Whether water damage, a broken window or burglary, there are many items in every home that can get damaged. Household contents insurance, adapted to your needs for a self-determined life, protects you against the financial consequences in the event of a claim.

What is household contents insurance?

Household contents insurance protects your personal, movable property such as furniture, clothing, jewellery or electrical appliances. It covers damage or losses arising from fire and natural hazards such as storms, theft or water damage inside the building.

Questions about household contents insurance?

Would you like to take out household contents insurance? We’ll give you individual, non-binding information.

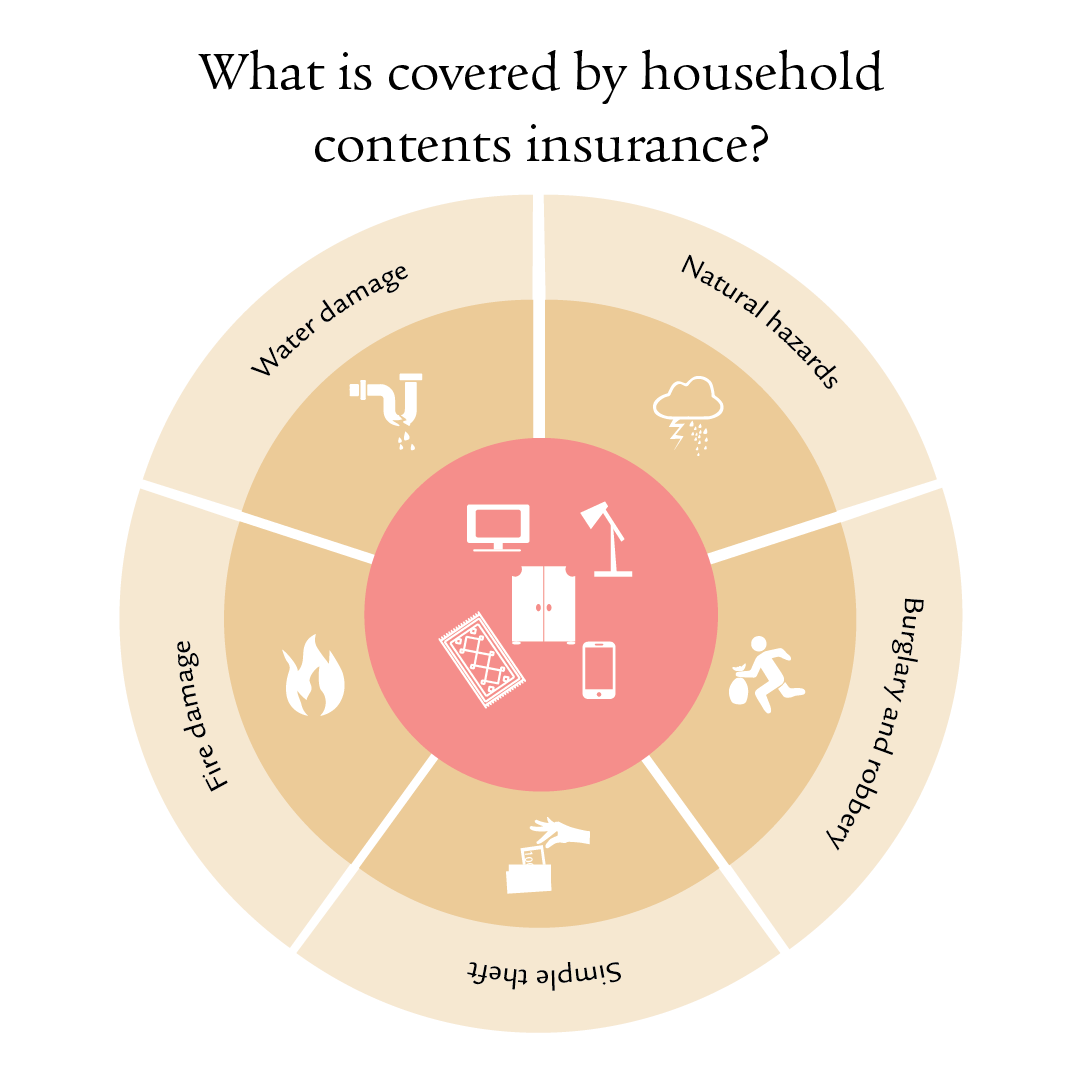

What is covered by household contents insurance?

Household contents insurance covers various damages and losses to your personal property in your apartment or house. Here are the most important things it covers:

- Movable property: all movable items in your home.

- Fire damage: protection against damage caused by fire, smoke, lightning or explosions.

- Natural hazards: protection against the consequences of flooding, storms or hail.

- Water damage: insurance cover in the event of damage caused by leaking water.

- Burglary and robbery: insurance cover in the event of theft by forced entry and robbery if possessions are forcibly stolen.

- Simple theft: cover in the event of simple theft, with supplementary cover outside your home worldwide.

In the event of damage, you will be reimbursed the replacement value / new value of the affected items.

Depending on the insurance package selected, damage caused by you or by people living in the same household is also covered. When taking out the insurance, it is important to check what is included in the policy and what is not. Damage caused intentionally is excluded from the insurance cover. Unintentional accidents, such as breaking your glasses because you accidentally sat on them, are often covered.

Who needs household contents insurance?

Household contents insurance in Switzerland is generally voluntary. However, in some cantons it is mandatory: Nidwalden, Vaud, Fribourg and Jura. In Nidwalden and Vaud, you must take out insurance against fire and natural hazards from the cantonal fire insurance company. In the cantons of Fribourg and Jura, insurance against fire and natural hazards is also compulsory, but you are free to choose the insurance company.

Household contents insurance is generally recommended for both tenants and owners. Unforeseen events leading to the total or partial loss of household contents, as well as additional costs in connection with a claim, can have a serious financial impact if you do not have adequate insurance cover. The costs of replacing items can be significant, especially when high-value goods are involved.

Household contents insurance provides important financial protection and ensures that you do not have to cover all the costs in the event of a claim. This allows you to return to normality quickly and without any financial loss in the event of a claim.

Arrange consultation

Any questions? Our experts will be happy to assist you further.

Special situations

House/flat share

Household contents insurance is also highly recommended if you are living in a house/flat share. It covers all people living in the household, regardless of how the household is made up. This also means that any damage caused by your flatmates is also covered.

Single people

Single people are also recommended to take out household contents insurance. Having optimal protection in place can avoid a major burden in the event of a claim.

Moving house

If you move house, it is important to inform your insurance company of your new address. Moving house also provides a good opportunity to check the value of your household contents and, if necessary, to adjust the sum insured.

Mobile phone

Smartphones are part of your household contents and are therefore insured against theft at home through your household contents insurance. With the “simple theft away from home” add-on, your mobile phone is also insured while on the move, for example if it is stolen while you are having an evening out. Pay attention to the excess amount and how it works, as there may be differences depending on the insurance provider.

Theft

In the event of burglary, robbery or simple theft, personal belongings such as furniture, electronics, jewellery and clothing are insured. A distinction is made between different types of theft:

- Burglary: this involves a person forcibly gaining access to your home and stealing items. An example of this is when a thief breaks a window to get into an apartment.

- Robbery: this form of theft involves the threat or use of violence. For example, a thief could threaten a person with a gun to force them to hand over money or valuables.

- Simple theft: this involves a theft taking place without the use of force; it is neither burglary nor robbery. A thief can easily gain access to your home without using violence or having to overcome obstacles. This would be the case, for example, if an unlocked door or an open window is used.

Basic coverage covers burglary, robbery and simple theft in the home (place of residence of the insured person). Simple theft that takes place outside the home requires additional cover. You should check whether the sum insured is sufficient.

How do I assess the value of my household contents?

To determine the exact value of your household contents for insurance purposes, you can create a detailed inventory. To do this, list every item in your household and note the insurance value / replacement value. In this way, you can calculate the sum insured accurately by adding up all the insurance values. There are also physical lists offered by insurers on which you can enter the inventory.

Alternatively, you can also determine the value of your household contents using a calculation tool. To do this, you first assign your household contents to one of three categories: simple, medium or high-value. For example, high-end furniture, designer clothing or top-end technical appliances fall into the category of “high-quality household contents”. Also take into account the number of people in your household, with children up to the age of 14 counting as “half people”. Finally, you should also include the size of your household and the number of rooms in your assessment.

In addition to these methods, it is advisable to update your inventory list or assessment regularly, especially after major purchases or personal changes in your household. This way you can ensure that the sum insured always reflects the current value of your household contents. It can be helpful to have expensive items valued and keep purchase receipts to prove their cost in the event of damage.

Your insurance advisor can not only help you determine the value, but also help you select the right insurance for your individual needs and circumstances. This way you can ensure that your household contents are adequately insured and that you are sufficiently compensated in the event of a claim. Take advantage of having proper insurance cover so you can count on receiving proper compensation in the event of a claim.

For tech enthusiasts

Laptops, headphones and tablets are also part of the inventory and will be covered in the event of damage.

For fashionistas

Household contents also include shoes, dresses and accessories such as bags and scarves.

For sports lovers

Who lead a self-determined life: surfboards and ski equipment can also be insured.

For bookworms

Who live a self-determined life in literature: All books are also insured and compensation paid for them in the event they are damaged.

Not sure?

We look forward to helping you.

Termination of household contents insurance

Normally, an insurance policy can be terminated at the end of its term. You must always observe the applicable notice periods. These will be listed on your policy.

How much does household contents insurance cost?

The average annual premium for household contents insurance is between CHF 150 and CHF 300 per year. The price depends on a number of factors: the size of your apartment, the value of your household contents and the additional cover requested. The number of people living in your household can also influence the cost.

What is the excess for household contents insurance?

The excess is the amount that you have to pay yourself in the event of a claim. Depending on the insurance policy, it is between CHF 200 and CHF 500.

Frequently asked questions about household contents insurance

Household contents insurance is recommended to protect yourself financially against any damage to or loss of your property.

Household contents insurance is generally voluntary in Switzerland, except in the cantons of Nidwalden, Vaud, Fribourg and Jura, where special cantonal regulations apply.

If the damage was not caused intentionally, household contents insurance also pays out if the damage was your fault. Minor negligence is not a factor, but you should check in your policy whether you are covered for gross negligence. Gross negligence includes, for example, forgetting to put out a burning candle, which then causes a fire.

The sum insured should cover the total value of your household contents in order to ensure you receive sufficient compensation in the event of a claim.

No, household contents insurance is not tax-deductible.

Yes, water damage is generally covered by household contents insurance. However, water damage caused by leaving windows or roof hatches open is not.

As a tenant, household contents insurance protects your personal property inside your rental apartment.

Yes, household contents insurance covers theft. This includes burglary and robbery as well as simple theft at home. You can also take out an add-on to protect yourself against theft outside your home. This protection then applies worldwide. If you have any questions about coverage, it is worth reviewing your personal situation and talking to an expert.

Household contents insurance is generally valid at your place of residence. Different conditions apply worldwide, which is why external insurance is available. External insurance protects your belongings all over the world. However, these items may only be temporarily away from the insured location (place of residence). You should check whether you have an adequate sum insured here.

It is advisable to take out household contents insurance as soon as you move into your first house or apartment and you want insurance cover for all your furnishings and personal belongings. And of course also if your living situation changes.

With household contents insurance you can protect your personal belongings against many risks and you will be reimbursed the original price of the damaged items in the event of a claim.

Household contents insurance also makes sense if you own expensive items or live in an area where there is an increased risk of burglaries, natural disasters or similar loss events.

In principle, all people living in your household are insured. This can include family members, cohabiting partners and roommates.

Yes, the insurance company also has the right to terminate the household contents insurance. This can happen, for example, if the policyholder is defaults on their payments. In addition, the insurance cover expires if reminder periods are ignored, which means that the insurer no longer has to pay benefits in the event of a claim. In addition, following the occurrence of a claim that is covered by the insurance, both parties have an extraordinary right of termination, both for the insurer and for the policyholder subject to the corresponding notice period.

Make a consultation appointment now

Do you have any questions or would you like to take out household contents insurance? We can help. Make an appointment for a consultation:

Swiss Life Home in One

Swiss Life Home In One offers you contents, liability and building insurance. Three types of cover in one contract – and you'll always be optimally insured in and outside your home.