For many students, saving and providing for the future still sounds a long way off. How should you think about life in retirement when you’re already overwhelmed by the question “where do you see yourself in five years’ time”? That’s where this guide comes in. It shows in a clear way how students can save early, take their first steps in providing for the future while avoiding typical mistakes – so that saving and future provisions make sense even while they are still studying.

We will show you how a budget plan can help to provide an overview of your own finances and optimise them as necessary. We will also provide valuable tips on why it is so important for students to pay into their AHV/AVS, and what else you need to keep in mind financially and in terms of pension provisions.

Pension & financial tips

AHV/AVS 1st pillar

Students are also required to contribute to the AHV/AVS. For people who are not in gainful employment, their obligation to pay contributions begins on 1 January of the year in which they turn 21.

This is especially important when studying, as AHV/AVS contributions are easily forgotten when you do not have a regular income. If contributions are not paid, contribution gaps open up. These will later have a direct impact on the level of your AHV/AVS pension.

The most important tip for students

Check early on whether your AHV/AVS contributions have been paid and take active steps to ensure they are. If you have little or no paid employment when studying, you have to pay the contributions yourself. That way you can avoid a reduced pension later on in life.

How students can meet their obligation to pay AHV/AVScontributions:

- Gainful employment alongside studies

If you are employed, your employer pays your AHV/AVS contributions directly to the social security administration office. The minimum contribution is deemed to have been paid if AHV/AVS contributions amount to at least CHF 530 per year.

If you are self-employed, you pay AHV/AVS contributions yourself and need to register directly with the social security administration office.

- Not in gainful employment

If you are not working, you have to pay AHV/AVS contributions of CHF 530 yourself. That way you avoid contribution gaps and secure your future pension.

- Married or in a registered partnership

If you are not in gainful employment, it is sufficient for your spouse to pay at least twice the minimum AHV/AVS contribution of CHF 1.060. This covers your duty to pay contributions.

Verification by social security administration offices:

The cantonal social security administration office at your place of residence will send you a letter of clarification once a year. The QR code on this letter will take you to an online questionnaire. This questionnaire is then used to check whether your duty to pay contributions has been met.

Beware of gaps in contributions

Contribution gaps are easy to overlook, but should be taken seriously. Missed payments can only be made retroactively for a maximum of five years, otherwise you will receive a lower 1st pillar pension.

Pension fund

Students who work are required to contribute to their pension fund to cover the risks of disability and death from 1 January of the year in which they reach the age of 18. The duty to pay contributions towards retirement savings begins at the age of 25. As a general rule, anyone who earns more than zweite-saeule-minimum-jahreslohn per year in an employment relationship (as at aktuelles-jahr) is admitted to a pension fund and makes the relevant contributions.

Contributions to pillar 3a

Even if as a student you often have little money left over to put towards your private savings, it is worth paying into a pillar 3a at a young age. Thanks to compound interest, even small contributions can make a significant difference, as compounding increases your assets exponentially.

Find out more here why it is worth making early payments into a pillar 3a.

Arrange a consultation

Our experts can answer all your questions about insurance, pension provisions and saving

Saving tips

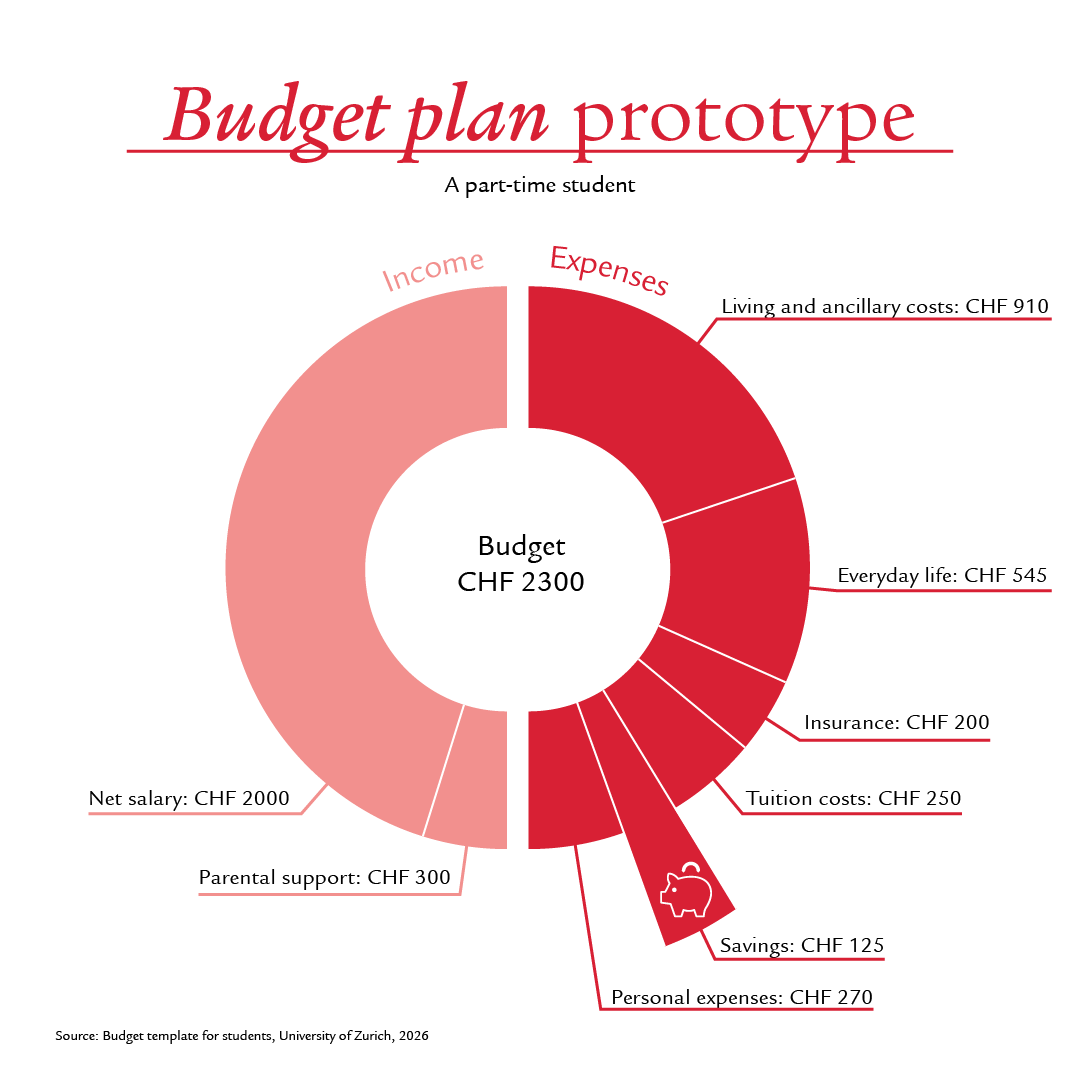

Budget planning

Especially when you are on a tight budget, it’s worth having an overview of your income and outgoings. You should scrutinise the individual items in your budget in order to optimise your finances.

Save first, spend later

It makes sense to open a savings account and set up a standing order at the beginning of the month with regular payments into this account. The less money you have in your current account, the less temptation there will be to spend it. Even if you can save only a small amount: if you incur unexpected expenses, for example repair costs for a broken laptop, it’s good to have a financial buffer to fall back on, no matter how small.

Saving with a bank account

Many financial institutions offer student accounts with no account maintenance fees. In some cases, there is also a welcome credit for opening an account. Find out where offers the best advantages.

Fund-based savings plan

In addition to a traditional bank account, there is also the option of investing money in a fund-based savings plan. Here, your money is regularly invested in investment funds or ETFs. That way you benefit from additional potential returns on the financial markets. This makes it particularly suitable for long-term asset accumulation.

A fund-based savings plan is quite simple: you automatically pay in a fixed amount each month and gradually accumulate assets. This is possible even with small amounts and is compatible with a student budget.

To get started, you need a custody account and to determine how much money you would like to invest each month.

Saving on health insurance

It's worth comparing your health insurance premiums regularly. You can get offers from different health insurers and compare them. Not only the amount of the premium can vary, but also the services and products included.

Basic insurance can be terminated every year by the end of November, so you should look at your health insurance needs before then. How often do you go to the doctor? What types of treatment do you prefer? Do you value supplementary insurance?

Further tips on saving money for students

Students can often benefit from student discounts. You should find out where offers these discounts. Often you can get discounts on leisure activities or online student discounts on music streaming, mobile phones or clothing.

Our advice

Before making an order online, it’s worth asking a search engine whether the provider offers a student discount.

Financing your studies

There are several ways to get financial support to help fund your studies. It is important to address the issue early on and be aware of the options.

Grants are a key form of student financing. As a rule, the canton in which you live is responsible for them. The application should be submitted in good time, ideally several months before you begin your studies. It should be noted that the amount and requirements vary from canton to canton. In addition, universities and private foundations also award grants. These are available irrespective of the canton and represent a further means of assistance.

Another option is a part-time job alongside your studies. Especially for part-time students, this can be a viable solution to cover ongoing costs while also gaining work experience.

Financial support from your family can also play a role. Which combination is best for you depends on your personal situation. If you start planning early, you will have more financial security and can better concentrate on your studies.

Protection for students

Protect against accidents

As a student, you don’t automatically have accident insurance. In the event of an accident, you may incur significant costs, in addition to suffering from the consequences of the accident. It is therefore strongly recommended that as a student, youtake out accident insurance as part of your health insurance.

If you work at least eight hours a week for one employer, you are insured for occupational and non occupational accidents on a mandatory basis. Otherwise you are not automatically insured for accidents and should therefore take out accident insurance with a health insurer.

Protection against disability

There is protection through state disability insurance (IV). A normal disability pension will be paid as soon as three contribution years have been reached. If a student has not reached these contribution years, they will still receive a 1st pillar disability pension amounting to only 133.33% of the minimum disability pension. However, these benefits do not cover the subsistence level. If you work while studying, you are also insured against the consequences of accidents through your employer and you would also receive a disability pension via this accident insurance. If you do not work, only the limited accident cover provided by your health insurance, which does not pay any pensions, applies.

Students are not covered by occupational provisions (2nd pillar) against disability caused by illness or accident. This can lead to significant financial shortfalls in the event of an emergency. It is therefore recommended to take out private disability insurance while you are studying.

Arrange a consultation

Our experts can answer all your questions about insurance, pension provisions and saving

This guide was created with the support of Swiss Life intern Camilla Zanoni.