Homeowners currently pay income tax on the imputed rental value of their homes. This will change. In September 2025, the Swiss electorate voted to abolish the imputed rental value. We have summarised the most important facts about the imputed rental value.

What is the imputed rental value?

The imputed rental value is a fictitious rental price for owner-occupied properties. It is based on the assumed revenue that would be generated if the property were not occupied by the owner but rented or leased to another party. This notional revenue is subject to income tax and must be declared in the owner’s tax return. Homeowners therefore pay additional income tax on the imputed rental value. In return, mortgage interest and maintenance costs can be deducted from taxable income, thus reducing income tax.

Would you like a consultation?

We provide comprehensive advice tailored to your goals at a place of your choice.

The vote was adopted: the imputed rental value will be abolished.

What you can expect once the imputed rental value is abolished:

There will no longer be an imputed rental value

People who live in residential property they own will no longer enter an imputed rental value in their tax return in future. This applies to first and second homes.

Deductions can no longer be made

Homeowners can no longer make deductions in their tax return for maintenance or renovation work on their property. In addition, energy-saving and environmental protection measures can no longer be deducted from federal tax. Individual cantons may continue to allow such deductions.

Mortgage interest

Mortgage interest on owner-occupied residential property is no longer tax-deductible: a transitional arrangement applies to first-time buyers: married couples can deduct a maximum of CHF 10 000 in the first year, CHF 9000 in the second year, and so on – the amount is reduced by CHF 1000 a year. The deduction no longer applies after ten years. Half the amount applies to single people.

Second homes

A new property tax has been introduced at cantonal level for second homes. It ensures important tax revenues, particularly in mountain cantons.

How is the imputed rental value calculated?

The imputed rental value is 60–70% of the amount that a tenant would have to pay to rent a comparable property. The imputed rental value is derived from the tax value of the property, which amounts to approximately 70% of the market value. For condominiums, the imputed rental value is around 4.25% of the tax value, while for single-family homes it is approximately 3.5% of this value.

In most cantons, maintenance costs can be deducted from taxable income at a flat rate of 20% of the imputed rental value. If the actual maintenance costs exceed this flat rate, they can be deducted in full – even beyond the imputed rental value.

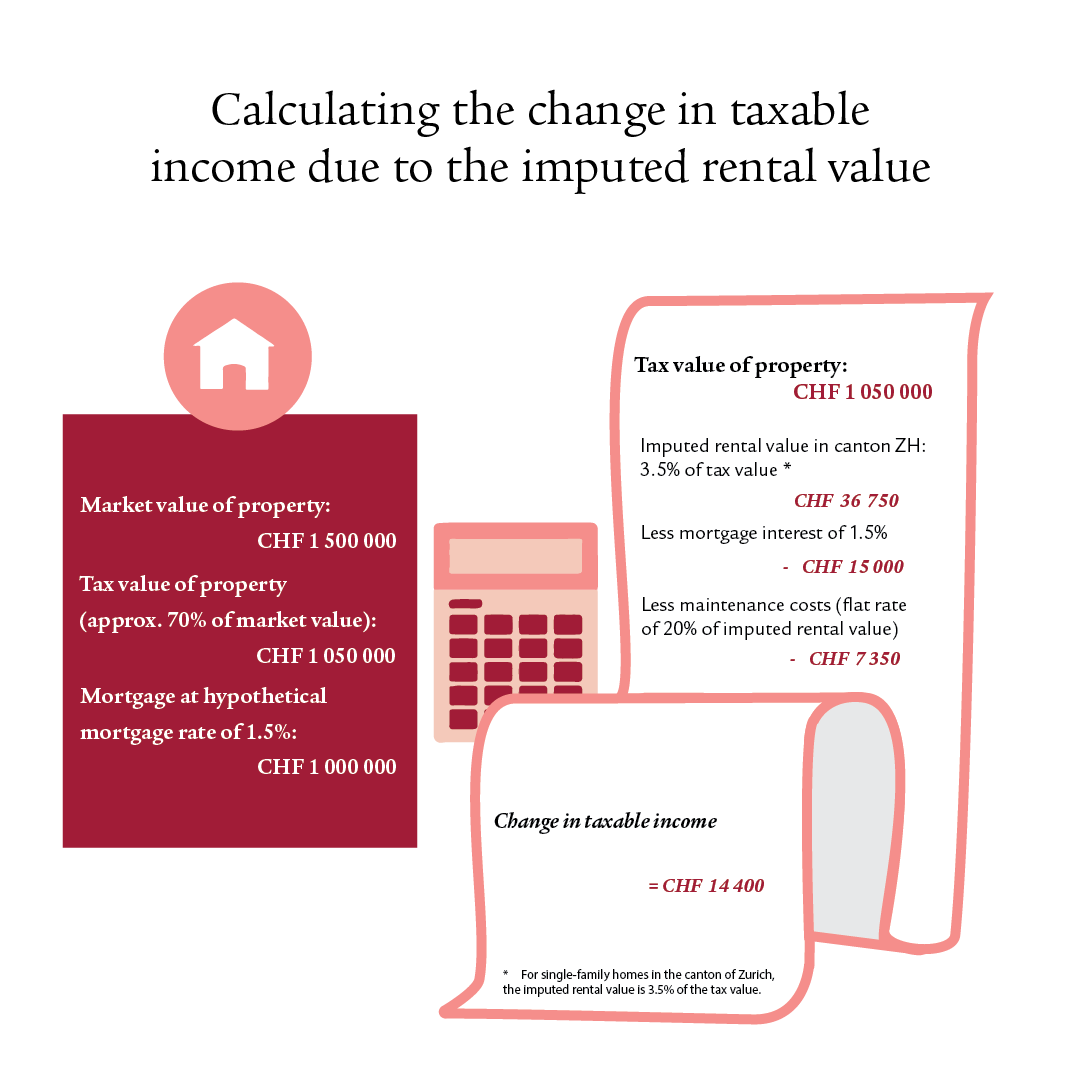

The following example illustrates the calculation of the tax impact:

The illustration shows that the imputed rental value and the other deductions are influenced by various factors. The imputed rental value depends on the property’s tax value and the imputed rental value rate in the respective canton. In most cantons, maintenance costs are calculated by deducting 20% of the imputed rental value. Alternatively, the actual, proven maintenance costs (e.g. repairs, upkeep) can also be deducted. However, these must be documented with receipts and invoices. The deductions may therefore be higher than the flat-rate deduction if the actual costs are correspondingly high.

If interest rates rise, the mortgage interest payable increases, which can also reduce income tax as more can be deducted from taxable income. The extent to which owners would or would not benefit from abolition of the imputed rental value therefore depends on their individual situation.

Once the change in the law comes into force, the calculated CHF 14 400 would no longer have to be taxed as additional income, thus reducing the tax burden in this example by CHF 14 400.

Would you like a consultation?

We provide comprehensive advice tailored to your goals at a place of your choice.