The subject of future provisions is complex and demanding. We know that. That’s why we offer you advice and support – so you can look forward to a financially secure and self-determined future.

Savings insurance explained simply

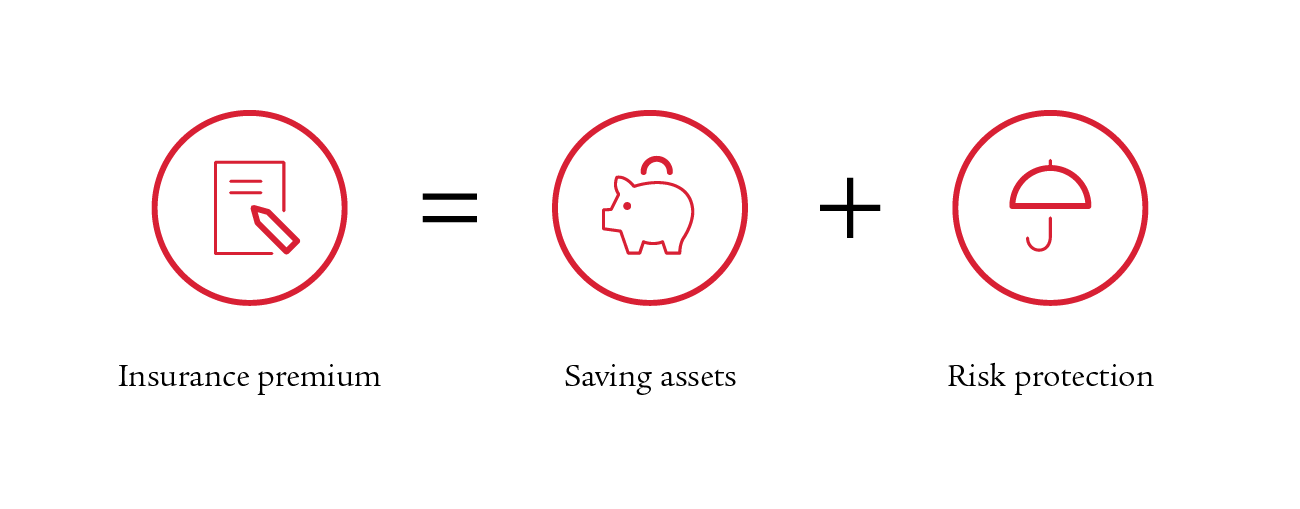

Savings insurance essentially consists of two parts:

The savings component allows you to save assets – as provision for the period after retirement, for the purchase of residential property or to fulfil a life’s dream. At the end of the contract term, the accumulated savings will be paid out to you.

But what if something happens to you during this saving process? If you become disabled or even die? Then the second component of savings insurance applies: individual risk coverage against the risks of death and/or disability. This way you can be sure that you or your loved ones will definitely reach your savings target and are ideally protected.

What are the advantages of savings insurance?

Personal risk protection

Even if you don't like to think about it: disability as a result of illness or accident can affect anyone. The often-heard belief that someone who is in work is well covered is deceptive. That's why it’s worth analysing your actual situation when it comes to protection. This is particularly true for people who are (temporarily) not working. In this situation, the need for protection is likely to be even greater.

Death is a great emotional burden for the survivors. And how does this affect their financial situation? Are the first and second pillar benefits sufficient or are they leaving you with a financial as well as an emotional burden due to insufficient funding?

With risk protection, you protect yourself and your loved ones from the financial consequences of being unable to work. For example, you can integrate a lump-sum death benefit or a disability pension directly into your savings insurance.

Pension plan savings in safe hands

The accumulated capital is paid out to you at the end of the contract term. But what happens to your money up to the time of payout? Our financial experts invest it during the contract term in accordance with your wishes.

What savings insurance options are there?

Depending on the product, you can structure your savings insurance with Swiss Life with various options to suit your personal life situation and needs. Because your self-determination is important to us.

This includes the following:

With our 3a solutions, you can strengthen your private provisions through regular premium payments. If you are unable to pay the premium, you can simply take a break from paying the premium and suspend the payment. Of course you can also pay in more than the planned savings amount each year. For example, you can fully exploit the pillar 3a maximum and the associated tax advantages.

You save taxes by paying into the 3rd pillar – year after year. Pillar 3a, also known as tax-qualified provisions, is primarily used for retirement provisions and therefore enjoys tax advantages. Up to a statutory maximum amount (aktuelles-jahr for employees: CHF abzug-3a p.a., for self-employed persons: CHF abzug-3a-selbststaendige per year) contributions are exempt from income tax. On the other hand, the funds are tied up until normal retirement age and can only be withdrawn early under special conditions – such as when acquiring residential property. In pillar 3b, on the other hand, you are much more flexible with regard to deposits and withdrawals.

Tax calculator

Would you like to know how much tax you can save with pillar 3a?

FAQ pillars 3a/3b

Would you like to learn more about the differences and benefits of the two pillars? You will find answers to frequently asked questions here.

Everyone has their own goals and desires. This gives rise to different interests and opportunities for investing your savings. That’s why we use your information on risk appetite and financial situation to determine your individual investment and risk profile. It helps you choose the right pension solution. You can also determine for yourself which investments you would like to invest in. We recommend that you make such decisions together with your advisor – take advantage of the know-how of our experts.

You can also delegate all investment decisions to our investment and asset specialists at Swiss Life Asset Managers (SLAM). SLAM is a well-known European asset manager with over 165 years of experience and strong investment expertise.

Your next steps

- We will be happy to answer all your questions in a personal consultation.

- We will help you analyse your situation and determine your personal needs.

- We will work with you to find the savings insurance that best suits you.