What insurance do I need if I become self-employed? Which insurance is voluntary and which mandatory? And how can I best provide for old age? We answer the most important questions about insurance and future provisions for the self-employed – for a financially self-determined life.

What does self-employment mean?

Self-employment means working for yourself and in your own name, without reporting to an employer. The self-employed bear the entrepreneurial risk themselves, but also benefit directly from their economic success. They are responsible for their own social security and financial security. There are various forms of self-employment in Switzerland, including sole proprietorships, public limited companies or limited liability companies (GmbH/Sàrl) – the insurance requirements vary depending on the legal form chosen.

Self-employment in Switzerland: influencing factors and developments

More and more Swiss people are opting to start their own business and become economically independent. According to a recent study by the IFJ Institute for Young Entrepreneurs, a total of 52 978 new companies were entered in the commercial register in 2024 – a new record. Compared with the previous record year, this represents a further increase of 2.6%.

Several developments have contributed in recent years to the fact that more and more people are taking the leap into self-employment, including digitalisation, working from home becoming common practice and part-time employment as well as a societal shift away from traditional career paths towards a desire for more self-determination in the area of employment.

Would you like to become self-employed?

Our advisors would be happy to help you find the right insurance and future provisions solutions.

What insurance do you need as a self-employed person?

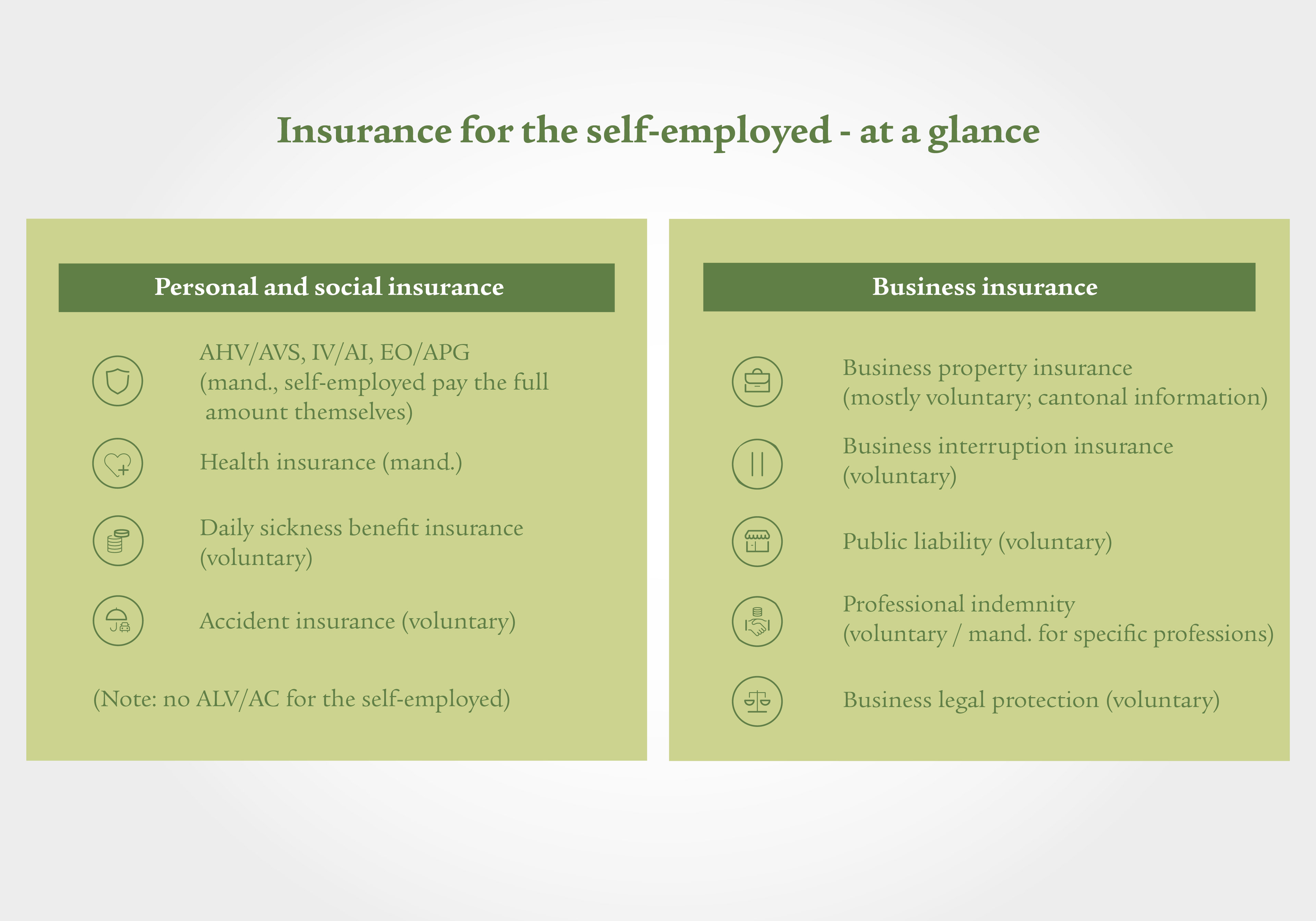

When you are self-employed, you are responsible for your insurance cover. We provide an overview of the most important types of insurance for the self-employed.

Abbreviation: mand. = mandatory

Personal and social insurance

AHV/AVS, IV/AI, EO/APG – The most important types of social insurance for the self-employed

AHV/AVS, IV/AI and EO/APG cover people’s basic needs. The self-employed are also obliged to pay contributions to be covered in old age, in the event of disability or loss of earnings (e.g. through maternity, military service). Unlike employees, the self-employed pay the entire contribution themselves. Contributions are calculated based on income and are settled annually by the relevant social security administration office.

AHV/AVS (Federal old-age and surviving dependants' insurance)

Self-employed people must register with the AHV/AVS administration office and pay contributions – regardless of the legal form of their activity. The amount of the contributions depends on their income: if they earn less, they pay a lower percentage. This depends on the decreasing contribution scale. It starts with an annual earned income of CHF 10 100 at a rate of 5.371% and increases to a maximum of 10% for an income of CHF 60 500 or more. The AHV/AVS guarantees a pension in old age and offers financial support for surviving dependants in the event of death. The amount of the contribution depends on the annual earned income and is definitively calculated after the tax return has been completed.

IV/AI (disability insurance)

IV/AI provides protection against the financial consequences of disability. Depending on the degree of disability, you may be entitled to a partial or full pension. The primary aim of IV/AI is to reintegrate people into working life – including self-employment – for example through retraining or making workplaces more accessible.

If applicable, self-employed people can contact their cantonal IV/AI office directly to apply for benefits.

EO/APG (Ordinance on indemnity for loss of earnings)

EO/APG provides compensation for loss of earnings as a result of military or civilian service, as well as maternity or paternity leave. Contributions to EO/APG are included in the total AHV/AVS, IV/AI and EO/APG contributions.

Unemployment insurance (ALV/AC)

In Switzerland, self-employed people are not insured against unemployment and therefore do not pay unemployment insurance (ALV/AC). Accordingly, they are not entitled to unemployment benefits in the event of unemployment. Voluntary unemployment insurance is not provided for self-employed people. Self-employed people work for themselves and bear full responsibility for their company’s opportunities and risks.

Health insurance

Health insurance covers primary medical care with a wide range of health services. It is mandatory for all residents of Switzerland.

Basic insurance benefits include medical treatment (visits to a doctor and emergency treatment), hospital treatment (in the general ward), prescription medication, psychiatric treatment and treatment by specialists (if medically necessary), and Spitex services (home care with a doctor’s prescription). For benefits in addition to the basic insurance, you can take out supplementary insurance.

Daily sickness benefit insurance

Self-employed people are recommended to take out daily sickness benefit insurance to avoid any loss of earnings. With daily sickness benefit insurance, self-employed people continue to receive an income in the event of incapacity to work. The daily sickness benefit can be paid out for the defined period up to a maximum of 720 days, depending on the insurance policy.

Accident insurance

Accident insurance is not automatically provided for the self-employed in Switzerland. While employees are insured through their employer, self-employed people must ensure adequate cover against accidents themselves. You can voluntarily take out occupational and non-occupational accident protection with Suva or a private insurance company. Such protection is important as accidents can entail high treatment costs and loss of earnings.

For the self-employed, the insured income under accident insurance is determined on the basis of the income from self-employment. As a rule, the actual annual income is taken as a basis, but there are also minimum and maximum limits set by the insurance company. In the event of an accident leading to an incapacity to work, the self-employed person generally receives 80% of their insured income as a daily allowance. As with employees, there is an upper limit for compensation and in the event of a long-term incapacity to work, compensation may fall to a lower amount.

Are you taking the leap into self-employment?

Our experts can advise you on individual solutions for your financial self-determination.

Business insurance

Business property insurance

Business property insurance is the equivalent of home contents insurance – but for companies. It covers damage to the company’s movable property (business contents) caused by fire, water, theft or glass breakage.

This insurance is usually voluntary. In some cantons, however, special requirements apply:

- In Nidwalden and Vaud, insurance against fire and natural hazards is mandatory and can only be taken out from the cantonal building insurance company.

- It is also mandatory in Fribourg and Jura, but there is a free choice of provider.

In all other cantons, it is the responsibility of companies to insure their business contents individually. Insurance protection should always be adapted to cantonal requirements and operational risks.

Business interruption insurance

Business interruption insurance provides protection if operations are shut down, fully or partly, due to insured damage such as fire, water or theft. It covers lost profits, ongoing fixed costs (e.g. salaries, rent) and additional expenses for an agreed period of time.

The prerequisite is that property damage is covered. As an option, insurance can be taken out to cover suppliers being unable to provide goods/services (so-called CBI losses).

Note: business interruption is usually included in the business property insurance policy.

Public liability insurance

Public liability insurance protects self-employed people if their activities cause damage to third parties – such as personal injury or property damage and the resulting loss of assets. Examples are damage caused by faulty products, failed projects or defects in the performance of services.

The insurance covers both justified claims for damages as well as defending unjustified claims – the latter is covered by the insurance as part of what is known as passive legal protection.

The insurance does not cover personal damage, intentional acts, breaches of contractual obligations or pure financial losses without personal injury or property damage. These are covered by professional indemnity insurance.

Professional indemnity insurance

Professional indemnity insurance is essential protection for self-employed people in consulting, medical or service-related professions with an increased liability risk. It covers the financial consequences of any financial losses incurred by third parties as a result of professional errors, negligence or omissions – for example, as a result of incorrect advice, treatment errors or planning deficiencies.

As a specialised form of public liability, it is tailored to the specific risks of individual occupational groups such as lawyers, doctors, architects, fiduciaries or insurance intermediaries. For some of these professions it is required by law, for many others it is voluntary, but highly recommended for reasons of liability and livelihood.

Business legal protection insurance

Business legal protection insurance can be very useful for the self-employed, and depending on the sector it can even be mandatory. It offers legal assistance in disputes with customers, business partners, employees or authorities.

Depending on the contract, business legal protection insurance covers the costs of lawyers, court proceedings, expert opinions or mediation. Collection and criminal defence costs can also be covered.

Important: it covers the costs of the proceedings, not claims for damages.

It is particularly recommended for sectors with many contracts or strict official requirements.

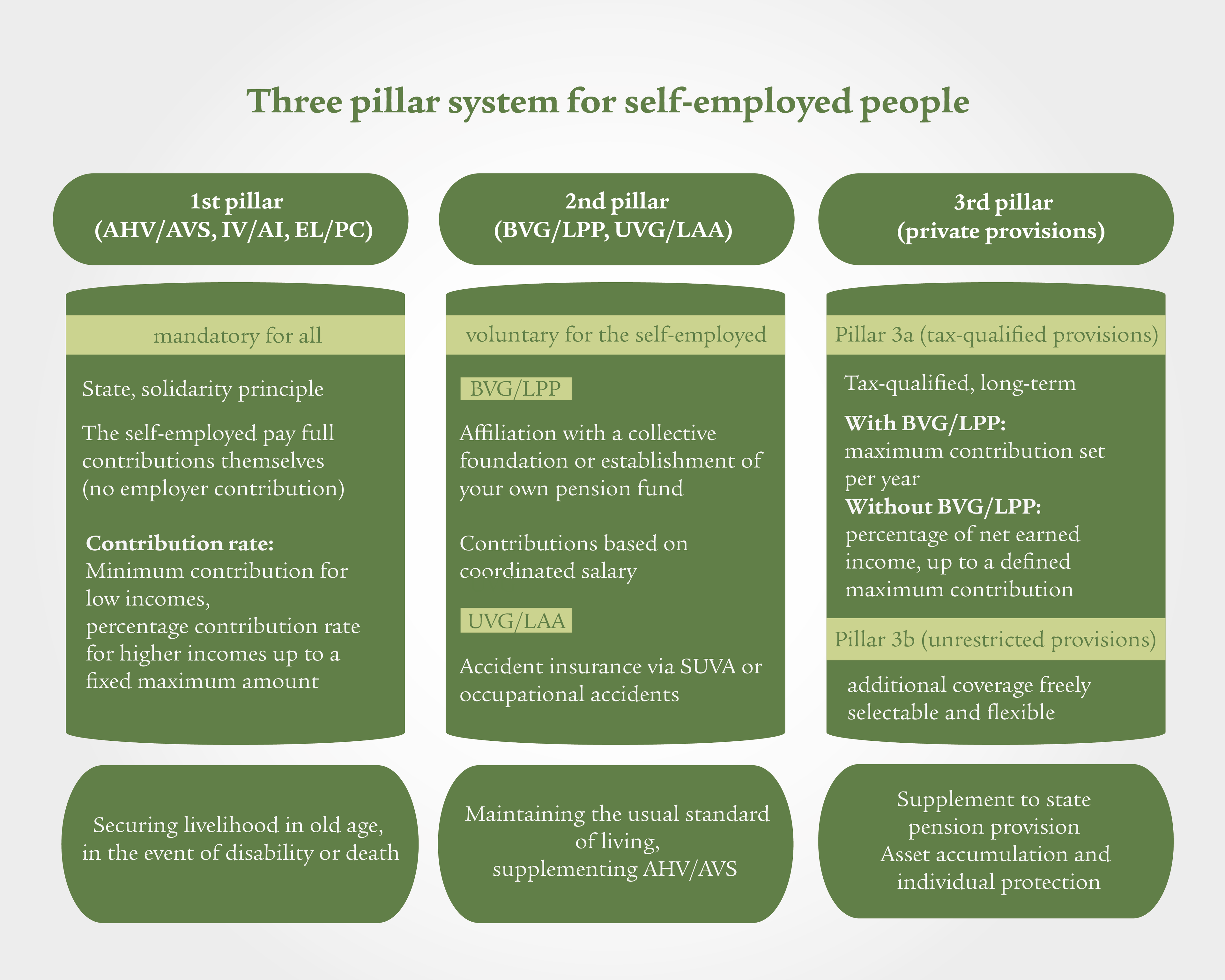

Retirement provisions for the self-employed

Self-employed workers are responsible for their own retirement provisions. They pay AHV/AVS, IV/AI and EO/APG contributions entirely independently. In the case of an employee relationship, the employer pays 50% of the contributions. The second pillar – occupational provisions – is not mandatory. However, it is possible to take out occupational provisions. This makes it all the more important for the self-employed to plan their future provisions actively and with foresight.

Supplementary insurance via the BVG/LPP (Occupational provisions)

Occupational provisions, also known as pension funds, are mandatory for employees in Switzerland. However, self-employed people are not obliged to take out such insurance. They may, however, voluntarily join a pension fund. One option is to join an existing pension solution via a professional association or a collective foundation. Alternatively, private provisions can be used via a pillar 3a solution.

Some insurers and banks offer special BVG/LPP solutions for the self-employed, which allow for higher coverage or a more flexible structure.

Additional protection through the 3rd pillar

Pillar 3a – tax-qualified provisions

Pillar 3a is one of the most attractive retirement provisions options for the self-employed. Private provisions are tax-qualified, since the sums paid in can be deducted from a person’s taxable income. In aktuelles-jahr, self-employed people can pay up to 20% of their net income, up to a maximum of abzug-3a-selbststaendige, into pillar 3a.

Pillar 3b – flexible private provisions

Pillar 3b is particularly suitable for self-employed people who want greater freedom in structuring their retirement provisions and are prepared to invest their assets in various types of assets. This pillar comprises all types of private provisions and savings that are not subject to the tax restrictions of pillar 3a. These include life insurance, savings plans, equities, real estate and other forms of investment such as art.

Arrange a consultation

We are here for you if you need support with regard to future provisions and pillar 3a.

FAQs on self-employment

In Switzerland, AHV/AVS, health insurance (basic insurance) and, depending on the sector, accident insurance or professional indemnity insurance are mandatory.

Daily sickness benefit or business interruption insurance can be used to protect against a loss of income in the event of illness or business closures. Daily sickness benefit insurance pays part of the income during longer breaks due to illness in order to avoid financial difficulties. Business interruption insurance covers a loss of income due to unforeseen events such as fire or natural disasters.

Accident insurance is also important for the self-employed, as it can also cover a loss of income in the event of an accident leading to incapacity to work. This insurance protects against the financial consequences of occupational and non-occupational accidents.

Yes, the self-employed have to pay into the 1st pillar (AHV/AVS) themselves and have the option of insuring themselves voluntarily in the 2nd pillar (occupational provisions). It is also advisable to accumulate a 3rd pillar (private provisions) to optimise your retirement provisions.

Yes, the self-employed are not automatically covered by mandatory accident insurance (UVG/LAA). Voluntary insurance is recommended.

Professional indemnity covers work errors (e.g. incorrect provision of services or advice) for certain occupational groups, while public liability covers personal injury, property damage or financial damage in the company’s day-to-day business.

Small business owners should pay particular attention to AHV/AVS, health insurance, accident insurance, liability insurance and retirement provisions.

No, the self-employed do not contribute to unemployment insurance (ALV/AC). Voluntary insurance against loss of earnings is possible, however.

Business legal protection insurance covers the costs of lawyers, court proceedings and disputes with customers or authorities.

A consultation helps to assess individual risks and select the right insurance cover.

Anyone who works for themselves in Switzerland and offers services or products in their own name is generally considered self-employed. In this case, you must notify the relevant AHV/AVS administration office – ideally as soon as you start working. They check whether all the requirements for being considered self-employed have been met, such as setting your own prices, bearing the entrepreneurial risk, having multiple customers or having your own business presence to the outside world.

Start on the road to self-employment – but with peace of mind!

Our experts can show you which insurance policies are key to your success and how you can best protect yourself.