Inheritance is a complex subject that is often associated with questions and challenges. Although laws regulate the distribution of the estate, personal decisions play an equally important role. We’ll show you what you need to know and bear in mind on the subject of inheritance.

Inheritance comprises the entire estate of a deceased person, including assets such as valuables, bank deposits, securities, real estate and personal belongings, as well as debts such as mortgages. In Switzerland, the order of succession is governed by the Swiss Civil Code (SCC), but can be arranged individually to the extent permitted by law in a will or contract of inheritance.

The basics of inheritance in Switzerland

According to the University of Lausanne, around CHF 100 billion is bequeathed in Switzerland every year. Precise data is not available, as the majority of inheritances in Switzerland are not subject to tax (NZZ, November 2025).

Basic terms related to inheritance:

- Testator: The deceased person whose assets are being passed on.

- Heir: Person who receives part of the testator’s estate.

- Will: A written unilateral declaration of intent in which a person states who should receive what after their death.

- Lineage: The lineage system describes the legal order of heirs.

- Estate: All assets less all debts that remain after death.

Inheritance law in Switzerland

In Switzerland, inheritance law (Swiss Civil Code) governs who inherits the estate of a deceased person. With a will or contract of inheritance, you can determine part of the distribution of your estate yourself.

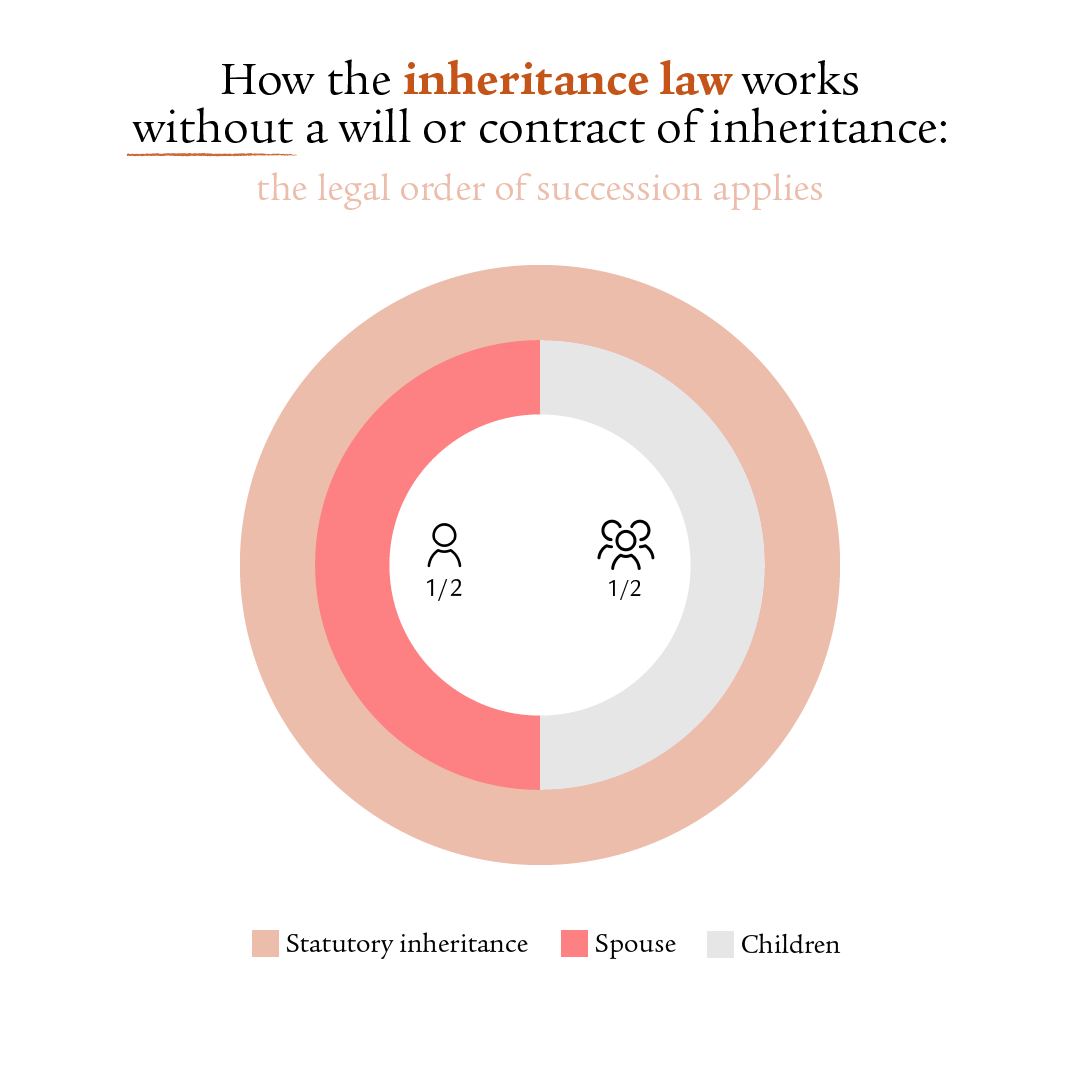

Without a will or contract of inheritance

If there is neither a will nor a contract of inheritance, the estate will be distributed according to the legal order of succession. The order of succession is based on blood kinship – including adoption – and follows the principle that close relatives exclude distant ones. If the deceased person leaves behind descendants, they inherit first. The surviving spouse or registered partner is always entitled to an inheritance.

An overview of the statutory inheritance portions:

The testator leaves behind ...

- Descendants only: 100%

- Spouse and descendants: 50% each

- Spouse and heirs in the parental line (e.g. parents, siblings, nieces, nephews): 75% for spouse, 25% for parental line

- Spouse and heirs in the grandparental line: 100% for spouse, 0% for grandparental line

The spouse’s compulsory portion will remain at 50% of the statutory inheritance. Cohabiting partners are not entitled to a statutory inheritance. If you would like to designate your life partner as the beneficiary, you must record this in your will.

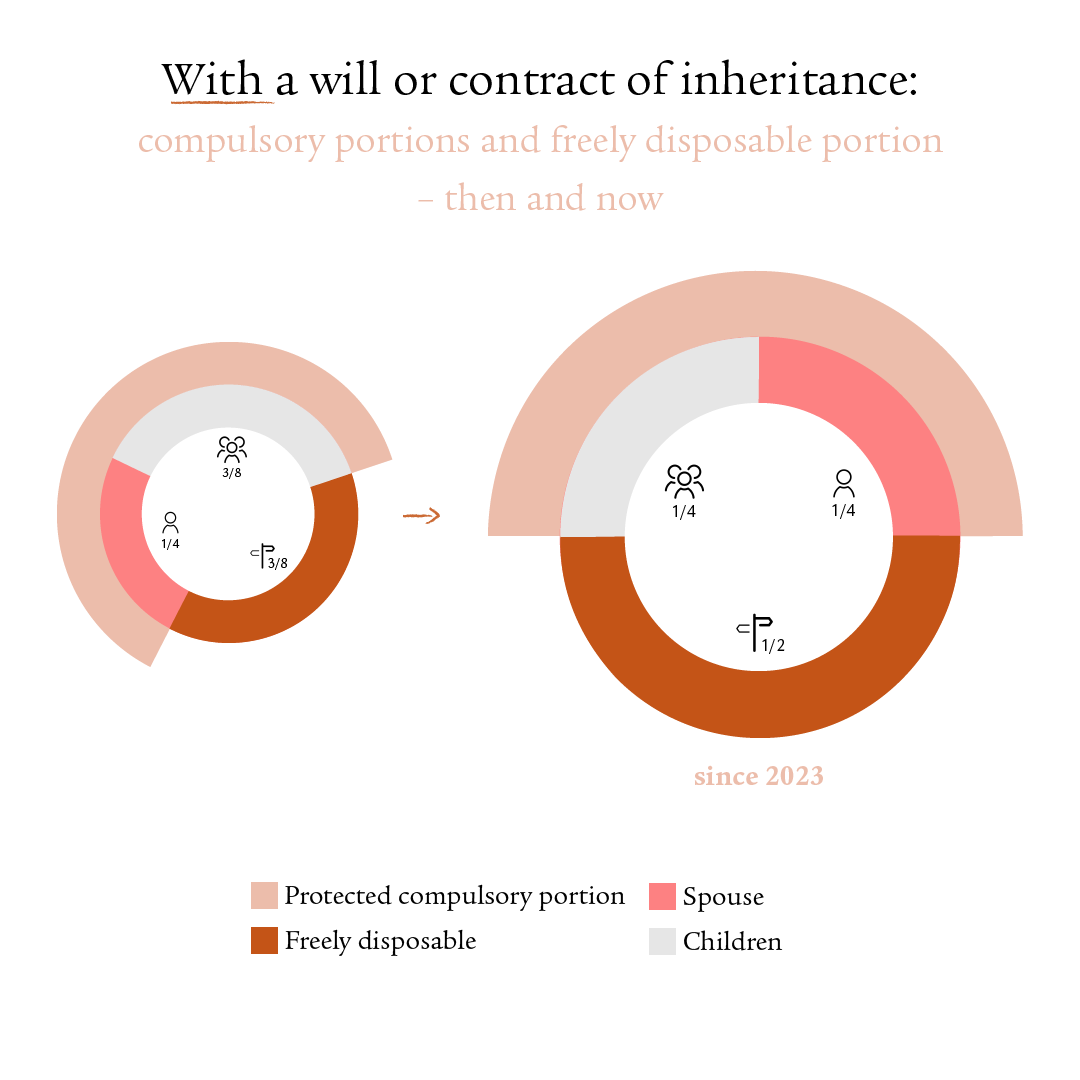

With a will

When you draw up a will, you determine for yourself who inherits and how your estate is to be distributed, as far as possible by law. In doing so, the statutory compulsory portions must be respected.

With a will, you can set out rules for the division, determine legacies, limit heirs protected by compulsory portion rights to their portion and designate other beneficiaries, amongst other things:

- You can allocate a larger share to your spouse or registered partner, so that they receive more than your children.

- You can include people who are not automatically designated as heirs by law – such as your cohabiting partner, godchildren or institutions.

Limits of inheritance

You cannot entirely exclude certain people from the inheritance. This includes the following:

- Your wife, husband or registered partner

- Your children and – if they have already died – their descendants

These persons are always entitled to half of their statutory inheritance entitlement: the compulsory portion.

More distant relatives such as parents, siblings and cousins, on the other hand, are not classed as heirs protected by compulsory portion rights. They can therefore be completely excluded, if you state clearly in your will to whom your assets are to be allocated.

Find out more about inheritance law in Switzerland here

Our article on inheritance law tells you everything you need to know about the partially revised inheritance law that entered into force in 2023.

Will & contract of inheritance

Will

A will is a unilateral decision that allows you to determine who receives what from your assets. You can create, amend or revoke a will on your own at any time – without the consent of others. It is important that the following requirements are met: the will must be handwritten, dated and signed, and the author must be at least 18 years old and capable of judgement. On request, it can also be established as part of an official certification.

With a will, you can designate additional heirs within the scope of the freely disposable portion (not subject to compulsory portion protection), or allocate more to individual legal heirs, amongst other things. You can also pay out legacies or determine rules on imputation and division of the estate. In doing so, you can make a binding decision on how your estate is to be distributed.

Contract of inheritance

Unlike a will, a contract of inheritance is a joint declaration of intent between several persons. It offers more options: a married couple with children can, for example, comprehensively benefit each other by their children contractually waiving their entitlement to compulsory portions.

The same requirements apply to a contract of inheritance as to a will: you must be at least 18 years old and capable of judgement. Unlike a will, a contract of inheritance cannot be drawn up by hand – it must be officially registered, e.g. by a notary. Subsequent changes or revocations are only possible with the agreement of all contracting parties.

Patient decree

Tip: You should also consider a patient decree. This allows you to relieve your relatives in stressful situations and at the same time determine which medical measures you agree to – and which ones you don't. That way you retain self-determined control over important decisions.

Tax aspects related to inheritance

In Switzerland, there is no inheritance tax at federal level – each canton regulates this itself. With the exception of Obwalden and Schwyz, all cantons levy inheritance tax. The amount and who has to pay it varies by canton.

Inheritance tax is generally paid by the heirs. Spouses and registered partners are tax-exempt in all cantons. Inheritances to descendants are only subject to inheritance tax in the cantons of Appenzell Innerrhoden, Neuchâtel and Vaud.

Other heirs may be subject to tax

Depending on the canton, other persons may be subject to tax, such as:

- Cohabiting partner

- Parents

- Siblings

- Nieces and nephews

- Friends, distant relatives or organisations

Depending on the canton, the tax burden ranges from moderate to very high. The canton of residence of the deceased person applies; in the case of real estate, the canton of the location applies. Generally, inheritance tax is progressive in two ways: the higher the amount and the more distantly related.

Advance inheritance and gifts

Advance inheritance

An advance inheritance occurs if a portion of your future inheritance is already paid out to your legal heirs during your lifetime. For example, if parents transfer assets to their children during their lifetime – such as money to buy residential property or the transfer of a property. The amount given in advance is later offset when the estate is divided up to ensure that all heirs are treated equally (hotchpot). A hotchpot may be ruled out if the compulsory portions are maintained by the heirs.

Gifts

A gift is an amount of money given to someone free of charge that is not automatically included in the subsequent inheritance. It can be transferred to the heirs or to third parties. Gifts to children, however, are often assumed to constitute an advance inheritance unless they are expressly excluded from the hotchpot.

Pay attention to gift tax

Advance inheritance and gifts may be taxable as they are subject to cantonal inheritance and gift tax. As a rule, the recipient is liable for tax. The canton of residence of the donor applies; in the case of real estate, the canton of the location applies.

Please note: spouses and registered partners are exempt from gift and inheritance tax in all cantons. Only the cantons of Appenzell Innerrhoden, Neuchâtel and Vaud levy inheritance and gift tax on descendants.

FAQs

Assets held in a deceased person’s pillar 3a (insurance or bank) solution do not form part of the estate and are not bequeathed. The assets are paid out as a lump sum directly and outside the order of succession to the beneficiaries, in accordance with the applicable regulations. However, the lump sum paid out or the surrender value (for 3a insurance policies) is taken into account in the calculation of the compulsory portion.

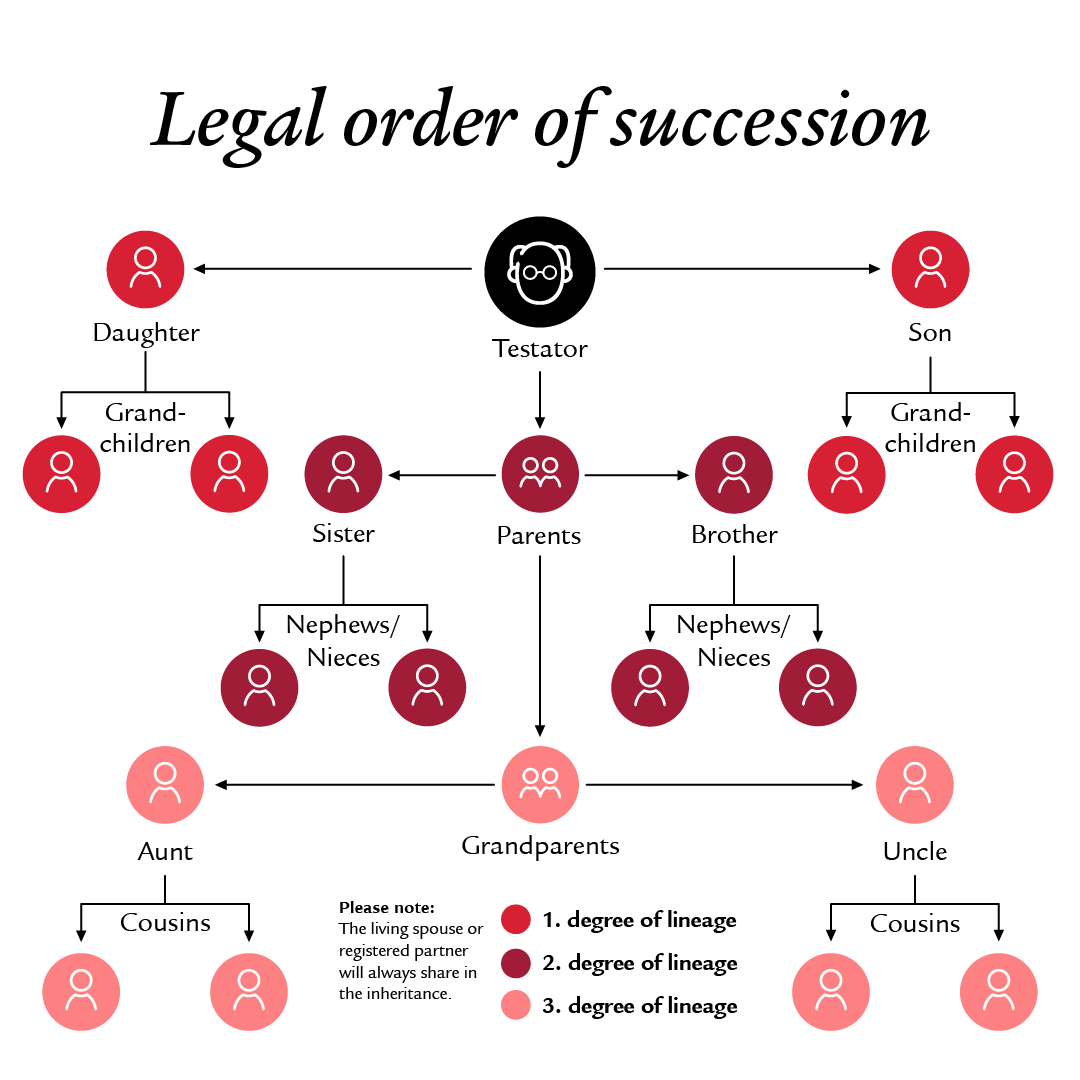

If the testator does not leave a will or contract of inheritance, the estate will be distributed according to the legal order of succession. The order of succession is based on blood relations (including adoption).

Closer relatives exclude more distant ones. As long as the testator leaves behind descendants, these will exclude all other relatives. In addition, the surviving spouse or registered partner will always inherit.

Unless the contract of inheritance or the will stipulate otherwise, the heirs are divided into three lines of succession (inheritance orders). The first line – the descendants – inherits first. If the testator leaves no descendants, the second line inherits – this is the parents or their descendants (siblings, nieces/nephews). If the testator is not survived by any parents or their descendants either, the third line – the grandparents or their descendants (uncles/aunts, cousins) – inherits. If there are no heirs in the third line, the estate goes to the community. If the testator has a spouse or registered partner, this person always co-heirs.

A will is handwritten, dated and signed formally – without a notary. If you wish to or are unable to handwrite your will, you can have it officially registered. This may offer additional security, as a specialist checks the legality and safeguards the document securely if necessary.

Spouses and registered partners will inherit automatically – but not everything. The proportion depends on whether there are descendants or, in their absence, heirs in the parental line. Unmarried couples (cohabiting partnership) will inherit nothing without a will. If you want to designate your partner as an inheritance beneficiary, you must arrange this in writing – for example, with a will or contract of inheritance.

Yes, this is possible. You can specifically favour your grandchildren in your will – however, the statutory portions of your own children and, if applicable, your spouse/registered partner must be respected. Only the freely disposable portion of your assets can be allocated in full to your grandchildren. If your children voluntarily waive their entitlement to a compulsory portion, this can be expanded even further with a contract of inheritance.

Plan your inheritance early

If you would like to learn more about this important topic or if you have any questions, we would be pleased to provide you with more information – in a personal and non-binding consultation.