There are only a few types of mandatory insurance for start-ups. However, many others are useful in the event of a loss. What types of insurance are mandatory and what risks should you consider when setting up a company? Our overview answers the most important questions so you can safely implement your business idea.

Whether or not insurance is mandatory depends primarily on the legal form of your company. If you are the owner of a sole proprietorship, you are considered self-employed and only have to pay state benefits for yourself, while everything else is voluntary. As the owner of a public limited company (AG) or limited liability company (GmbH), on the other hand, you are considered to be employed, and most social insurance policies are also mandatory for you.

As the majority of start-ups in Switzerland are sole proprietorships, only a few types of insurance are mandatory. Nevertheless, you should carefully consider which risks you want to insure in your start-up, and what you can do without in order to enter into entrepreneurship in a financially self-determined manner.

The following overview shows you which types of insurance are mandatory and what you should consider for your start-up.

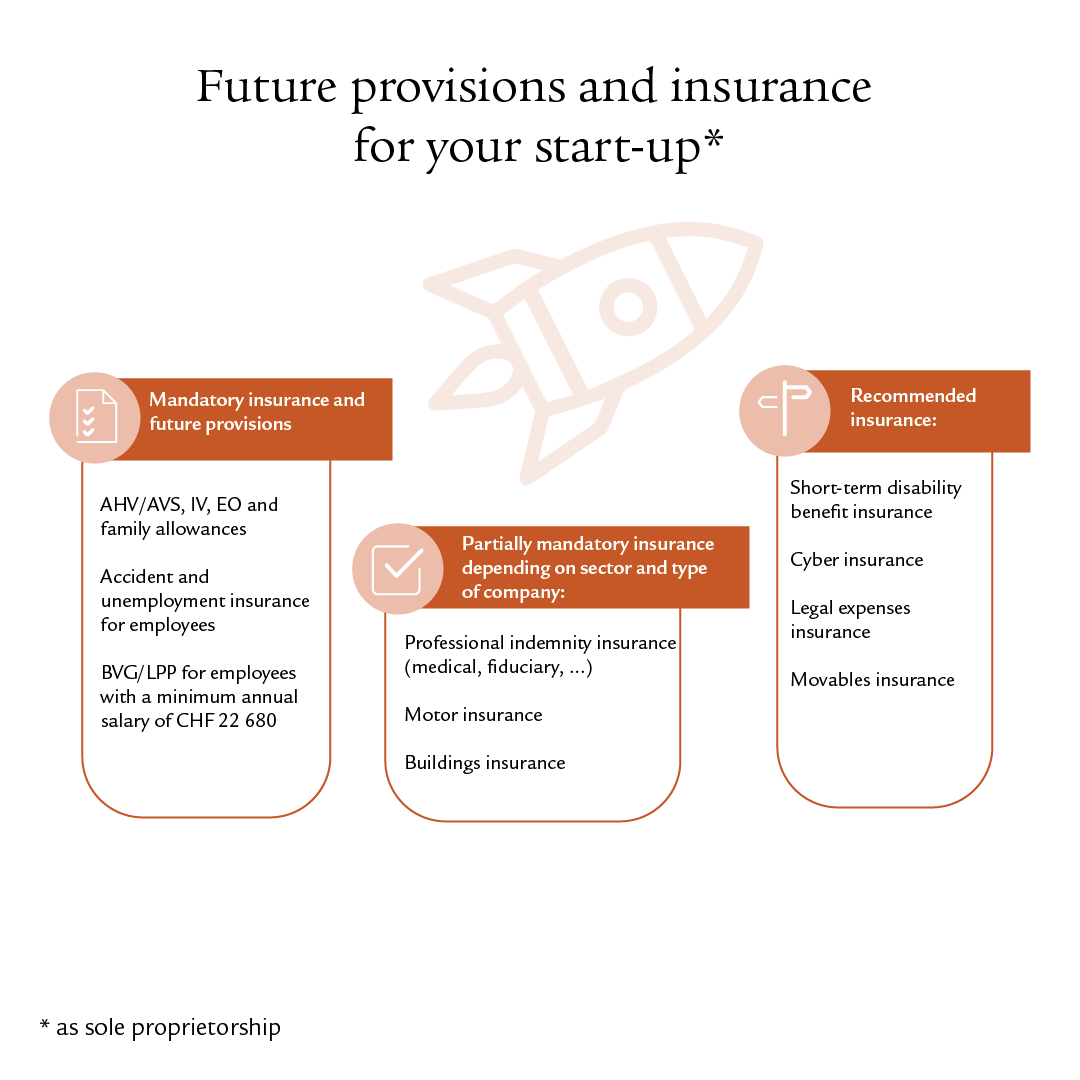

Mandatory and voluntary provisions for the self-employed

1st pillar: AHV/AVS, IV, EO and family allowances

The sole proprietorship is the most popular legal form for start-ups in Switzerland. In principle, only AHV/AVS, IV and EO, i.e. the 1st pillar, and family allowances are obligatory for sole proprietors. Depending on the sector or ownership structure, however, other mandatory insurance may be added; see below for more information.

2nd pillar: pension fund and accident insurance

As the owner of a sole proprietorship, you decide for yourself whether to join a pension fund and take out accident insurance – i.e. the second pillar. Although both are voluntary, affiliation is advisable.

In addition to care benefits and reimbursement of costs, accident insurance also covers loss of earnings due to an accident in the form of a daily allowance or disability pension. Like accident insurance, however, occupational provisions in accordance with the BVG/LPP are highly recommended. They offer protection against the risks of disability and death as well as provisions for old age.

As a sole proprietor without employees, you can voluntarily join a pension fund solution offered by your professional or industry association or, if none exists, the Substitute Occupational Benefit Institution. If you have employees, you must insure them under both the Accident Insurance Act and the BVG/LPP. You can also select the same pension solution for yourself as for your employees.

3rd pillar: private provisions

The 3rd pillar offers further options for providing for old age. If you opt for an insurance solution, you can also include disability income in the event of illness or accident, as well as death cover.

If you are not insured under the 2nd pillar, you can pay up to 20% of your income, up to a maximum of abzug-3a-selbststaendige, into pillar 3a every year. If you join a pension fund, the maximum amount for persons insured under the BVG/LPP applies to you, namely abzug-3a per year (as of aktuelles-jahr). You can deduct the contributions paid into pillar 3a from your income for tax purposes. The payout is then taxed at a reduced rate, separately from your other income.

There are hardly any restrictions on the amount of deposits in pillar 3b. You can also deduct these from your taxable income, but only within the scope of the lump sum for insurance. As a rule, you can reach this amount with your health insurance premiums. However, the payout from pillar 3b is generally tax-free.

The same usually also applies to members of a general or limited partnership as for sole proprietorships. However, as soon as you hire staff, you will also have to take out mandatory insurance for your employees.

Mandatory insurance for employees

Social security administration office: AHV/AVS, IV, EO and family allowances

As an employer, you must register your start-up with the cantonal AHV/AVS administration office or with the administration office of your professional or trade association. You will have to pay contributions to AHV/AVS, IV, EO and the Family Allowances Office.

You and your employees each pay 50% of the AHV/AVS, IV and EO contributions. As the employer, you must pay all the contributions to the Family Allowances Office.

Unemployment insurance (ALV)

Unemployment insurance (ALV) and AHV/AVS contributions are levied together. Here, too, you can deduct half from your employees’ salary. In the event of unemployment, the ALV will pay the persons concerned 70% or 80% of their insured salary.

Important: self-employed persons cannot insure themselves against unemployment.

Accident insurance in accordance with the UVG

Under the UVG, you must insure all your employees against accidents. However, there are differences depending on their weekly working hours: you must insure all employees against occupational disease and occupational accidents (BU), no matter how low their level of employment. Employees who work at least eight hours a week in your company must also be insured against non-occupational accidents (NBU). Contributions for occupational diseases and accidents are borne by the company; non-occupational contributions can be deducted from the employees’ salary.

Following an accident, accident insurance will cover the costs of treatment without any excess or deductible. In addition, it will pay a daily allowance of 80% of the insured salary in the event of incapacity to work, but only after a waiting period of two days and up to a maximum salary of CHF 148 200.

For employees who earn more than this, the employer must top up the daily allowance to 80% of their actual salary and must also continue to pay 80% of the employee’s salary during the waiting period for the UVG daily allowance. As an employer, you can cover this and other benefits in excess of the statutory minimum with UVG supplementary insurance.

Occupational provisions (BVG/LPP)

Pension fund payments are mandatory for employees who earn an annual salary of at least zweite-saeule-minimum-jahreslohn (as at aktuelles-jahr). Occupational provisions through pension funds offer insurance cover in the event of disability and death, while retirement savings are accumulated. Employees receive a pension from these assets in old age, at least part of which they can also draw as a lump sum.

You and your employees each have to pay half of the contributions to the pension fund. Instead of the BVG/LPP minimum, you can offer your employees pension fund solutions that offer better benefits, for example in the event of disability or death. You can also insure salaries above the BVG/LPP maximum of zweite-saeule-maximum-jahreslohn (as at aktuelles-jahr).

Arrange a consultation

We will advise you individually in a personal meeting. Free of charge and with no obligation.

Partially mandatory insurance

Professional and public liability insurance

The two terms professional liability and public liability are often confused, but there are some differences. Public liability insurance is primarily aimed at companies and their employees. Professional liability, on the other hand, protects certain occupational groups and fields of activity.

Public liability insurance is not mandatory, but it makes good sense for many companies. It covers personal and property damage caused by you or your employees to third parties in the course of your business activities.

Professional liability insurance, on the other hand, is mandatory in a few sectors, for example in the fields of medicine, fiduciary, consulting, construction and IT services. For example, it covers losses caused by fiduciaries or lawyers who provide incorrect advice, or treatment errors by medical professionals.

There are many overlaps between professional and public liability. In a consultation, you will find out which types of insurance make sense for your start-up or are even mandatory in the case of professional liability.

Motor insurance

As with private vehicles, motor liability insurance is mandatory for company cars. Without this insurance certificate, you will not be able to register the vehicle in Switzerland. You can also take out voluntary partially or fully comprehensive insurance to cover damage to your company car.

Buildings insurance

It is rather unusual for companies in the start-up phase to own their own commercial property. However, if this is the case with your start-up and you own your property, buildings insurance is mandatory in most cantons. The benefits of buildings insurance and movables insurance (see below) are not clearly defined in some cases. Find out in a consultation what applies to your start-up.

Recommended insurance for start-ups

Short-term disability benefit insurance (KTG)

Short-term disability benefit insurance eases the burden on the company if employees fall ill and are absent for an extended period of time. Although short-term disability insurance is voluntary for Swiss companies, some collective employment contracts require it – so check this in advance. However, short-term disability insurance is always recommended to ensure that your employees are well covered in the event of serious illness, and that your company can continue to operate in a financially self-determined manner. The company and the employees each pay half of the premiums for this insurance.

Without short-term disability insurance you must continue to pay your employees 100% of their salary for three weeks in the first year of service , and for a correspondingly longer period for longer years of service. Depending on your location, the period for continuation of salary payment is based on the Zurich, Bern or Basel scale.

Cyber insurance

From one day to the next, your entire IT system might be paralysed: such a scenario is becoming more and more likely – due to hacker attacks or other criminal cyber activities. Cyber insurance offers protection against cybercrime, which is increasing each year, and covers the costs of third-party and personal damage.

Legal expenses insurance

Disputes with third parties or major losses often require legal support. However, a lawyer can quickly become expensive. Business legal protection insurance generally covers the costs of legal advice, attorneys, litigation and expert opinions. Supplementary cover is also available, depending on your start-up's activity.

Tip: Please note that as a sole proprietor your private legal protection insurance does not cover professional cases. For these, you always need business legal protection insurance.

Movables insurance

Movables insurance protects goods and equipment in your company and insures them against fire, natural hazards and water damage as well as theft. The insurance can therefore be regarded as the equivalent of private household contents insurance. Depending on the provider, it may also be called goods, inventory or commercial property insurance. You can also add business interruption insurance to bridge any interruptions in business activities resulting from losses.

Avoid under-insurance, also known as a shortfall, in terms of you property insurance. This is particularly relevant in the case of partial losses. Here is one example: you own three identical machines with a total value of CHF 90 000. Since you assume that not all three will break down at the same time, you only insure the machines for a total of CHF 60 000. If a machine is damaged, however, due to the two-thirds shortfall you will not receive the full machine value, but only two thirds of it, i.e. CHF 20.000.

Arrange a consultation

We will advise you individually in a personal meeting. Free of charge and with no obligation.