How can I protect myself in the event of illness or death? And how can life insurance be combined with my retirement provisions? We show you what risks life insurance covers and how you can make sure you are financially protected in terms of life and old age – for more financial self-determination.

Life insurance offers a unique combination of financial security and future provisions, which can be particularly valuable in Switzerland. It is not only a way to hedge risks, but also to accumulate and maintain your assets.

What is life insurance?

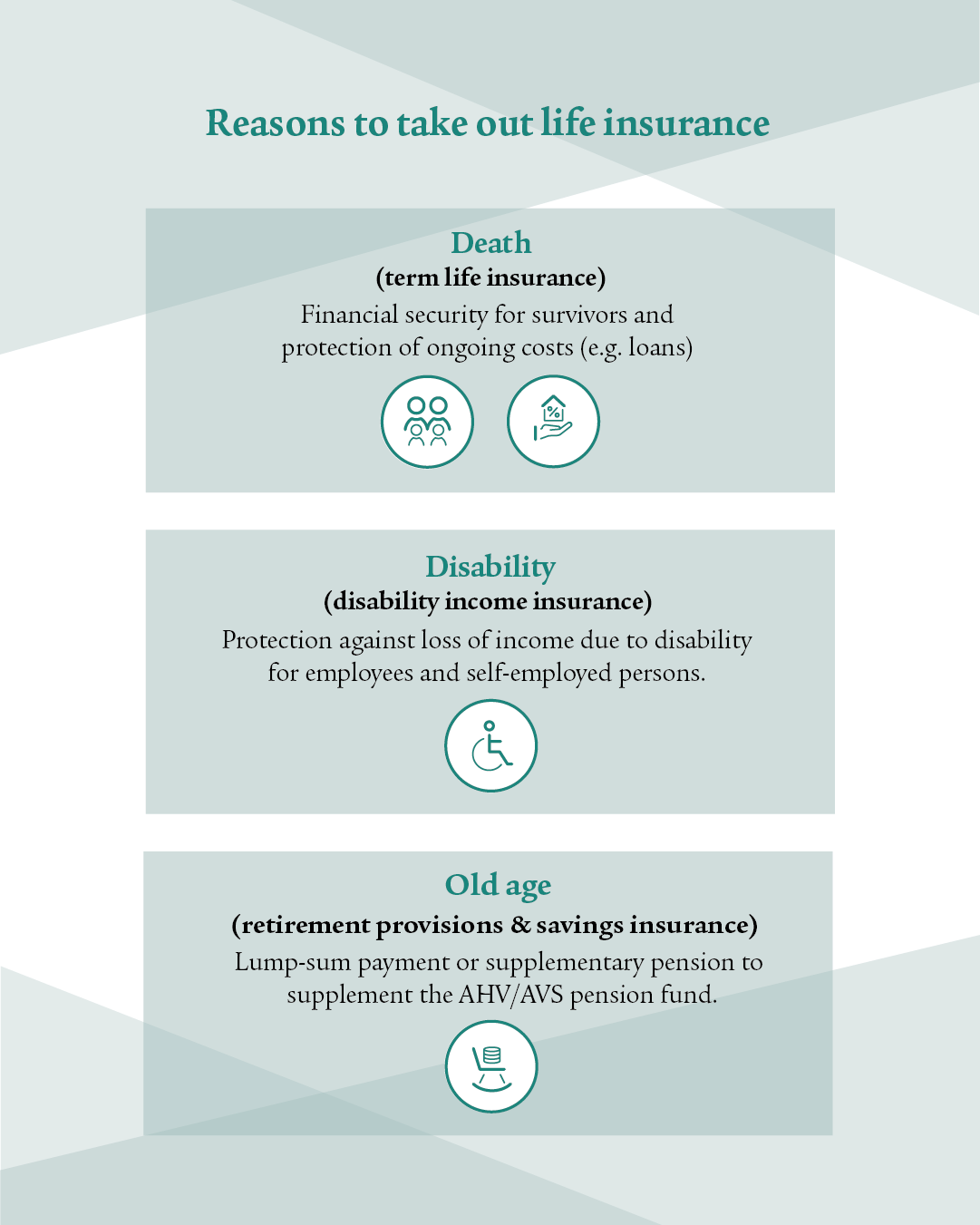

Life insurance is an important part of the third pillar in Switzerland’s three-pillar system. It provides protection against three key financial risks: the financial burden of death, a loss of income due to disability and people’s capital requirements in old age to supplement their retirement pensions.

The principle of life insurance is simple: after taking out a policy, an annual premium is paid over the fixed term of the contract or a one-off premium is paid. In return, the insurance company pays a contractually agreed sum in the event of an insured event.

With term life insurance, this means that the insurance company pays the agreed amount to the survivors in the event of death. This money can be used, for example, to reduce current loans or pay off a mortgage so that the family can continue to live in their own home.

In the event of disability, insured persons can secure their income with disability income insurance. This insurance pays an annuity to supplement first and, where applicable, second pillar pensions.

If additional capital is required in old age, there are life insurance policies that are specifically designed for this purpose. Endowment insurance takes the form of accumulated capital, which is paid out at the end of the contract or earlier, in the event of the death of the insured person.

The three key risks – death, disability and old age – can be covered either separately or in combination with savings insurance.

In addition, there are many life insurance options designed, for example, as savings insurance for a child’s future or as a return-oriented solution for long-term growth opportunities. There are also models that make regular payouts, for example as an additional retirement pension.

Life insurance is part of the third pillar of the Swiss three-pillar system and can be concluded either as a pillar 3a (tax-qualified provisions) or pillar 3b (non tax-qualified provisions) policy. The decision as to which of the two options is best depends on your individual financial life situation and self-determined financial goals.

Questions about life insurance?

Would you like to find out more about life insurance? We will answer your questions.

Reasons for taking out life insurance

Life insurance offers comprehensive financial protection and security in the event of both disability and death. It protects you and your family from the financial consequences of unforeseen events.

With term life insurance, survivors receive support in the event of death to offset the loss of income and to cover ongoing costs (e.g. a mortgage). For example, a young family living in their own home where the father dies suddenly can generally continue to live in their own home with term life insurance because the mortgage can be financed using the money paid out by the life insurance. This is possible if the family has planned their insurance policy accordingly.

Who should take out life insurance?

Taking out a life insurance policy with risk protection provides comprehensive protection and security in various life situations. Below you will find the most important groups for whom a life insurance policy is particularly well suited:

Families with children

- Provides financial protection in the event of a parent’s illness or death.

- Any loss of income can be compensated by the agreed amount, especially if the benefits from the first and second pillars are not enough.

Single parents

- Maintenance for the children in the event of the death of one of the parents

- Securing the retirement provisions of the single parent despite frequent financial constraints

Homeowners

- You are able to stay in your home if the main wage earner is no longer there, meaning you do not have to move house.

- Protects survivors from the financial burdens of mortgage or rental costs if the main wage earner dies.

- It is important for homeowners to adapt their insurance cover in line with the term of their mortgage.

Cohabiting couples

- Provides security to unmarried couples with children without the legal benefits of marriage.

- Offers protection against financial risks caused by the loss of one of the partner’s income.

Self-employed workers

- Offers protection in the event of a lack of occupational provisions (second pillar).

- Protects against a loss of income in the event of disability or death, safeguards the family’s financial well-being.

Single people

- Ensures individual financial stability and independence in the event of disability or other unforeseen circumstances.

- Personal liabilities can be met and standard of living maintained without any financial burden.

Insurance can be flexibly tailored to personal needs.

The best time to take out life insurance

You need to carefully consider whether to take out life insurance; here are some situations in which it is worth considering it:

Early at a young age

An excellent time to take out life insurance is at a young age, for example when you start your professional life. At this age, the contributions are usually lower because the risk to the insurance company is lower. In addition, the insurance can grow over the years and therefore benefit from compound interest.

When starting a family

A good time to consider life insurance is following the birth of a child. Protecting your family in the event of your own death or disability can protect survivors from many financial worries.

When acquiring real estate or taking on loans

If you buy a property or take out a larger loan, it is a good idea to take out life insurance. In the event of an unexpected event, the insurance can be used to settle outstanding debts and avoid financial burdens.

In the event of professional changes or an increase in income

A change of job or a salary increase can also be a good reason to take out life insurance. A higher income can mean it is necessary to insure a larger amount, while at the same time protecting your standard of living.

When planning retirement provisions

Even when you start planning your retirement provisions, you can start thinking about life insurance. Endowment life insurance in particular can be a worthwhile addition to the state and occupational provisions as a way to increase your pension and allow you to lead a financially self-determined life in old age.

The best time to take out life insurance always depends on your individual life situation and personal goals. In general, the sooner the better, as more favourable conditions are often available at a young age and higher levels of insurance can be built up over the long term.

Payout options for life insurance

The payout options for your life insurance vary depending on the type of insurance you select:

Payout of risk insurance

If you have taken out risk insurance, the amount is only paid out if the insured risk occurs, i.e. in the case of death or disability. If no risk occurs, the risk insurance is not paid out.

Payout of endowment insurance

With endowment insurance, you or your beneficiaries receive the benefit either when you die or when the contract expires.

Early payout options

Under certain circumstances, it is possible for a 3a life insurance policy to be paid out early:

- When acquiring residential property for your own use

- On receipt of a disability pension

- Pension fund purchases

- Taking up self-employment

- Emigrating from Switzerland

If you have taken out your life insurance as a pillar 3b policy, you can have it paid out at any time, subject to a few restrictions.

These payout options offer flexibility and security to help you achieve your financial goals and adapt to changing circumstances. Choosing the right life insurance and knowing the payout options are key to getting the most out of a policy.

Life insurance payout

Are you planning to have your life insurance paid out? We would be happy to help ensure this is a smooth process.

Frequently asked questions about life insurance

Choosing the right life insurance is a very personal decision, which depends on many individual factors. No matter whether you live in a family, live your day-to-day life as a single parent, cohabit with a partner, own a property, are self-employed or suffer from a disability – all these circumstances play a role in deciding on the best cover for you.

In a personal consultation, we work with you to develop an individual solution that is tailored to your life situation. Our aim is to offer you life insurance that not only offers you security, but also supports your financial goals.

The monthly costs for life insurance vary. The premium depends on your individual financial situation. Depending on the product, savings premiums are possible from as little as CHF 100 per month.

With a pillar 3a policies, people employed by a company can pay a maximum amount of CHF 7258 per year into life insurance in 2026. Self-employed workers without a pension fund may pay in a maximum of CHF 36'288 in 2026.

There is no maximum amount for premiums in pillar 3b; here you can pay in as much as you want.

As with a pillar 3a pension savings account, with life insurance you can also deduct contributions from your taxable income. This leads to a direct reduction in your tax burden.

By strategically organising your life insurance within the framework of pillar 3a, you not only optimise your retirement provisions, but also benefit from tax advantages.

You can also benefit from tax savings with pillar 3b. During the contract term, the surrender value is taxed as wealth, but the payout is tax-free. With 3a life insurance, the payout is subject to tax, so it is worth having your pillar 3a contributions paid out in several stages in order to reduce your tax burden.

If you die, the sum insured is paid out to the beneficiaries. This process ensures that survivors receive immediate financial support and is an essential part of the protection offered by life insurance.

The choice of beneficiaries for life insurance depends on whether you have opted for a pillar 3a or 3b policy:

In the case of pillar 3a insurance, there are legal requirements as to who is eligible as a beneficiary. As a rule, this is the spouse or registered partner. If you do not have a spouse or registered partner, the statutory intestacy rules apply.

With pillar 3b, you can decide for yourself who should receive the insured sum.

With specified exceptions, 3a life insurance runs until the reference age (normal retirement) is reached or a maximum of five years earlier. However, there are the following exceptions:

- Becoming self-employed

- Financing residential property for your own use

- Repaying a mortgage

- Leaving Switzerland permanently

- Drawing a full disability pension

- Pension fund purchases

With 3b life insurance, you can select the term yourself. As a rule, a long-term horizon is chosen.

Life insurance continues even in the event of divorce. Check whether the beneficiary needs to be changed – particularly in the case of risk insurance.

Note for cohabiting couples:

With pillar 3a, partners can move to second place in the order of beneficiaries after five years of a marriage-like relationship. Specifically, this means that they are the next beneficiary immediately after the insured person’s descendants. In order for this to happen, the marriage-like relationship must be notified in writing to the insurance company.

The importance of good advice

It is worth comparing the various products and benefits available, as they can vary a lot. After getting some initial information, it is advisable to seek advice from a life and pensions specialist. In this way, you can find a pension solution that is ideally tailored to your needs.

With sound advice and careful decision-making, life insurance can be an ideal option for those looking for a tailor-made combination of risk coverage and savings options to secure the financial future of their dependants.

We can advise you

We can help you with all aspects of life insurance. We will work together to find the right solution for you.