties, he or she is incapable of working. However, this does not necessarily mean that the person is also disabled. Disability arises when a person is no longer able to pursue any occupation, regardless of the previous occupation they learned. If you become disabled following an accident, you are financially covered via your employer as a gainfully employed person. If the cause is illness, the situation is different. In this case, the loss of earned income as a result of serious illness creates an income shortfall.

Accident

If you become disabled as a result of an accident, the OASI/IV and accident insurance will pay for lost income. This is usually 90 percent of your previous salary.

Illness

If you become disabled as a result of illness, your pension fund will pay your pension. As a rule of thumb, pensions from disability insurance and the pension fund cover just under 60 percent of your last income. This results in an income shortfall of around 40 percent

Disability income insurance and disability insurance

An income shortfall due to disability owing to an accident or illness can be covered with disability income insurance. Following the expiry of a waiting period, it will pay you an annuity if you are no longer able to work. Depending on your personal situation, you can choose between a level and a rising annuity. The amount of the annuity payment depends on the degree of disability and the insured benefit.

Self-employed individuals

If you are self-employed and do not belong to a pension fund, you are only entitled to a disability pension under pillar 1 (max. CHF 29 400). The same applies if you have not taken out accident insurance. It is therefore particularly important for self-employed individuals to take out additional insurance. Disability income insurance guarantees a regular annuity.

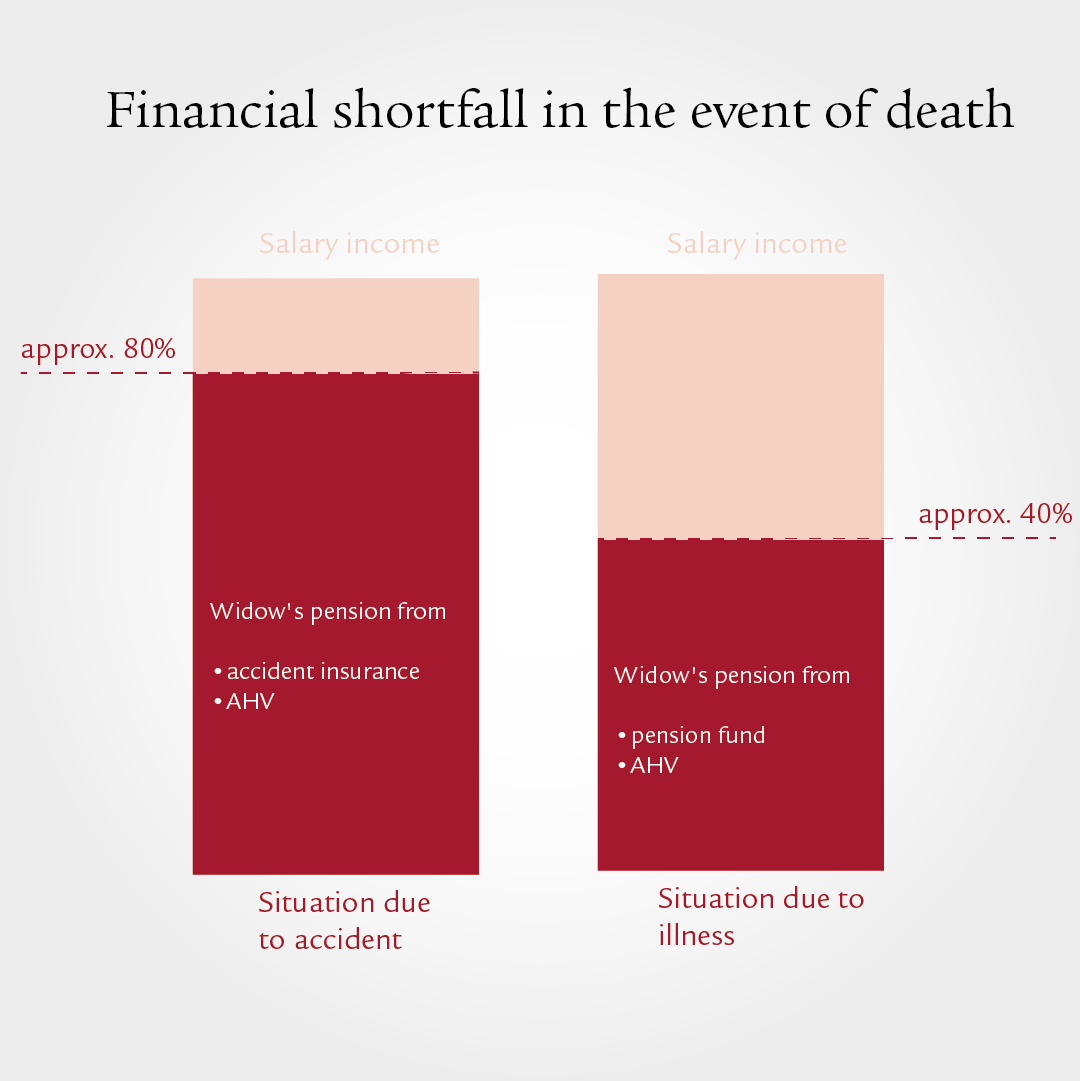

Death

A death is already an enormous burden for a family by itself. The financial consequences come on top of this. First and second pillar pensions are often not sufficient to cover the costs of living and regular fixed costs.

Accident

OASI and accident insurance cover about 80% of the lost salary income in the event of death caused by an accident.

Illness

In the event of death as a result of illness, only around 40% of salary income is covered. As a result, there will be an even bigger income shortfall.

Term life insurance

With term life insurance you can financially protect survivors or other supported persons. In the event of death, the insurance pays a predefined monthly pension or a lump-sum death benefit to the beneficiaries. It is possible to determine individually whether the amount of the lump-sum death benefit remains the same or decreases.

Cohabiting couples

The situation is different for unmarried couples. Here the survivors are generally not entitled to an annuity and depend on supplementary provision. For example, in the case of a cohabiting couple with children, if one of the partners dies, no benefits are paid to the surviving partner.

Obtain advice now

We will help you find the right solution for you.

Swiss Life Protection

Protect yourself or your survivors against the effects of disability or in the event of death.

Term life insurance

With this term life insurance, you determine the amount of the death benefit at the start of the contract. Your beneficiaries will receive this sum when you die. You enjoy life-long death cover.

Swiss Life Dynamic Elements Duo

The savings and risk insurance (pillar 3a/3b) is modular and can be structured in a number of different ways. Thanks to the intelligently linked savings elements it offers an optimum mix of security and returns.

.jpg)