If you have a business idea, you want to found your own start-up straightaway. However, it is a good idea to research the key steps for becoming self-employed and to give them some thought. This includes financing your start-up, choosing its legal form, as well as pensions and insurance.

1. Your business idea

Company founders often take their first step towards independence long before founding a company – when they come up with their business idea. In the beginning, this often only exists in their head or in a note jotted down on their smartphone.

You need to take your basic idea, work on it and formulate it specifically so that it is competitive. You should start talking to people about it as soon as possible. This will often provide you with some valuable tips that you otherwise would not have thought of. Perhaps you know someone who has already set up a business and could pass on what they have learned.

2. Business plan

The foundation for a successful start-up is your business plan. This serves as a guide for bringing your business idea to the market. In the initial phase, it also helps to present your idea to investors – whether banks and angel investors, or a larger target audience in the case of crowdfunding.

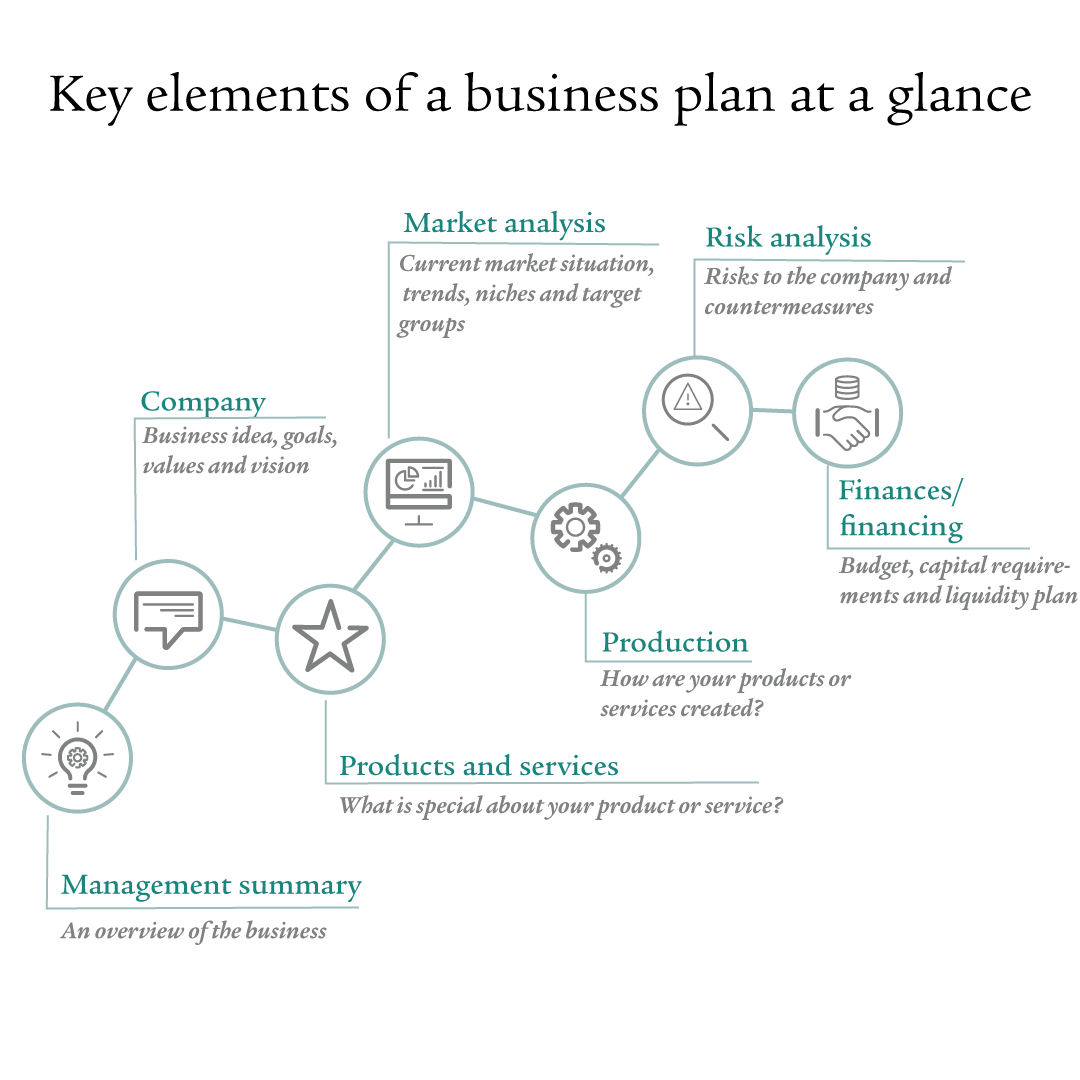

Key elements of a business plan (extract):

- Management summary: record the most important points about your idea here so as to convince readers that they should read the entire business plan.

- Company: present the goals, values and vision for your project here.

- Products and services: answer the question “what makes your product special?”.

- Market analysis: current market situation, trends, niches and target groups

- Production: summarise how your products or services are created.

- Risk analysis: what are the risks relevant for your company? Describe any countermeasures, such as prevention or insurance.

- Finances: outline your budget, capital requirements and liquidity plan and show that you will generate sufficient returns and how you will do so.

The “Finances” aspect in particular shows whether going through with your business idea is financially viable. The business plan may therefore also protect you from failing.

3. Financing for your start-up

Being self-employed does not necessarily mean being self-financed. Financing depends not only on the size of the investments you are planning, but also on equity capital and your own risk appetite. In order for company founders to be financially self-determined in shaping the later phases of their company, investors are often needed at the outset.

Typical financing options for start-ups:

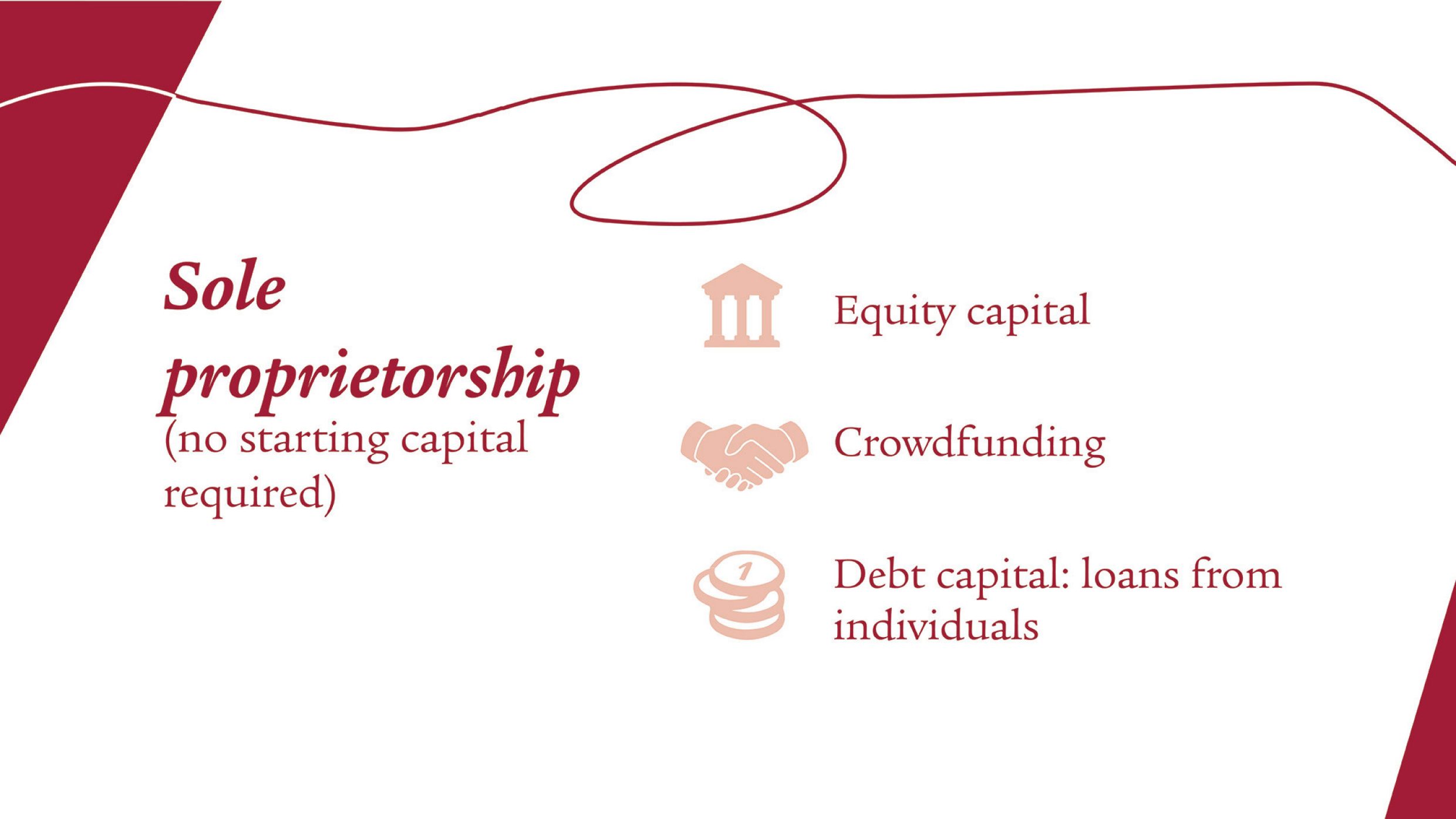

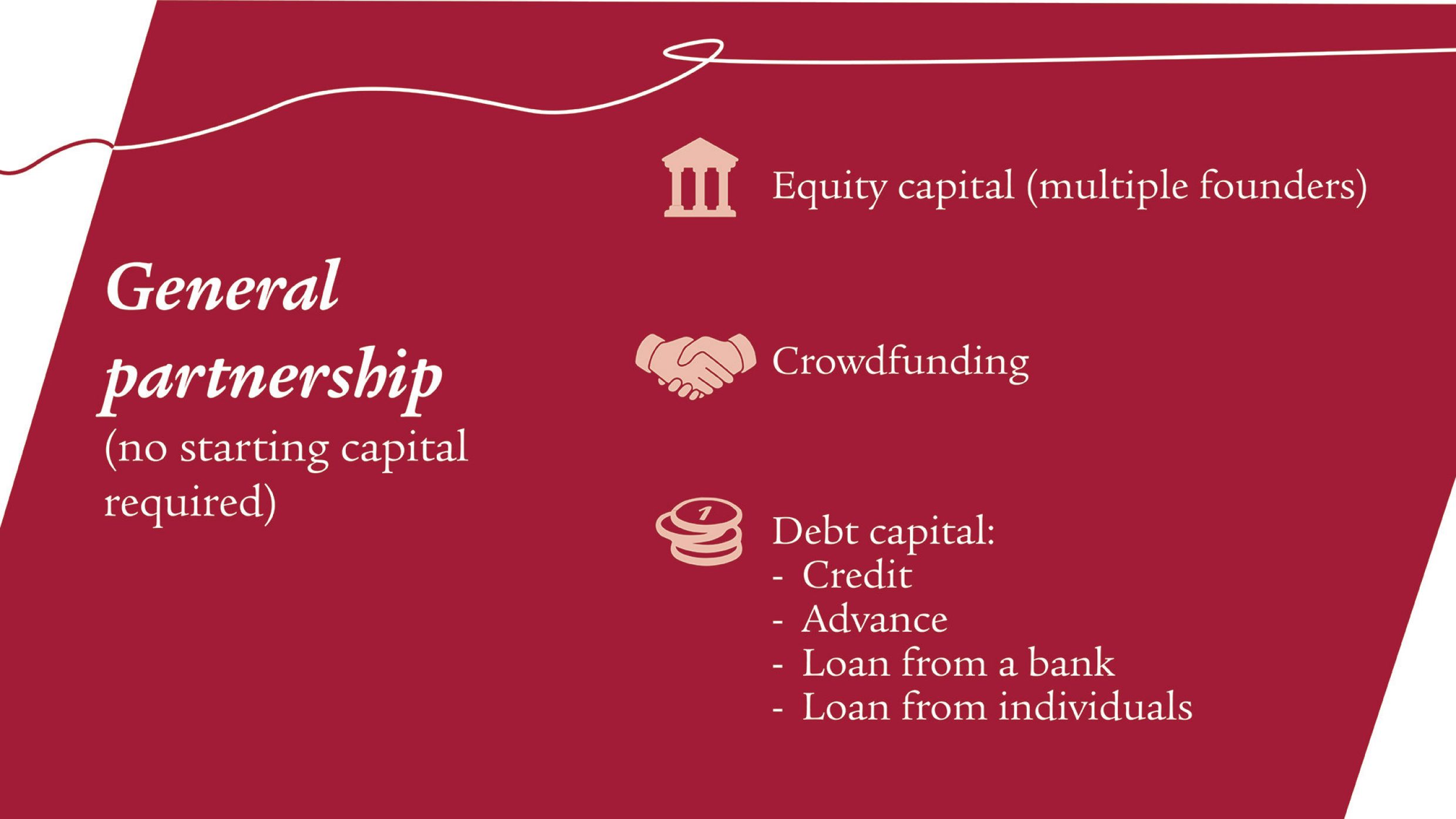

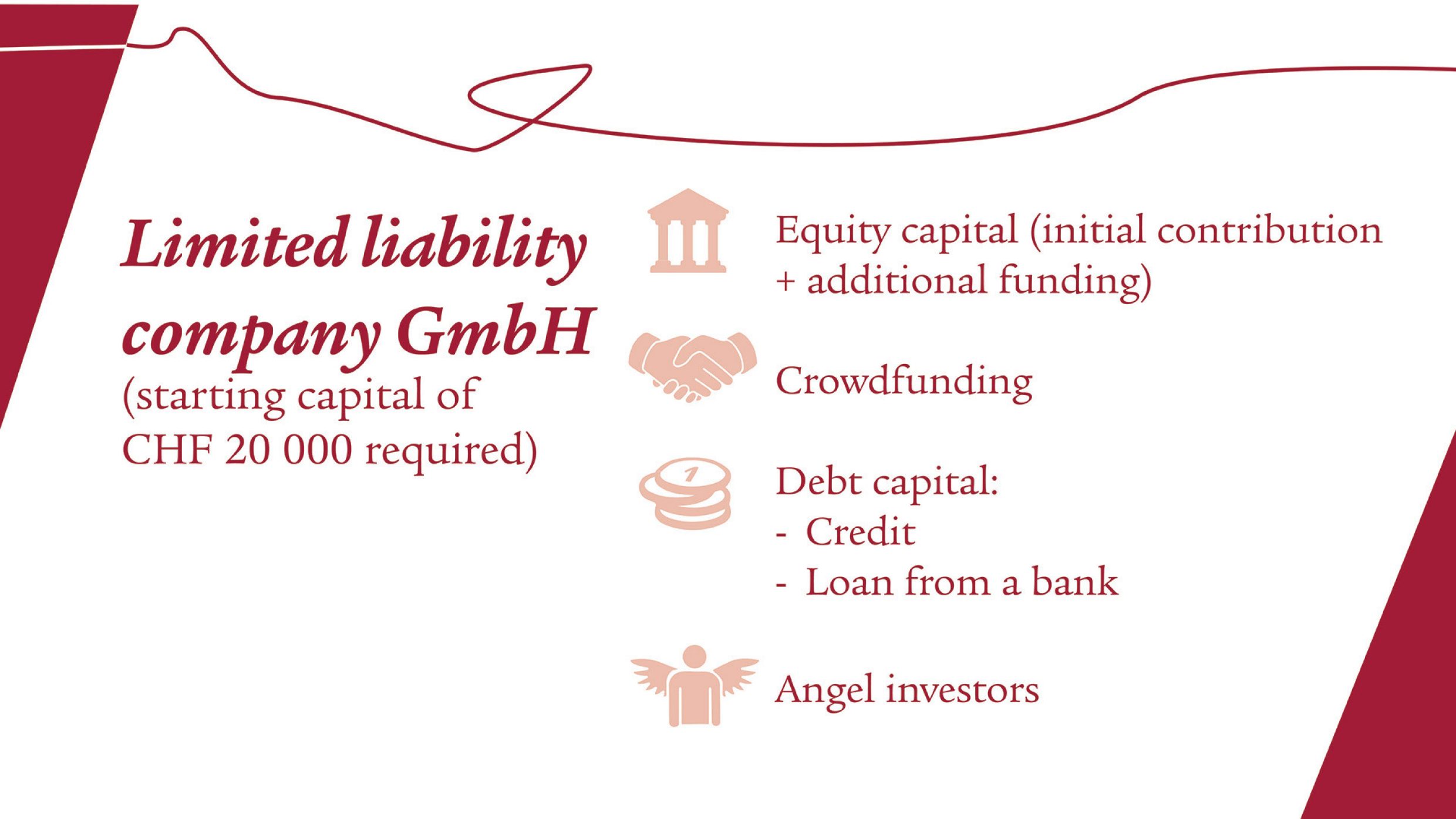

Equity capital

With this option, you can draw on funds from your savings account, securities or assets. Many founders invest some of their own assets in their company. In the case of a sole proprietorship or general partnership, you can make an early withdrawal from your pension fund or terminate your pillar 3a account early and use the funds for your company.

Debt capital

This could be credit, an advance or a loan. However, because it is difficult to know how well a start-up will do, obtaining financing from banks is difficult for young companies. In addition, the riskier a bank thinks a business is, the higher it sets the interest rate for loans.

Loans from individuals

Instead of a bank, it is also possible to borrow money from individuals, for example from relatives or friends. Often, this does not require the same collateral as is the case with banks and people are frequently prepared to offer the money at lower interest rates. However, you should bear in mind the emotional aspects of borrowing money from friends or relatives – you do not want to damage any personal relationships you may have with them. A loan agreement may be of help in this case.

Angel investors

Angel investors may also be an option. Angel investors are individuals and often company founders themselves who, in addition to their funding, can also offer their expertise for start-ups. An example of this is the UK TV show “Dragons’ Den”. In it, start-up founders pitch their business ideas in an attempt to get funding from angel investors. One of the potential investors on the Swiss version of the show is Roland Brack, founder of the online shop of the same name.

Venture capitalists

A similar model is that offered by venture capitalists. These are not individuals, however, but companies or fund management companies that specialise in start-up investments.

Crowdfunding

With crowdfunding, multiple investors, usually individuals, help to finance a company by contributing an amount of their own choosing. There are various online platforms on which start-ups can give a brief introduction about their business, for which potential investors can then easily provide funding. Recently, the Swiss journalist Simona Boscardin, for example, ran a successful crowdfunding campaign. She raised over CHF 50 000 from 664 supporters for her journalistic project “On Fire”.

Foundations

Many Swiss foundations support start-ups. These foundations predominantly select which start-ups they finance by region or sector. It is worth taking a look at the Federal Directory of Foundations (DE, FR, IT only) or the Fundraiso platform.

Am I exempt from my BVG/LPP obligations if I am self-employed? Find out more in the guide “What a company needs to consider in terms of occupational provisions”.

4. Ideal infrastructure

There are start-ups that can commence their business with just a laptop. A coworking space can also make sense for growing start-ups, as additional workplaces may be needed at short notice.

If clients visit your premises, your office and meeting room are your company’s calling card. The same applies if your business idea involves a shop. In both cases, you can offer added value if your business is easily accessible both by public transport and by car.

Depending on the business idea, there are also technical issues such as IT infrastructure, POS systems as well as a professional website. If there are significant requirements in this respect and it is complicated to implement it yourself, it is worth outsourcing these tasks to a specialist company.

5. Choice of legal form

Choosing the right legal form is key when setting up your own company. Here is a brief overview of the main features of the most common legal forms in Switzerland:

Sole proprietorship

Consists of just one person, no starting capital is required, the owner is personally liable, the company founding process is straightforward.

General partnership

Consists of at least two partners who are jointly and severally liable. No start-up capital is required and both partners are jointly and severally liable.

Limited liability companies (GmbH)

A minimum capital amount of CHF 20 000 is required and the partners are not liable with their private assets. These companies must be registered in the commercial register.

Public limited companies (AG)

Starting capital is at least CHF 100 000, of which at least CHF 50 000 must be paid up. Shareholders are liable only for their share. The AG form means that investing is more flexible and is more suitable for larger companies.

A detailed overview of the legal forms can be found at the IFJ Institut für Jungunternehmen.

It is also possible to change legal form after the company has been founded. This makes sense, for example, if the company has grown or another form of financing is required, such as from shareholders.

6. Risk protection and pensionprovisions

Only a few types of insurance are mandatory for sole proprietors. By contrast, for public limited companies (AGs) or limited liability companies (GmbHs), you are considered to be an employee of your own company and therefore many aspects of personal insurance are mandatory. These include pension funds (BVG/LPP), accident insurance and AHV/AVS.

Want to find out more?

Then read our guide “Start-ups:the main types of insurance”. It tells you what risks you should address when setting up a company.

When deciding to become self-employed, think not only about the legal requirements, but also about your personal pension provisions and the risks your company faces. This way, you will remain a financially self-determined business owner. You should protect yourself in such a way that if you suffer an illness or accident, this does not spell the end for your company.

Would you like a consultation?

In any case, it is a good idea to seek advice from an expert when it comes to pension provisions and insurance.

FAQs

Depending on the legal form of the company and income, self-employed persons have the option of paying a higher amount into their pillar 3a than they do when they are employed. They may, however, voluntarily join a pension fund as a self-employed person.

There are various options in this respect: You join your employees’ pension fund if the fund’s regulations allow this. You join a pension fund run by your professional or trade association. Another option is the Substitute Occupational Benefit Institution. However, this only provides insurance within the framework of mandatory BVG/LPP benefits coverage.

Contributions to AHV/AVS, IV/AI, EO/APG and to the Family Allowances Office are mandatory for self-employed persons. However, it makes sense to adequately manage the risks to your company and the people working in it.

With a public limited company (AG) or limited liability company (GmbH), your pension fund assets will be transferred to the new pension fund as they would be if you changed job. If you set up a sole proprietorship or a general partnership, you can also transfer your assets to the new solution. In this case you can withdraw some of them as an early withdrawal and use them as equity to build up your company.