Retirement is a significant phase of life – finally, more time for travel, hobbies and family. However, before this phase begins, there is a key question to be asked: should you draw your pension fund savings as a lifelong pension, withdraw them as a one-off lump sum or choose a combination? This decision affects your financial future. We explain the main pros and cons of the various options.

Pension or lump sum – a fundamental decision

When it comes to retirement, you can usually choose between three options for taking your pension fund savings: as a monthly pension, as a one-time lump-sum payment or as a combination of the two. This decision has far-reaching implications – it affects your financial future in old age and cannot be reversed later. The following tips will help you make an informed decision that will give you financial confidence in your later years.

Analyse your financial situation

The first thing you should do is gain an overview of your financial situation after retirement. Start by calculating your projected income and comparing it with your expected expenses. In addition to AHV/AVS benefits, consider other potential sources of income such as rental income, life insurance payouts or investment income.

Think realistically about how much money you will need each month to maintain your desired standard of living in retirement. This step is essential for determining what additional amount you will need from the pension fund.

Would you like a consultation?

Our experts can show you which pension fund withdrawal option best suits your situation.

Need for security vs. flexibility

Whether to choose a pension or a lump sum depends to a large extent on your personal stance.

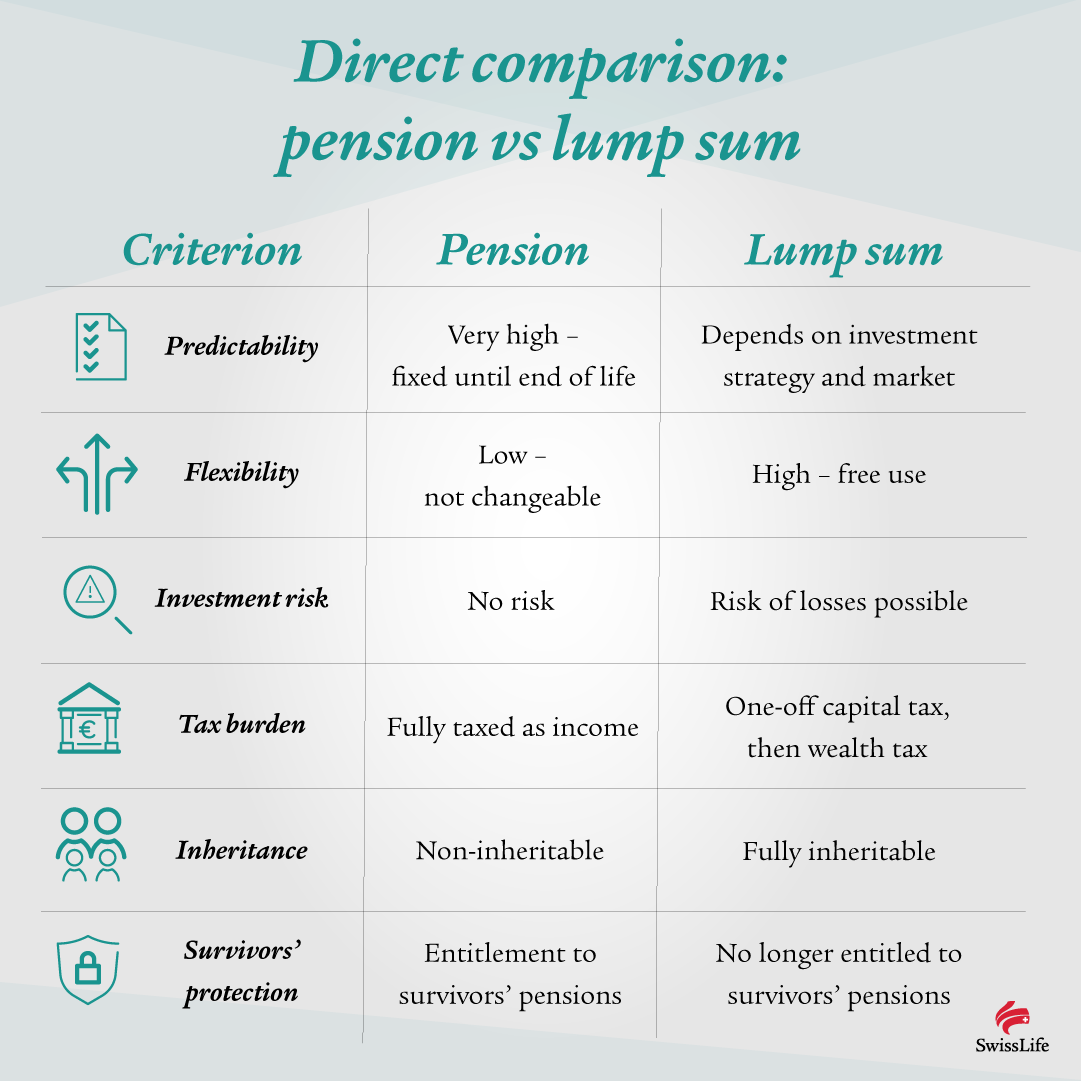

Do you value security and a predictable income?

If so, a monthly pension offers stability for the rest of your life. It provides protection against market risks but does not permit any major one-off payments – for example to pay off a mortgage – and rules out possible stock market gains.

Would you like more control and flexibility?

If so, a lump-sum payment may be the right choice. You decide for yourself how the money is invested or used and can manage it yourself – with the opportunity to achieve higher returns. However, you also bear the risk: if stock market prices fall, your retirement capital may decrease and there are no guaranteed monthly payments.

Tip: Think about how important financial security is to you – and whether you are prepared to take responsibility for managing your assets yourself.

Investment knowledge and risk appetite

If you opt for a lump-sum withdrawal of your pension fund savings, you bear full responsibility for them. The advantages are flexibility and opportunities for higher returns. However, it is important that you are well versed in investing or that you entrust the management of your money to an expert. Without investment knowledge, you risk making poor decisions and incurring losses. Also think about who will manage your finances if you fall ill or are no longer able to make decisions for yourself. In addition, it is only worth investing with a long-term investment horizon. If you need the money in the near future, you should not invest it.

Remember: you determine how much you will need each month to live, including unforeseen expenses. You invest the remaining capital on your own responsibility.

Tip: A lump-sum withdrawal makes sense if you are easily able to calculate your future living requirements and are prepared to accept a certain level of risk. You also need to be actively interested in managing your investments or to have access to expert support in wealth management.

Take tax implications into account

Whether you opt for a pension or a lump sum, the tax implications vary and can influence your long-term financial planning.

- Pension: Monthly pension payments are taxed 100% as income (lifelong).

- Lump sum: The lump-sum payment is taxed separately from other income and at a reduced rate once during the payout year. Thereafter, the capital is subject to regular wealth tax.

A lump-sum withdrawal can be more tax-efficient – depending on your marginal tax rate, place of residence and life expectancy.

Tip: Have your personal tax situation reviewed by a specialist before you make a decision.

Latest information: The Federal Council is planning to increase taxation of lump-sum withdrawals in the near future. If this change is actually implemented, you must take this aspect into account when choosing between a pension and a lump sum and carefully calculate the financial implications.

Would you like a consultation?

Our experts can show you which pension fund withdrawal option best suits your situation.

Property and mortgage

If you own your own home, a lump-sum withdrawal can help to pay off some or all of your mortgage. This reduces monthly costs and improves affordability – an important point, as income is often lower after retirement.

Important: Banks require that the ongoing costs for your home (interest, ancillary costs, maintenance and mortgage repayments) do not exceed a third of your income. A lump-sum withdrawal allows you to reduce your debt and ensure your financial stability in retirement.

Tip: Check early on whether your mortgage will remain affordable after retirement – and whether partial repayment is advisable.

Protect your family

If you want to protect your family financially in the event of your death, a lump-sum withdrawal may be a good idea. The remaining retirement capital is bequeathed and goes to your surviving dependants – for example, your children or your spouse.

The situation is different if you opt for a monthly pension: the pension ends on death and any undrawn capital remains with the pension fund. In this case, your spouse and children receive a survivor’s pension. Note that the orphan’s benefit is paid up to the child’s 18th birthday at the latest – or, in the case of continued initial education or training, no later than the child’s 25th birthday.

Tip: Consider whether you would like to actively protect your family – and whether a lump-sum withdrawal is the better solution.

Tip: Don’t miss the application deadline for a lump-sum payment

You must notify the pension fund in good time if you intend to make a lump-sum withdrawal – up to three years prior to retirement, depending on the pension fund. If you miss this deadline, you cannot apply retroactively for a lump-sum withdrawal.

The amount of retirement savings you can withdraw as a lump sum depends on your pension fund. The law allows at least 25%, but many pension funds also allow 50% or even the entire savings to be withdrawn.

Recommendation: ideally, you should start planning your retirement between the ages of 50 and 55. You should determine when and how to take your pension fund savings no later than five years before you reach the reference age.

What are the advantages of drawing a pension?

- Lifelong security: the pension is guaranteed until the end of your life – regardless of how long you live.

- Predictable income: Consistent monthly amounts make budget planning easier.

- No investment risk: the pension fund bears the risk, not you.

- Simple administration: no overhead for investment decisions or financial management.

- Protection against market and interest rate risks: your payment is not subject to stock market fluctuations

What are the advantages of withdrawing a lump sum?

- High flexibility: you decide how and for what the money is to be used – e.g. investments, major purchases or debt repayment.

- Inheritance: unused capital can be passed on to your heirs.

- Tax optimisation possible: clever planning can make lump-sum withdrawals more tax-efficient than a pension.

- Opportunity for higher returns: if you invest wisely, your capital can increase in value.

- Personalised financial planning: you decide on the time of withdrawal and the amount of the payouts, which gives you greater financial self-determination.

Strike a balance with a combination of pension and lump sum

A combination of a pension and lump sum can be a sensible solution – especially if you want to benefit from both security and flexibility.

Basic principle: cover your essential monthly expenses – such as housing, health insurance, food, transport, hobbies and holidays – with a secure, lifelong pension from the undrawn capital. This covers your basic needs. You can withdraw the remaining capital as a lump sum and use or invest it flexibly – depending on your goals and risk appetite.

Would you like a consultation?

The sooner you begin to plan your retirement, the more options you’ll have.

FAQs on “Pension or lump sum”

This depends on personal factors: security, risk appetite, state of health, tax situation and family plans. A pension offers security, the capital more flexibility.

A rule of thumb says: for a carefree retirement, you should have around 80–90% of your previous income – a combination of AHV/AVS, pension fund and private provisions.

Yes, many pension funds offer a combination. This enables you to cover your basic needs and also use the capital flexibly.

Depending on the pension fund, the application for a lump-sum withdrawal must be submitted up to three years prior to retirement. Anyone who misses the deadline is usually no longer entitled to it.

The lump-sum withdrawal is taxed separately from other income at a reduced tax rate. Wealth tax is due later.

Not usually. Once you have applied for a lump-sum payment or a pension, the decision is final.

Some pension funds allow early withdrawal with reductions. The rules are set out in the pension fund regulations.

When making a lump-sum withdrawal, a broadly diversified and secure investment strategy should be pursued in line with your risk profile and investment horizon. It makes sense to consult an expert.