The mandatory BVG/LPP benefits coverage determines who has to pay into the occupational provisions and the level of benefits and contributions according to age and salary level. However, companies can insure benefits in excess of mandatory benefits coverage and thus create more attractive conditions. We answer the most frequently asked questions about BVG/LPP and explain the most important terms.

How do occupational provisions work?

The abbreviation BVG/LPP stands for "Federal Act on Occupational Old Age, Survivors' and Invalidity Pension Provision". Together with accident insurance in accordance with the UVG, this forms the second pillar of the Swiss pension system. The aim of occupational provisions, together with the first pillar, is to enable people to maintain their accustomed standard of living in an appropriate manner. Occupational provisions, together with the AHV/AVS, are intended to provide insured persons with 60% of their previous salary after retirement.

All pension funds must meet the mandatory BVG/LPP benefits coverage. The relevant provisions are set out in the law. However, many pension funds also insure supplementary benefits. These are governed by the rules in the regulations of the respective pension fund.

Persons who reach retirement age are entitled to retirement benefits. Pension funds usually pay this out in the form of a monthly pension. The amount of this pension is determined by the conversion rate (see below). Instead of drawing a pension, pensioners can also have their retirement savings paid out as a lump sum or opt for a combination of a lump sum and a monthly pension in order to remain financially self-determined after retirement.

In addition to retirement benefits, occupational provisions also include risk benefits. These take effect in the event of disability or death. In the event of disability, for example, there is a disability pension as well as a children’s benefit for minors and children in education up to the age of 25. The pension fund is also involved in the event of death and pays a widow’s or widower’s pension and orphan’s benefit. Depending on the regulations, pension funds also pay a lump-sum death benefit.

Questions on occupational provisions?

Let our experts provide you with personal and non-binding information at a consultation.

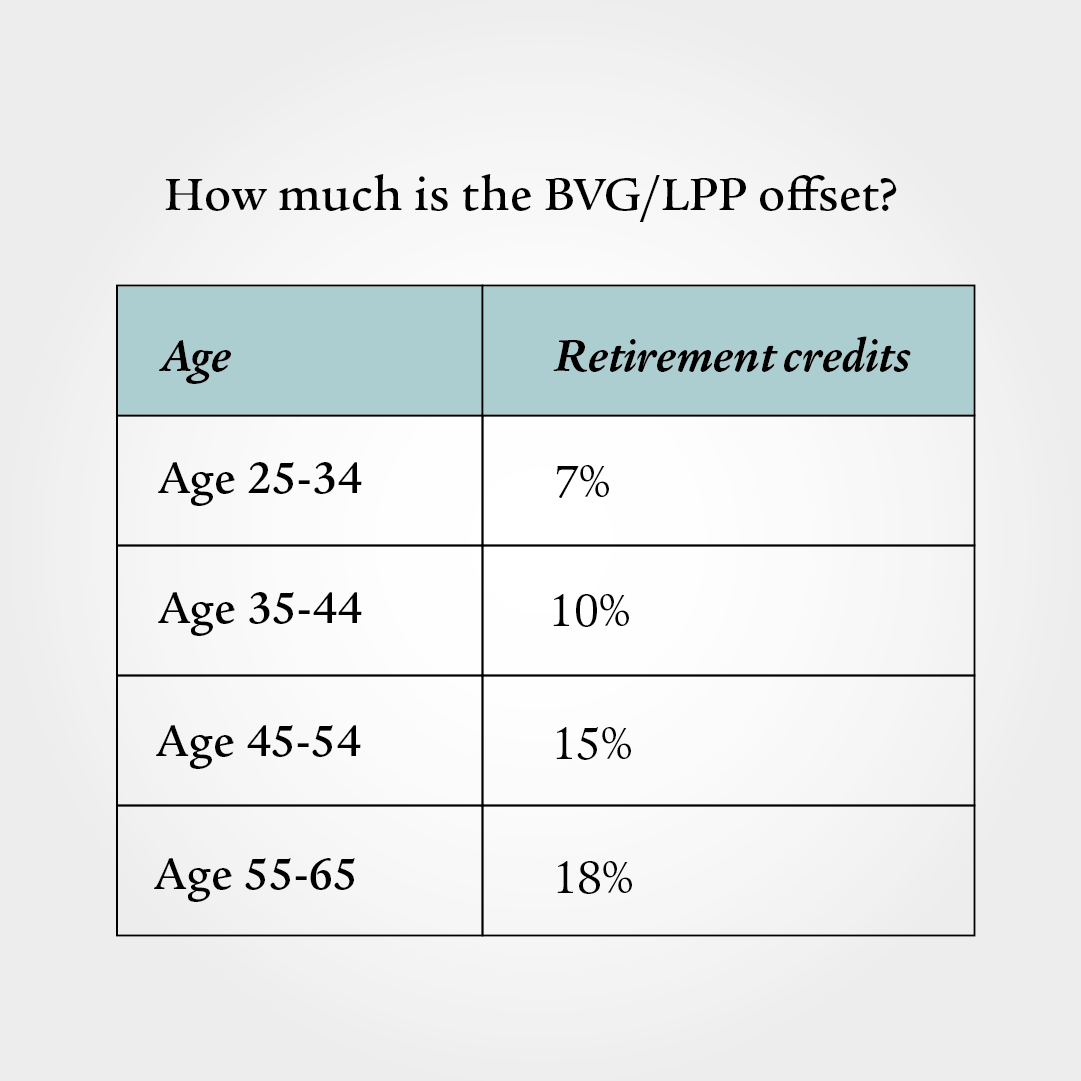

How much is the BVG/LPP deduction by age?

The legally prescribed portion of occupational provisions, the BVG/LPP mandatory benefits coverage, generally applies to all employees who earn an annual salary subject to AHV/AVS contributions of at least zweite-saeule-minimum-jahreslohn (BVG entry threshold, as at aktuelles-jahr).

The applicable maximum AHV/AVS annual salary for mandatory benefits is zweite-saeule-maximum-jahreslohn (as at aktuelles-jahr). A company can voluntarily insure higher salaries in its supplementary benefits. Not only salary, but also age and employment type play a role in determining the obligation to pay BVG/LPP contributions.

The following table lists the BVG/LPP savings contributions by age. The employer must pay at least half of the contribution, but may voluntarily assume a higher amount. As a rule, the employer and the employee each pay half of the BVG/LPP contribution. For BVG/LPP solutions with higher benefits, both the employer and the employee pay higher savings contributions.

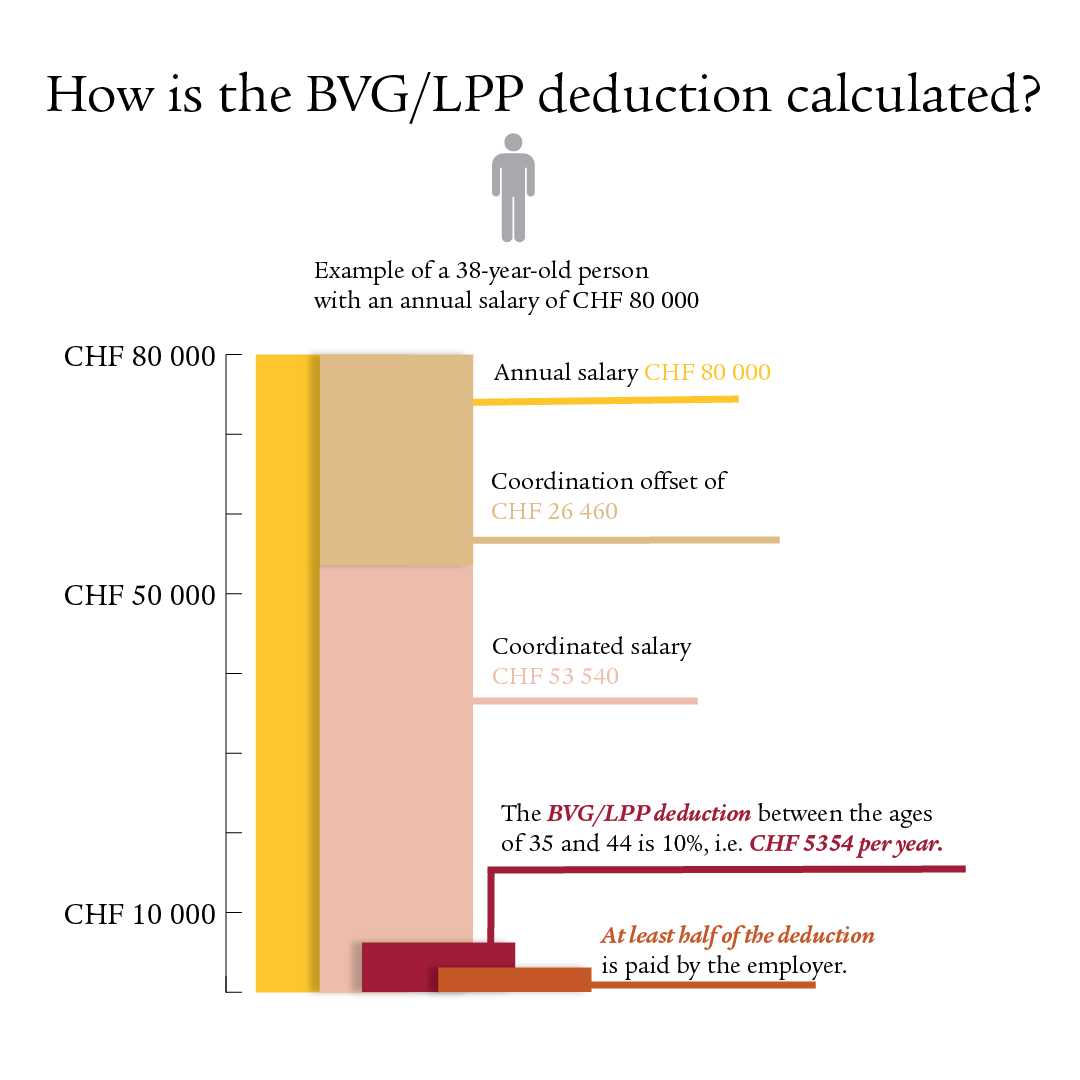

How is the BVG/LPP deduction calculated?

The annual salary subject to AHV/AVS contributions minus the coordination offset gives the coordinated salary. Of this, the BVG/LPP contributions are levied in accordance with the above table and divided between the employee and the employer.

The coordination offset is based on the AHV/AVS retirement pensions and is bvg-koordinationsabzug (as at aktuelles-jahr). The aim of the coordination offset is to coordinate 1st and 2nd pillar pensions.

Example: A 38-year-old person earns an annual salary of CHF 80 000. Minus the coordination offset of CHF 26 460, this results in a coordinated salary of CHF 53 540. Contributions of between 7% and 18% are levied on this salary. For a 38-year-old person, that would be 10%, or CHF 5354 per year. The employer and the employee each pay half of this amount. BVG/LPP contributions are generally deducted from the monthly salary and can be seen in the salary statement.

What applies to the 13th monthly salary?

The 13th monthly salary forms part of the annual salary and is therefore taken into account in determining whether or not the BVG/LPP entry threshold has been reached. Companies must therefore also take the 13th monthly salary into account when calculating their BVG/LPP deductions. The same applies to any bonuses.

Special features of hourly pay

Employees on hourly pay are subject to the same rules as employees on a fixed monthly or annual salary. However, the settlement is more complex, as it is not always clear in advance how many hours a person will work or how much the salary will ultimately be.

As a rule, it is possible to extrapolate whether employees reach the BVG/LPP entry threshold or not. For companies and employees, it is best to make a monthly BVG/LPP deduction for hourly pay.

Questions on occupational provisions?

Let our experts provide you with personal and non-binding information at a consultation.

From what age is the BVG/LPP deduction made?

If employees earn an annual salary above the entry threshold, they are insured against the risks of disability and death from 1 January following their 17th birthday. From 1 January following their 24th birthday, retirement savings will be added with the savings contributions described above.

Who is exempt from the BVG/LPP obligation?

The following groups of persons are excluded from mandatory benefits coverage:

- Employees who earn less than zweite-saeule-minimum-jahreslohn per year (as at aktuelles-jahr)

- Employees until 31 December following their 17th birthday

- Employees with a fixed-term employment contract of maximum 3 months

- Self-employed persons

- Employees who work part-time for a company and who are already subject to the BVG/LPP as their main occupation

- Employees who work part-time for a company and are self-employed as their main occupation

- Persons who are at least 70% disabled according to the disability insurance

- Family members working on their own farm

For whom are occupational provisions voluntary?

Self-employed persons can insure themselves voluntarily in accordance with BVG/LPP. This is possible with your employees’ pension fund, an industry fund or the foundation for the BVG/LPP contingency fund.

Employees with several minor part-time jobs can also take out insurance if their total annual salary is above the entry threshold. This is possible with an employer’s pension fund, if permitted by the regulations, or with the foundation for the BVG/LPP contingency fund. Employers are then obliged to pay the BVG/LPP contributions on a pro rata basis.

What are the different BVG/LPP solutions?

The savings accumulated in the pension fund over the years depend not only on the contributions of employees and employers. The return on the capital invested also makes an important contribution. Pension funds offer a range of solutions:

Full insurance – security-oriented: If a company does not want to take risks, it opts for full insurance. Full insurance guarantees 100% security for the retirement savings and the interest on them. A shortfall is not possible. In accordance with provisions, savings can “only” be invested with a conservative investment strategy (equity component of less than 5%). This may lead to a lower return than with a semi-autonomous solution.

Semi-autonomous solution – returns-oriented: With a semi-autonomous solution, companies have the opportunity to play a role. They decide whether to take on a low or high investment risk. With a higher investment risk, there is an opportunity for higher returns. However, both companies and employees bear the investment risks.

How can companies optimise their BVG/LPP solution?

All companies must insure the legally stipulated BVG/LPP minimum benefits. In order to offer their employees more attractive conditions and financial self-determination, they can insure better benefits under supplementary benefits. Here are two examples:

Insure higher salaries: According to the BVG/LPP, annual salaries of up to zweite-saeule-maximum-jahreslohn must be insured minus the coordination offset of bvg-koordinationsabzug (as at aktuelles-jahr). However, companies can also insure salary portions exceeding the BVG/LPP maximum salary on a voluntary basis. The same applies to salaries below the entry threshold; companies can also insure them voluntarily in the BVG/LPP.

Extended coverage for unpaid leave: Companies can voluntarily continue to pay into their employees’ occupational provisions if they are taking a sabbatical or other unpaid leave.

Frequently asked questions

The conversion rate determines the annual pension based on the accumulated retirement savings. For mandatory benefits coverage, it is 6.8% (as at 2025). Example: A person has accumulated retirement savings of CHF 250 000 in their professional life. With a conversion rate of 6.8%, this results in an annual retirement pension of CHF 17 000. Most pension funds set a lower conversion rate for supplementary benefits (5% or less).

The coordination offset is used to harmonise the 1st and 2nd pillars. The deduction corresponds to the portion of the salary which is normally covered by the AHV/AVS (first pillar). To avoid duplication of coverage, no 2nd pillar contributions or benefits are provided for this portion of the salary.

The coordination offset is 7/8 of the maximum AHV/AVS retirement pension. If there is a cost-of-living adjustment of AHV/AVS pensions, the coordination offset also changes.

The minimum interest rate on the assets accumulated under occupational provisions for BVG/LPP mandatory benefits coverage is set by the Federal Council. It is currently 1.25% (as at 2025). For the supplementary portion, the pension funds set the interest rate themselves and often set it lower.

The BVG/LPP is the law which sets out the conditions for occupational provisions described above. The pension fund is the organisation that implements the law and manages the members’ contributions and assets. Colloquially, the two terms are often used synonymously.

Obtain advice now

Provide for every eventuality. Find the disability insurance that best suits your needs.