Pillar 3a enables you to invest strategically in your retirement provisions – while saving on taxes. Tax-qualified provisions help you accumulate assets over the long term, especially if you choose investments with compounding interest. We show you the advantages of pillar 3a and how you can make optimal use of them – for more financial self-determination.

What is pillar 3a?

Pillar 3a is part of the third pillar of the Swiss pension system – private provisions, which also includes non-tax-qualified pillar 3b.

The pension system in Switzerland consists of three parts:

- 1st pillar: state provisions (AHV/AVS, disability insurance and supplementary benefits)

- 2nd pillar: occupational provisions (BVG/LPP, pension fund, accident insurance)

- 3rd pillar: private provisions (tax-qualified pillar 3a and non-tax-qualified pillar 3b)

Pillar 3a is voluntary and serves to bridge the financial gap after retirement. This is because the state pension and employer pension fund only cover on average around 60% of your last income in retirement – depending on your individual situation.

Pillar 3a is tax-qualified, which means that withdrawals are only possible under certain conditions.

What are the advantages of pillar 3a?

With pillar 3a, you’ll be able to lead a financially self-determined life when you’re older: you increase your pension and can close any income gaps after retirement.

Additional advantages of pillar 3a:

- Save on taxes: you can deduct your pillar 3a contributions from your taxable income on your tax return.

- Flexible savings amount: you decide how much to contribute – up to a legally defined maximum amount.

- Long-term asset accumulation: especially when investing in securities, you benefit from the compounding effect – the sooner you start, the better.

- Early withdrawal subject to certain conditions: for example, when purchasing your own home, becoming self-employed or emigrating.

- Early withdrawal before retirement: you can withdraw the savings at the earliest five years before reaching the reference age.

Arrange a consultation

We are here for you if you need support with regard to pension provision and pillar 3a.

What is the maximum pillar 3a amount?

The following maximum amounts apply in aktuelles-jahr for contributions into pillar 3a:

- With a pension fund: maximum abzug-3a

- Without a pension fund: maximum 20% of net earned income up to a maximum of abzug-3a-selbststaendige

The maximum amounts are reviewed regularly by the Federal Council and adjusted annually or every two years in line with salary and price changes.

How can I save on taxes with pillar 3a?

If you pay into pillar 3a, you can deduct your contributions from your taxable income up to the legally defined maximum amount. This reduces your tax burden – how much depends on your income, canton of residence and tax rate. Every year you receive a statement, showing the amount you have contributed, from your bank or insurance company, which you submit with your tax return.

To ensure that your contributions are taken into account for the current tax period, you should make them by mid-December at the latest. Depending on your situation, you could save several hundred to several thousand francs in taxes per year.

Tax calculator

Calculate in just a few clicks how much tax you can save with your 3a contributions – your personal overview, free of charge.

Please accept marketing cookies so you can watch this video. Cookie settings

When can I start contributing to a pillar 3a account?

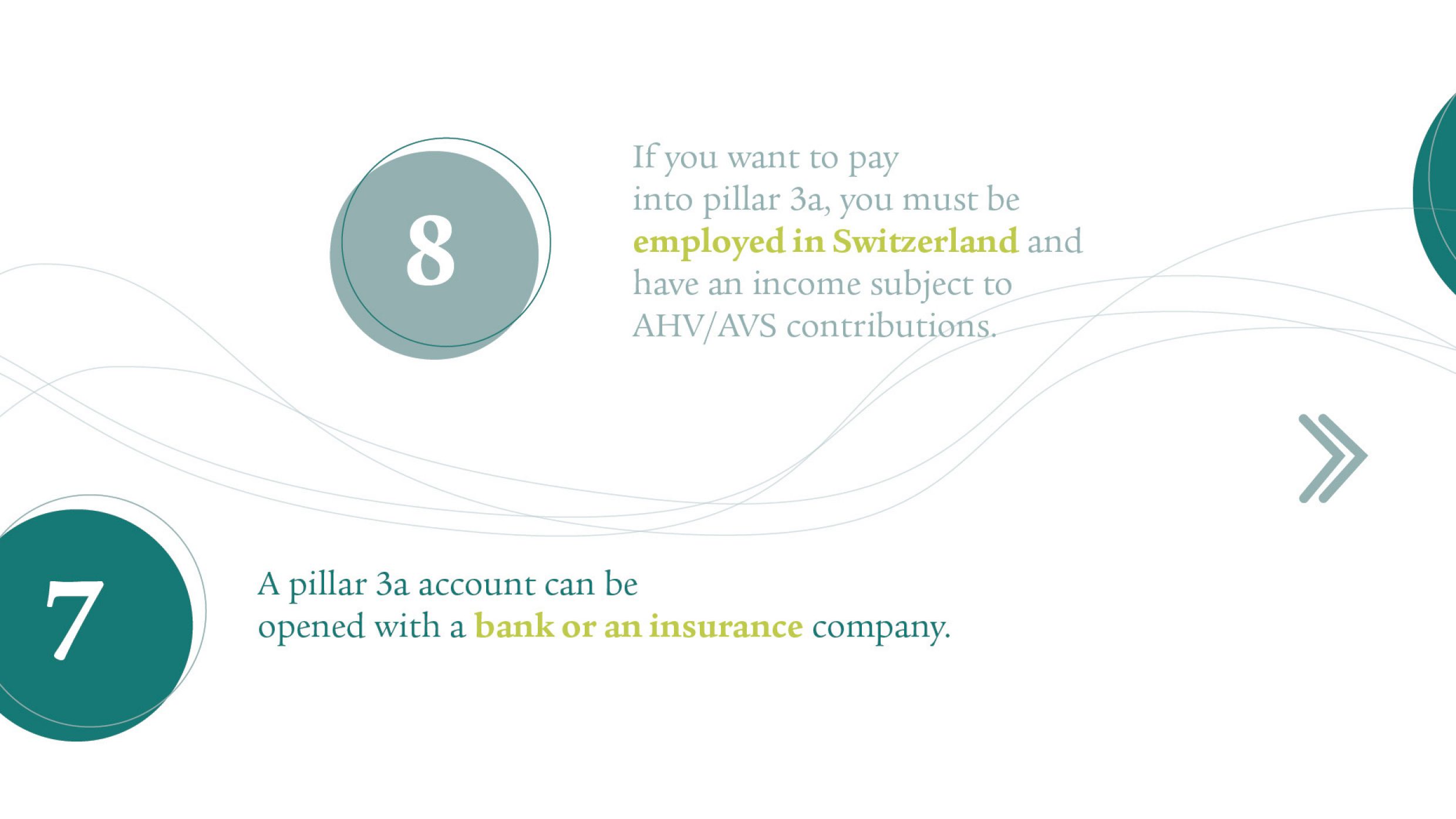

As soon as you start working in Switzerland and earn an income subject to AHV/AVS contributions, you can pay into pillar 3a – whether you are employed or self-employed.

The sooner you start, the better. The longer the money is invested, the more you benefit from the compounding effect – especially if you invest in a 3a solution with securities.

Find out here why paying into pillar 3a early on is worthwhile.

Pillar 3a: insurance company or bank?

You can take out a pillar 3a product either with an insurance company or a bank. Both offer different solutions – depending on how much security or potential returns you want.

Insurance solutions

3a savings policy with guarantee

A fixed-interest 3a savings policy combines retirement provisions with insurance protection in the event of disability and/or death. Part of your premium is used to save, the other part covers the risk. As a rule, you receive a guaranteed minimum benefit in old age – supplemented by possible non-guaranteed bonuses.

Unit-linked 3a policy

With a unit-linked 3a policy, you also benefit from the combination of capital and insurance protection in the event of disability and/or death. The savings component of the premium is put into investment funds, with significantly higher returns expected over the long term. Here too, however, there is a risk that the capital markets are subject to fluctuations. There are also policies that guarantee a minimum payout when they mature.

Bank solutions

Interest-bearing 3a account

With a traditional 3a account, your assets earn a fixed rate of interest. Interest rates are usually slightly higher than on a normal savings account. This solution is secure, and while there is no risk of loss, there is hardly any potential for growth.

Unit-linked 3a account

With a unit-linked pillar 3a account, your money is invested in investment funds, e.g. in equities, bonds or real estate funds. This allows higher returns over the long term – but at the same time there is a risk of value fluctuations. The longer the term, the better these can be offset. Experts recommend an investment term of at least 10 to 15 years.

Think about what’s more important to you: security or potential returns? If you want to remain flexible, a bank solution might be the right choice for you. If you also want protection in the event of death or disability, you should consider an insurance solution.

Which 3a solution is right for me?

The right 3a solution depends on your personal goals, your financial situation and your need for security or flexibility.

Insurance solution – with additional protection

An insurance solution offers risk protection in addition to savings. You can cover gaps in income in the event of disability and protect your family financially in the event of death. Although you commit to a longer term, you benefit from a structured savings plan that enables you to reach your savings target, even in the event of disability, thanks to a waiver of premium.

Bank solution – stay flexible and in control

If you are purely interested in tax-privileged savings and do not need additional insurance protection, a bank solution is often sufficient. You can adjust the contributions flexibly – depending on your financial situation. You need to have self-discipline when it comes to saving, as there is no contractually binding contribution.

When can I start withdrawing money from my pillar 3a?

As a rule, you cannot withdraw your pillar 3a savings until five years before you reach the AHV/AVS reference age at the earliest. Ordinarily, you only withdraw the funds upon retirement.

Early withdrawals are only possible in certain exceptional cases:

- Taking up self-employment provided you are no longer affiliated to a pension fund

- Purchase, construction or renovation of your own home

- Repayment of a mortgage on your own home

- Permanently leaving the country

- Receipt of a full disability pension, if your pillar 3a does not cover disability benefits

Special tax regulations and some reporting obligations apply in the case of an early withdrawal.

What happens to my pillar 3a assets if I die?

If you die, your pillar 3a assets are paid out to specific people in accordance with legally defined rules. In the first instance, this is your spouse or registered partner. In their absence, children, life partners, parents or other close relatives may be next in line, depending on the situation. The exact order is determined by law and there is little scope for making your own choices.

Find out who your beneficiaries are – especially if your life situation changes.

How many 3a accounts can I have?

You may have several 3a accounts – there is no legal limit. Many people deliberately open two to three accounts so that they can withdraw their pension plan savings in stages over several years when they retire.

This allows you to save on taxes, as capital withdrawals from pillar 3a are taxed progressively: the more you withdraw in a single year, the higher the tax rate.

In some cantons, special tax rules apply if savings are withdrawn from multiple 3a accounts within a short period of time. Seek advice in good time to plan how best to stagger your withdrawals.

Can I make top-up payments into my pillar 3a?

From 2026, it will be possible to retroactively make top-up payments for missing pillar 3a contributions for up to ten years. Top-up payments will be possible to cover contribution gaps from 2025 at the earliest and only for people who work in Switzerland, earn an income subject to AHV/AVS contributions and who have not fully paid in the maximum pillar 3a amount in the past ten years.

How does that work?

In addition to paying the maximum annual pillar 3a amount, you can top up any unused amount from previous years. For example, a person who does not pay in full the maximum amount of CHF 7258 in 2025 can make top-up payments for this missing amount in the next ten years.

The prerequisites for this are:

- You must have earned income subject to AHV/AVS contributions in Switzerland in both the year in which you wish to make the top-up payment and the year to which the top-up payment applies.

- You must have already reached the maximum amount for the year in which you are making the top-up payment before you can top up previous years.

Important information:

- Top-up payments can be made for the first time in the 2026 tax year for 2025.

- Contributions for years prior to 2025 cannot be made retroactively.

- The maximum possible top-up payment per calendar year is limited to the “small contribution to tax-qualified provisions”, which corresponds to the maximum annual amount. This amount applies to people with and without a 2nd pillar and is to be paid in the form of a one-off payment.

- The top-up payment is fully deductible from your taxable income together with the normal maximum amount.

What is the difference between pillar 3a and pillar 3b?

Pillar 3a comprises tax-qualified provisions and is subject to clear legal requirements. It is designed to provide retirement income and offers tax advantages – but withdrawal of assets is only permitted under certain conditions (e.g. retirement, home ownership, self-employment).

Pillar 3b comprises non-tax-qualified provisions. It is not regulated by law and offers more flexibility: you have access to your saved assets at any time. Pillar 3b is suitable for medium to long-term savings targets, but also for risk insurance or as a supplement to retirement provisions.

Find out more about pillar 3b here.

Set up pillar 3a now

Obtain free pillar 3a advice with no strings attached.