Staying in a rental apartment or buying your own home – what is best for you? There’s no one right answer to this. Both types of housing have their advantages and disadvantages. We will show you the main differences as well as the important factors to consider so that you can be self-determined in choosing what is currently best for your situation.

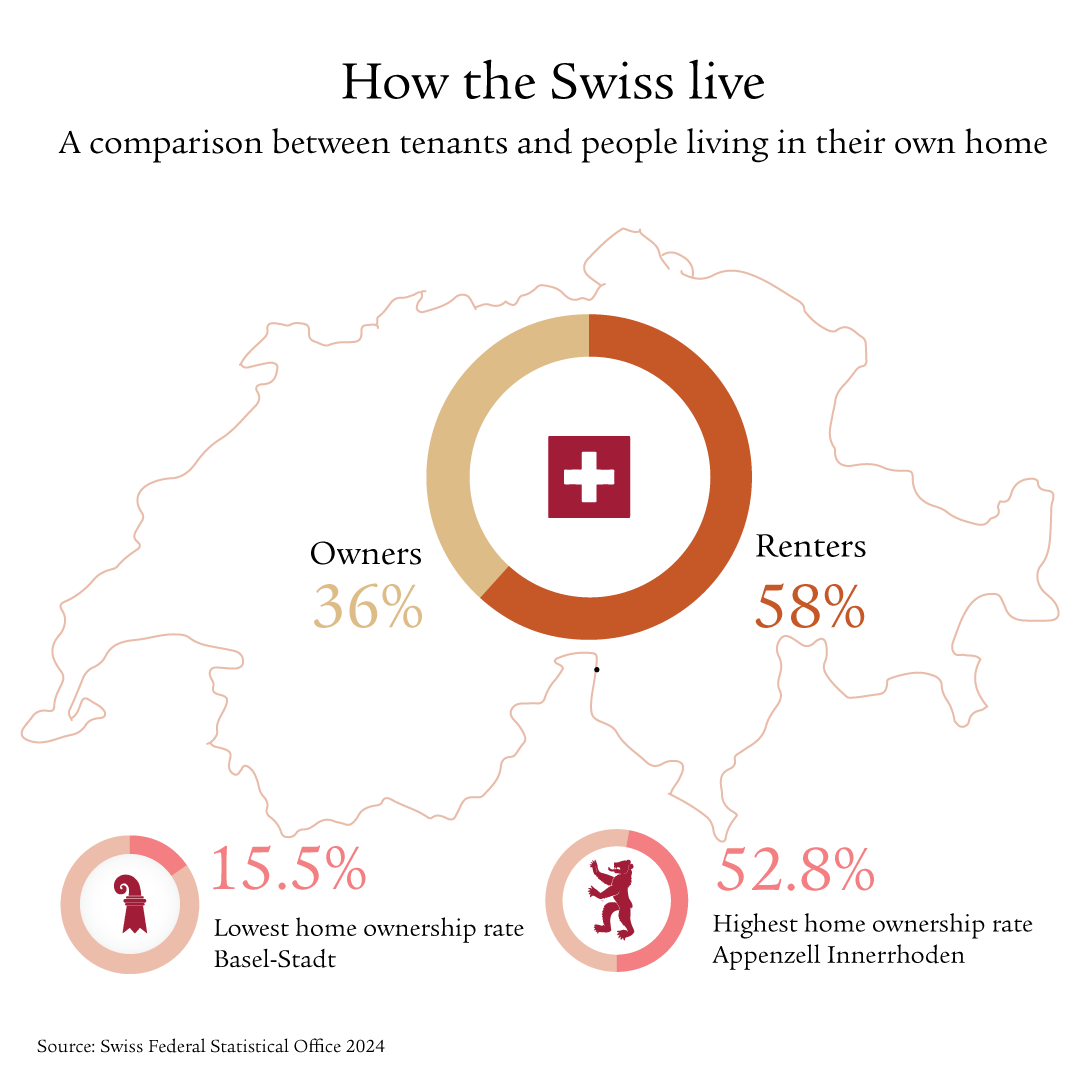

Around six in ten homes in Switzerland are currently rented. The other 40% own their own homes. This relatively even balance shows that there is no one right answer to the question “buy or rent?”. You can find the right answer by understanding the four main differences and making a self-determined decision as to what is important to you.

The four main differences between renting and buying

Financial

Financially free vs. asset accumulation

Freedom

Flexibility vs. freedom of choice

Responsibility

Low risk vs. long-term commitment

Security

Control vs. stability

You are more financially independent when renting than when buying. If you suddenly start to earn less or want to spend more money on something else, you can look for a cheaper apartment. In addition, there are no unexpected costs for repairs or renovations when renting – you do not need to build up any reserves.

Buying usually entails lower costs over the long term than renting the same property. You may need a large amount to invest at the outset, but there is an opportunity for capital appreciation. This means that depending on location, demand and condition, your property will increase in value over the years and you can build up your assets. In addition, owners benefit from attractive tax deductions. And if you later rent or sell your property, you can even generate income.

When renting, you are not tied to a particular apartment or house. You can move spontaneously, to another place, to something bigger or smaller, and you are thus more flexible in how you shape your life. Since you do not need reserves for unexpected repairs, you have more money available for other things.

When buying, you decide for yourself how to design and live in your dream home. A pool in the garden? A new pet? You be as self-determined as you like when making life decisions. You have less freedom when it comes to your mortgage and financial obligations. When you buy a house, you are entering into a long-term commitment. It is usually difficult to get rid of a mortgage at short notice.

When renting, you usually only have a short-term commitment and can react quickly to changes and rising rents. In addition, you don’t have to worry about costly renovations, regular maintenance or administrative matters. You have more time for other things. This means that you take on a low financial risk with a rental contract. For example, if you reduce your level of employment or have less money available for other reasons, you can look for cheaper accommodation.

When buying, you are responsible for maintaining the property and bear a higher financial risk than when renting. With a mortgage, you may face unexpected fluctuations and value losses. In addition, any financial bottlenecks can lead to liquidity risks for buyers more quickly than for tenants. You take out a mortgage over many years and commit to making regular payments.

When renting, you always have your budget under control. You know exactly what your monthly costs will be. Any unexpected costs due to repairs are covered by the landlord. Furthermore, tenants are less affected by economic and financial developments and fluctuations than buyers are.

When buying, you can rest assured that you will be able to live in your own four walls for as long as you want. No one can give you notice. If you have paid off your mortgage, when you are older you won’t even have to pay rental costs. This means you have more money left over and gives you financial security and flexibility.

Having a good feeling and good planning are essential when buying

The decision to own a home is primarily emotional. To make your dream home realistic and sustainable, you should carefully clarify the facts. Having a good feeling is not enough on its own. It should always be backed up by sound planning. You should carefully consider the pros and cons. This allows you to be sure that your decision is not just driven by your emotions, but can actually be put into practice.

How buying a house works

To make your dream of owning your own home a reality, we recommend that you prepare as follows:

- Start planning early

- Determine an optimum asset accumulation strategy to save up as much equity as possible

- Define your budget

- Define affordability based on your budget

- Draw up a financial plan that includes at least 20% equity for the purchase

- Compare mortgages

The 'Best Offer’ is determined on the basis of current interest rate trends and takes into account both Saron and fixed-rate mortgages.

Move closer to your dream of owning your own home

We will provide personal advice and help you plan your finances. Arrange a non-binding, free-of-charge consultation with our advisory team.