A suitable occupational pension solution tailored to your needs offers your employees a valuable contribution to their retirement savings and makes your employment conditions more attractive. Certain supplementary benefits in particular will boost your employees’ pension fund. The company itself also stands to benefit. Here we outline the most important points.

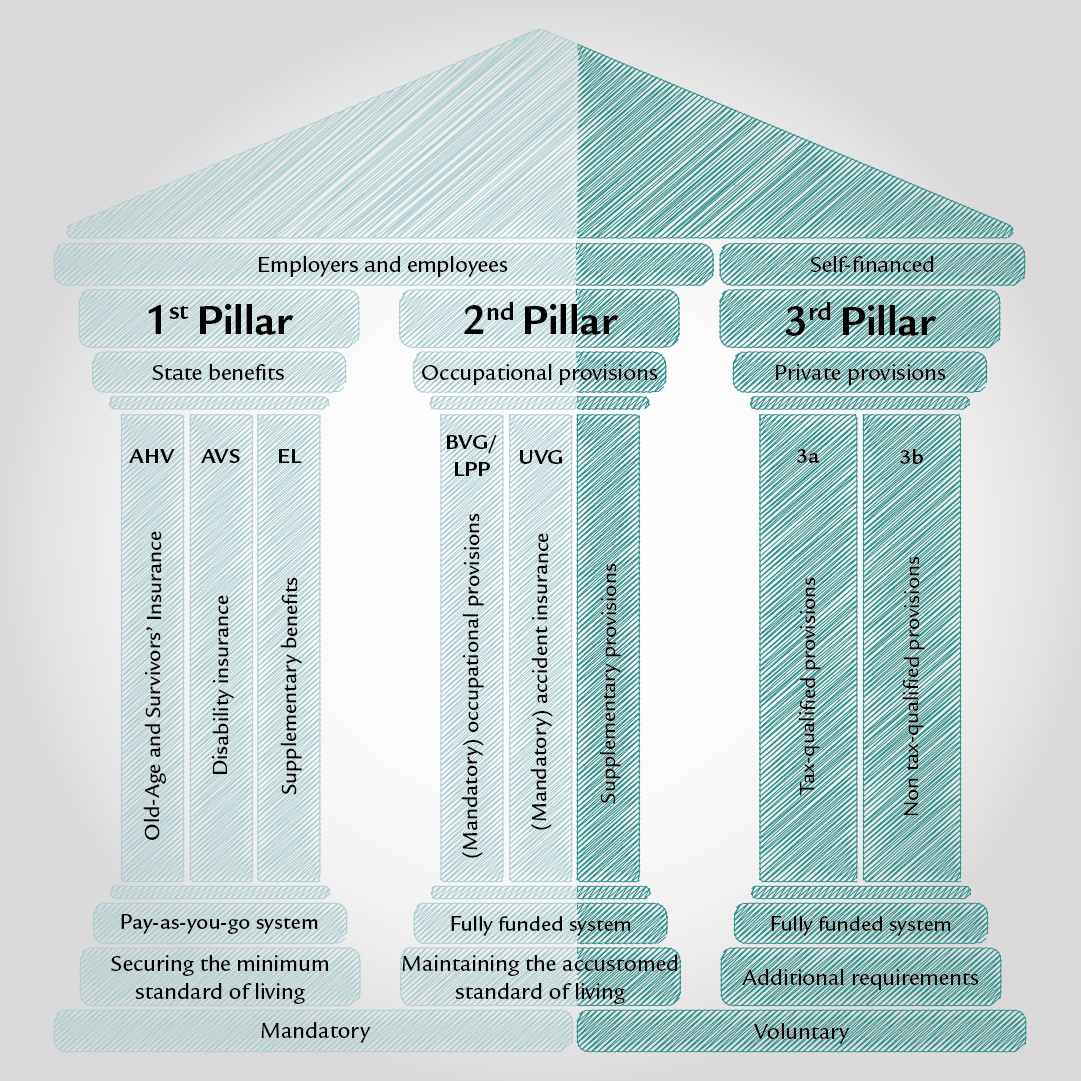

The second pillar of the Swiss three-pillar pension system comprises occupational provisions as defined in the Occupational Pensions Act (BVG/LPP) and accident insurance as defined in the Accident Insurance Act (UVG/LAA). The first two pillars are designed to cover 60% of a person’s income when they retire. Then there is the voluntary, self-financed third pillar.

While the first pillar consists entirely of mandatory benefits, the second pillar offers more flexibility. In addition to the legally stipulated minimum (mandatory benefits), this pillar also includes voluntary – or supplementary – benefits for those insured.

In the supplementary portion, companies can insure salaries higher than those required by law or contribute larger sums, amongst other things. Supplementary BVG/LPP benefits make companies more attractive as employers. This can be an advantage in the event of a shortage of skilled workers, for example.

What benefits are included in mandatory coverage?

The Occupational Pensions Act (BVG/LPP) stipulates who must be affiliated to an employee benefits institution. However, the BVG/LPP only stipulates a minimum, which is the mandatory benefits coverage. Age is one relevant factor in this regard. As a rule, there is a duty to pay contributions to cover the risks of death and disability from 1 January following a person’s 17th birthday. From 1 January following the 24th birthday, contributions must also be paid towards retirement savings. The duty to pay contributions ends when the employee reaches the reference age.

Another important factor is the annual salary. The entry threshold is the annual salary subject to AHV/AVS contributions, which is zweite-saeule-minimum-jahreslohn (as at aktuelles-jahr). There is no legal duty to pay contributions for employees with an annual salary below this minimum amount. The maximum insured annual salary is zweite-saeule-maximum-jahreslohn (as at aktuelles-jahr). Companies can also insure salaries outside this range by means of supplementary benefits (see below).

What companies should bear in mind with regard to BVG/LPP

In addition to age and salary, there are other criteria that should be taken into account when it comes to occupational provisions.

Supplementary benefits: what advantages can I offer my employees?

Many pension funds offer benefits that go beyond mandatory benefits. Companies determine these in conjunction with the pension fund committee. The supplementary solutions are not necessarily the same for all employees. Some are executive solutions (such as the 1e pension plan) and some benefits differ according to age and salary. Larger companies also often offer different plan options. These options allow employees to choose each year whether they wish to voluntarily pay more retirement savings contributions.

Below we describe a selection of current supplementary benefits that will allow your company to create more attractive conditions and your employees to make financially self-determined choices when saving for their retirement:

Insuring salaries outside mandatory benefits coverage

Mandatory benefits cover annual salaries subject to AHV/AVS contributions between zweite-saeule-minimum-jahreslohn (entry threshold as at aktuelles-jahr) and zweite-saeule-maximum-jahreslohn (maximum BVG/LPP salary as at aktuelles-jahr). If a company wants to insure employees with salaries below or above this range, it can do so via supplementary benefits. For employees with low salaries, a company can make voluntary contributions so that money can also be paid into the pension fund of these employees. For employees with salaries exceeding the BVG/LPP maximum, voluntary inclusion of these salary components can be an attractive employment condition.

You can also offer younger employees an advantage by paying contributions into the pension fund before they reach the age of 25.

Lower coordination offset

The annual salary minus the coordination offset produces what is known as the coordinated salary. The pension fund levies savings contributions as well as risk and cost contributions for occupational provisions on the coordinated salary. The coordination offset corresponds to 7/8 of the current maximum AHV/AVS pension, which is bvg-koordinationsabzug in aktuelles-jahr.

The salary is coordinated in the sense that it ensures the correct reconciliation of the first and second pillar pensions. The purpose of the offset is to make sure the pension fund only levies savings contributions – and pays them out after retirement – on the portion of the salary on which the AHV/AVS does not pay a pension.

Companies can reduce the coordination offset or eliminate it altogether to insure a larger portion of the salary. This means that a higher sum is paid into the employee’s pension fund.

Greater employee and employer savings contributions

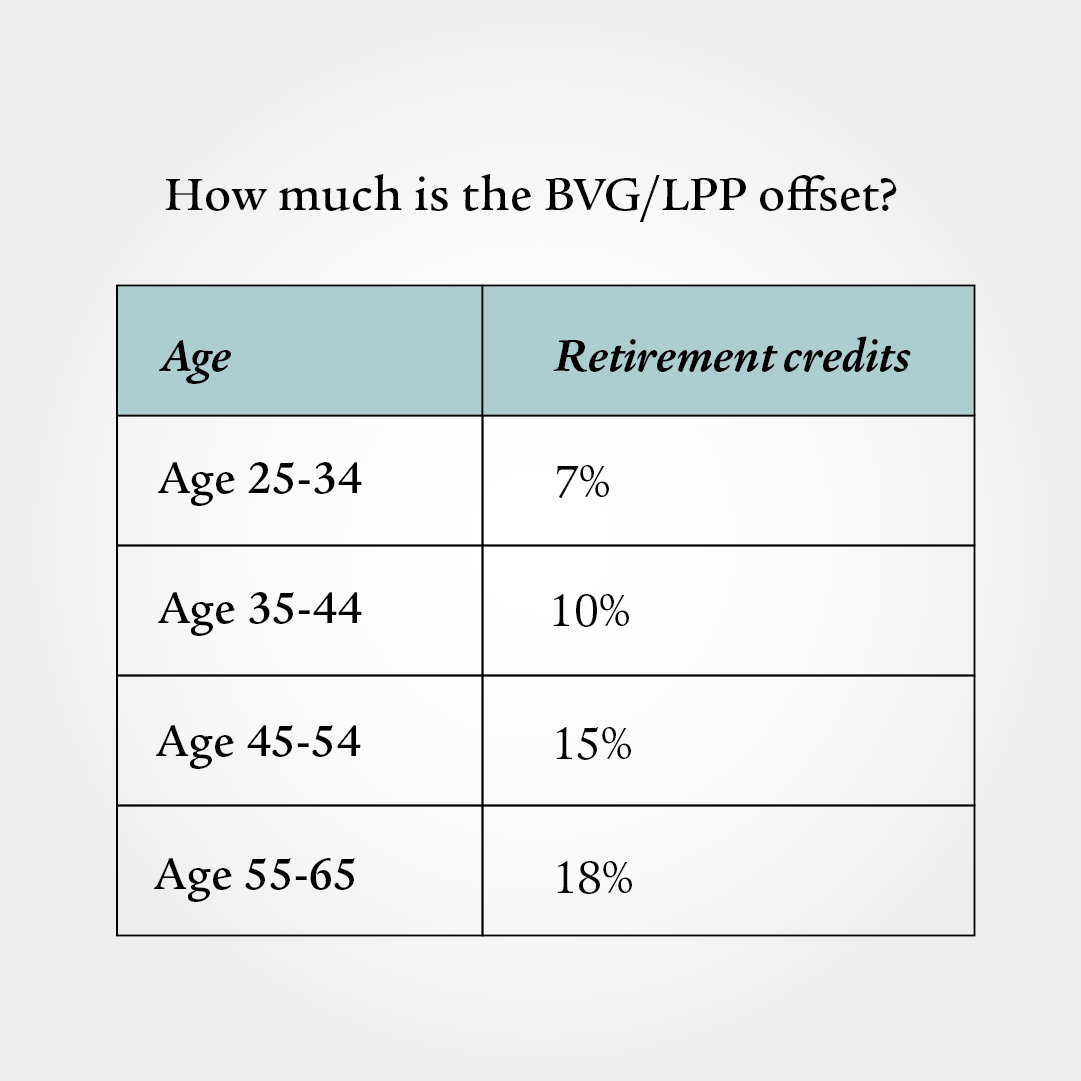

The mandatory savings contributions are calculated by age group and range from 7% to 18% (see table). The employer must pay in at least half of this amount, while the other half is paid by the employee.

Companies can offer their employees more attractive BVG/LPP conditions by paying more than half of the savings contribution. As a result, employees have a lower BVG/LPP deduction and a higher salary paid out while savings contributions remain the same.

Interest rate on retirement savings

The BVG/LPP stipulates a minimum interest rate for savings accumulated under mandatory benefits coverage. In aktuelles-jahr, this is zweite-saeule-mindestzinssatz. However, pension funds often pay a higher rate of interest on retirement savings.

The prescribed minimum interest rate only applies to the mandatory portion of occupational provisions. The minimum interest rate does not apply to supplementary benefits. The interest rate for supplementary benefits is set by the pension funds themselves.

Selection of investment strategy

In some models, you can give employees the opportunity to define the investment strategy for their pension fund assets themselves. Here, employees can decide for themselves whether to take investment risks and how high they should be.

This will result in potentially higher or lower returns. One example of this is the selection of the equity component in the pension fund assets of between 15% and 75%.

Conversion rate for supplementary benefits: what to bear in mind

The minimum conversion rate for mandatory BVG/LPP coverage is prescribed by law and determines the annual pension based on the total retirement savings in the pension fund. This conversion rate is currently zweite-saeule-umwandlungssatz (as at aktuelles-jahr). If someone has accumulated mandatory retirement savings of CHF 200 000 in the pension fund, the annual pension paid out amounts to 6.8% of that amount, i.e. CHF 13 600 or CHF 1 133 per month.

The legally prescribed conversion rate applies to normal retirement age. Pension funds generally reduce the conversion rate if the employee retires early. The number of percentage points deducted depends on the pension fund in question and the model selected.

Like the minimum interest rate, the minimum conversion rate also only applies to mandatory benefits coverage. For the supplementary portion, the pension funds determine the conversion rate themselves using market-based assumptions relating to life expectancy and potential returns.

Splitor uniform conversion rate

Pension funds have the option of applying two different conversion rates to retirement savings:

the statutory minimum conversion rate for mandatory benefits or an individually defined conversion rate for supplementary benefits. In this case, this is referred to as a split conversion rate.

The alternative is the uniform conversion rate. In this case, the pension fund sets a uniform conversion rate that is applied to all retirement savings. This is based on a mixed calculation of mandatory and supplementary savings. This method is only legally permissible if it is ensured that the resulting pension will be at least as high as when applying two separate conversion rates. This is checked by each pension fund using a compliance account. This involves carrying out internal checks to determine whether the statutory minimum benefits are maintained at all times.

What are the tax advantages of supplementary benefits for my company?

Supplementary BVG/LPP benefits are advantageous not only for your employees, but also for you as a company. You can deduct employer contributions to the pension fund from your corporate taxes.

You can increase your employer contributions and benefit from tax advantages in the following ways: you increase the employer’s contribution and pay more than the stipulated 50% of the BVG/LPP contributions, or you pay contributions into the pension fund before the employee’s 25th birthday.

What aspects are relevant to the choice of supplementary benefits?

Some of the features of your company will affect your choice of supplementary BVG/LPP benefits. These features include the workforce and the financial situation of the company. Here’s a selection of the most important criteria:

Age of employees

Are your employees generally young and prefer to be responsible for their own savings? Or are they already older, don’t need the money urgently and are happy to have more pension fund assets available as they approach retirement? Answers to these and similar questions will help you find a suitable pension fund model.

Salary structure in the company

Another key factor is the salary structure in your company. If you generally pay salaries that exceed the BVG/LPP maximum salary, it makes sense to include supplementary benefits so that your employees can make financially self-determined choices about their retirement.

Availability of skilled workers

A shortage of skilled workers in your own company can hamper important business processes. If it offers supplementary benefits in its pension fund, your company is better positioned on the employer market. This way, you stand out from the competition and attract valuable employees to your company.

Frequently asked questions about BVG supplementary benefits

Both these portions of occupational provisions fall within the second pillar. The mandatory portion is also referred to as pillar 2a, while the supplementary portion is referred to as pillar 2b.

Answer: Ensure that you enclose the pension fund benefits with the employment contract. You should also ensure that pension fund information is easily accessible to employees, such as in a personal folder or on the intranet.

The BVG/LPP is the law governing the mandatory BVG/LPP benefits. The pension fund, on the other hand, is the institution that manages and pays out the retirement savings.

A change of pension fund solution may make sense if the age or salary structure of the company alters. The development of a company is also a factor, for example if the company has successfully survived its founding phase and more funds become available.

Following the AHV/AVS reform, the term “normal retirement age” was replaced by the term “reference age”. The reference age corresponds to the age at which the AHV/AVS pension can be drawn without deductions or supplements. This change of term applies to the first and second pillars.

Arrange a consultation

We will advise you individually in a personal meeting. Free of charge and with no obligation.