We take a look back at a very good investment year in 2024. Swiss Life’s economists have drawn up five theses for the coming year. We discuss what they mean for the 2025 investment year.

Key points at a glance

A strong US economy combined with simultaneous interest rate cuts by the central banks triggered a rally on many financial markets in 2024. For 2025, Swiss Life’s economists expect that the US economy will continue to grow robustly, continental European central banks will pursue a stimulating monetary policy, inflation will not return to target levels everywhere but will remain under control, the debt economy will continue, and China will still not be a growth engine. These are good prospects for the 2025 investment year for developed equity markets, Swiss real estate and the US dollar.

Our expert assessment is set out in detail below.

Make an appointment for a consultation

Find the optimal solution for your individual investment strategy together with our experts,

CIO Update November 2024

Take a look at the baseline scenario of financial market developments in November with Chief Investment Officer Dr Peter Kaste.

What distinguished 2024?

The key feature of 2024 was the surprisingly robust US economy, which meant that economists’ expectations for US gross domestic product growth had to be continuously revised upwards over the course of the year. This growth was driven by high government spending and strong private consumption. In comparison, the European and Chinese economies performed weakly. However, the prospect of a moderate acceleration in economic activity has saved the European labour markets and the financial markets from disruptions.

The fall in inflation allowed all the major central banks to start cutting interest rates. The Swiss National Bank was the forerunner with its first interest rate cut in March of the year. It also made the biggest interest rate move by a total of 1.25 percentage points over the course of the year to an interest rate of 0.5% as of December. The European Central Bank and the US Fed each lowered their interest rates by 1.0 percentage points to 3.0% and 4.5% respectively at the end of 2024.

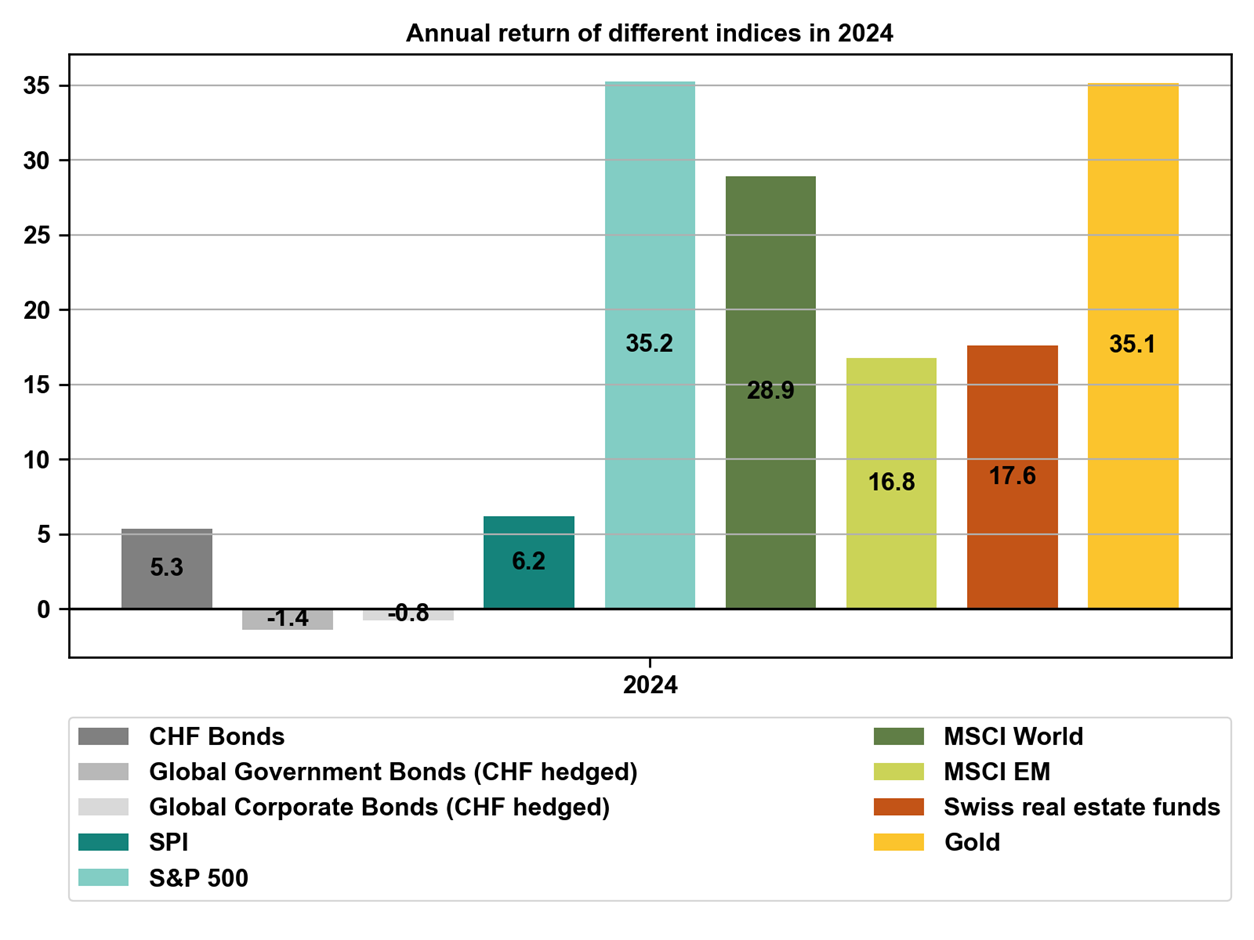

Stronger-than-expected economic growth with simultaneous interest rate cuts by the central banks was grist to the mills of the financial markets. Swiss investors enjoyed very attractive returns on almost all investments, as shown in Figure 1.

Fig. 1: Net total return in Swiss francs of various investments in 2024

With a return of 5.3%, bonds denominated in Swiss francs were among the best bond markets for the second time in a row. Swiss equities (Swiss Performance Index (SPI)) also posted a good return of 6.2%. However, this pales in comparison to the 35.2% achieved by the US equity market (S&P 500). From the perspective of a Swiss franc investor, the latter benefited not only from an outstanding market performance, but also from the appreciation of the US dollar. Swiss real estate funds benefited from falling Swiss interest rates, and also outperformed Swiss equities with a return of 17.6%. Gold enjoyed an exceptionally strong year with a return of 35.1% in Swiss francs.

More than half of the world’s population voted in 2024, with the US election on 5 November 2024 receiving the greatest attention. In our quarterly report at the end of September 2024, we provided an outlook on the US election and stressed that investors should not become nervous. In this report, we highlighted one election scenario and discussed which assumptions would change in our baseline scenario. This was the election of Donald Trump as US President along with a Republican majority in both houses of the US Congress. This election result has become a reality. In a flash commentary after the election, we once again explained what this result means for our economic and financial market assumptions. Our following outlook for 2025 is also shaped by the impact of the policies of the new US administration, which will take office on 20 January 2025.

Five theses for 2025

At the beginning of every year, Swiss Life’s Macroeconomic Research Team led by Chief Economist Marc Brütsch draws up five theses for the coming year. Together with the medium-term scenarios, these provide an excellent basis for formulating the macroeconomic and financial market outlook for the next year.

Thesis 1: “The US will continue to race away from Europe in terms of economic growth”

The US economy has already outpaced the European economy in real terms over the past 20 years. This divergence has even increased in recent years. The new US administration’s more growth-oriented policies will maintain or even widen the growth differential.

Thesis 2: “Continental Europe will transition to an expansionary monetary policy”

Falling inflation and the weak European economy are allowing the European central banks to make further interest rate cuts, especially the ECB. Interest rates will also be lowered in the eurozone to a level that has a stimulating effect on the economy. With a key interest rate of 0.5%, this is already the case in Switzerland.

Thesis 3: “Trump 2.0 involves inflationary elements, but there is no reason to panic”

Several elements of Donald Trump’s political agenda will have an elevating effect on US inflation. The introduction of trade tariffs, for example, will cause a temporary surge in the price of goods. On the other hand, the widening government deficit and restrictive immigration policies will lead to more permanent inflationary pressure. However, Donald Trump knows that US citizens do not like inflation. We therefore assume that the threat of excessive trade tariffs is part of the new US administration’s negotiating tactics, but that the actual tariffs introduced will be lower and more specific.

Thesis 4: “The debt economy will continue to expand”

At 1.83 trillion US dollars, the US had an astonishingly high level of new debt in 2024 considering how well its economy has grown, how low its unemployment is, and the fact that the US is not at war. Given its high spending plans combined with tax breaks, the debt will not shrink under the new US administration. In Europe, France and Italy have such high public deficits that both countries are facing an excessive deficit procedure by the EU. This means they will not be able to increase their new debt, but neither will they want to significantly reduce this due to strong domestic political pressure. In Germany, a new government could increase the federal deficit in order to finance urgent investments in infrastructure renewal and increased defence spending.

Thesis 5: “China’s real estate sector is calming down, but the trade conflict is now causing strain”

China’s growth has been slowed in recent years by the crisis in the real estate sector. The government has now defined guidelines for a package of measures to stimulate the economy. However, this still needs to be implemented. Whereas the real estate sector is starting to stabilise, there is a risk of a trade conflict with the new US administration. China will therefore still be lacking as a growth engine for the global economy, which will also affect export-oriented European companies.

Would you like to know what impact the current market situation might have on your personal situation?

Talk to our investment experts and arrange a free, non-binding initial consultation.

What do these theses mean for the financial markets in 2025?

The central banks will continue to cut interest rates at the start of 2025. However, the persistently robust US economy combined with above-target inflation will force the US Fed to pause its interest rate cuts during the first half of the year. Our economists believe that Swiss inflation will fall to zero in the summer, and the export economy has an interest in a weaker Swiss franc. However, the Swiss National Bank has only 0.5% left to reach a zero interest rate. We do not expect it to go any further and introduce negative interest rates again. The ECB has the most scope for interest rate cuts in order to stimulate the weak European economic growth and help the export economy by weakening the euro. We are therefore expecting larger rate cuts by the ECB in 2025, while the Fed and the SNB will soon pause theirs.

The current yield curves in the Swiss franc, US dollar and euro are too flat and will become steeper in the course of 2025. As interest rate cuts by the SNB and the FED are limited, we expect short-term Swiss franc and US dollar rates to fall only slightly, while short-term euro rates may fall somewhat more sharply. The longer-term interest rates for all three currencies have already risen since the US election in anticipation of an inflationary policy by the new US administration, although the central banks have lowered their respective key interest rates.

Credit spreads on corporate bonds are very low for US dollar bonds and slightly higher for EUR bonds. The credit risk is therefore insufficiently compensated, especially when taking the expected credit defaults into account. We are expecting a slight increase in credit premiums overall for 2025.

The interest rate scenarios above mean that investors will only receive a small return on bonds in 2025, this time including bonds denominated in Swiss francs. However, good-quality bonds serve to diversify equity risks, especially in portfolios with a defensive risk profile.

We expect equities to remain the traditional asset class with the highest yield in 2025. At the same time, we expect US equity markets to again race away from the other markets, even if their returns will not be as strong as in 2024. Your return is no longer being driven by higher valuations, and we are even expecting valuations to fall. Instead, the focus will be on robust earnings growth, which is likely to be more broadly based and no longer solely driven by technology stocks. While European equities are weighed down by a weaker domestic economy and the trade conflict with the US, they should not be written off. Valuations are lower, and expectations are moderate. Export-oriented companies in the eurozone are being supported by a weakening euro, while their Swiss counterparts, especially medium-sized companies, are suffering from the strong Swiss franc. Emerging market equities are being held back by the weak Chinese equity market, but should also generate positive returns.

Swiss real estate funds started to rally in the second half of 2024, driven by lower interest rates. This asset class remains attractive given the continuing low interest rate environment. Real estate is attractive for the diversification of equity risks, particularly for more defensive risk profiles.

Due to the relative interest rate movements of the central banks and relative economic growth, we expect the US dollar to remain strong, possibly also appreciating further against the Swiss franc, as well as a depreciation of the euro.

We already presented these market prospects in our flash commentary following the US elections. Much has already changed since then. However, we expect these movements to continue.

What key figures will we be monitoring?

In order to see whether the economy and financial markets will perform in line with our expectations, we are monitoring the implementation of the new US administration’s political agenda. How quickly and to what extent will it implement these tax cuts and deregulation, and how high will its new trade tariffs be? The inflation trend will be decisive for the central banks’ scope for further interest rate cuts. On the other hand, the labour markets will be central to private consumption. Companies’ order books and capacity utilisation will indicate whether the companies themselves will start to make investments.

What do you need to know as an investor in 2025?

We are expecting 2025 to be another good year for investments.

Nevertheless, as an investor you should always be guided by your long-term strategy. The start of a new year may be an opportunity to review this to see whether it is still in line with your objectives, risk capacity and risk appetite. This is a New Year’s resolution with a lasting effect in any case.

All Swiss Life General Agencies

Find a Swiss Life agency near you

Dr. Peter Kaste

Chief Investment Officer Swiss Life Wealth Management AG

Peter Kaste is the Chief Investment Officer at Swiss Life Wealth Management Ltd. He holds a doctorate in physics and is a CFA charterholder, a member of the Swiss CFA Society, and a lecturer at the Lucerne School of Business. Following his doctorate, Peter Kaste worked as a researcher for several years at École Polytechnique (Paris) and ETH Zurich. He has worked in asset management since 2006. Between 2008 and 2023, he established and headed the Quantitative Research Team at Swiss Life Asset Managers. He has been Chief Investment Officer heading up Investment Management at Swiss Life Wealth Managers since 2024.

Please note: The information provided is for information purposes only and is without guarantee and liability. It does not constitute an offer, investment advice or a recommendation to acquire or sell financial instruments or to conclude any other legal transactions. This article contains forward-looking statements, which express our assessment and expectations at a given point in time. However, various risks, uncertainties and other influencing factors can cause the actual developments and results to differ significantly from our expectations. Past performance is not an indicator of current and future developments and results. Investments in financial products entail various risks, including the potential loss of the capital invested.