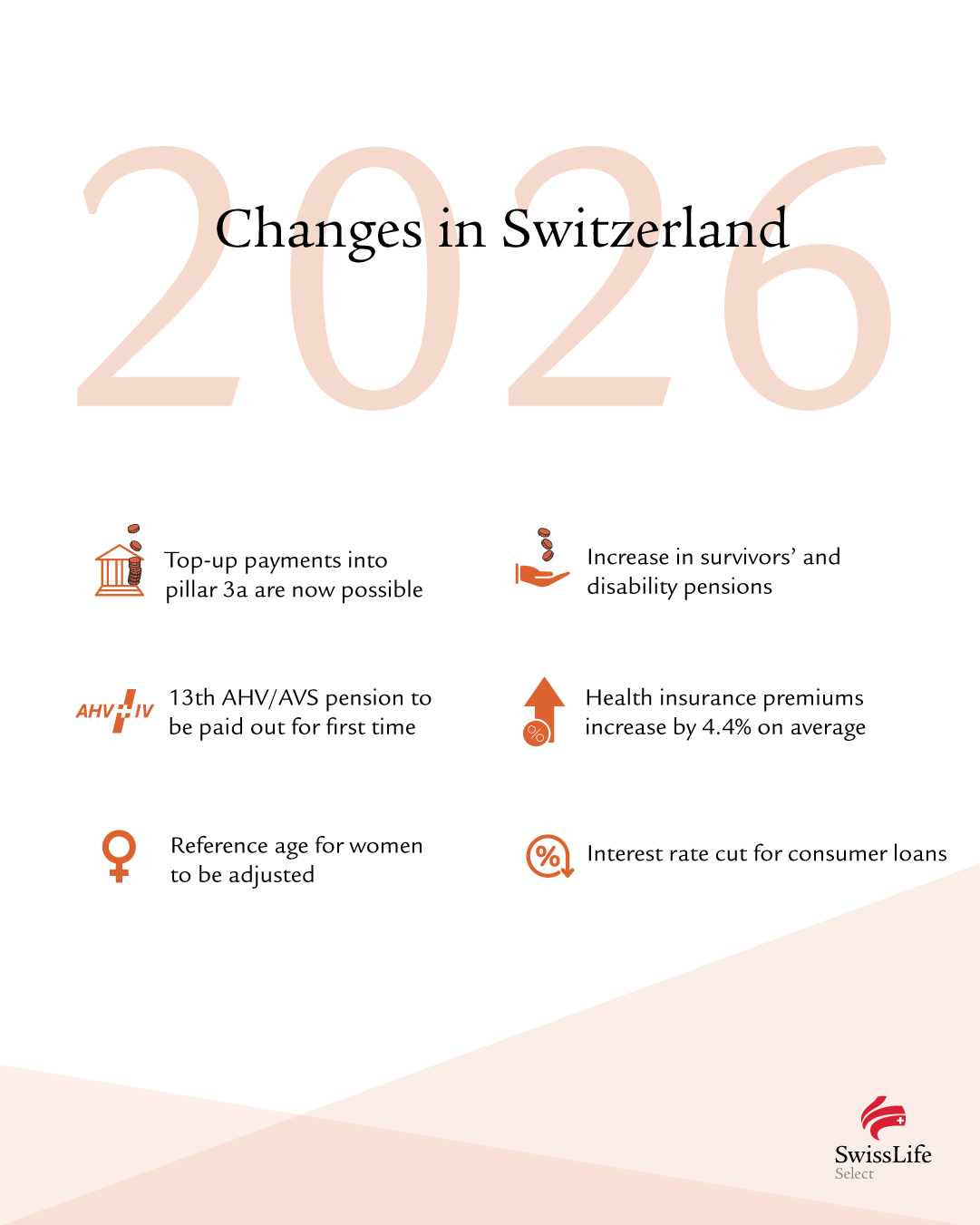

2026 will bring a number of changes in various areas of life. These include rising health insurance premiums, the introduction of the 13th AHV/AVS pension and the new option to pay pillar 3a contributions retroactively. This article provides an overview of the key changes in 2026.

Would you like a consultation?

We provide comprehensive advice tailored to your goals at a place of your choice.

Pensions

Pillar 3a top-up payments

From 2026, it will be possible to pay missing pillar 3a contributions retroactively for up to ten years. This applies to gainfully employed persons in Switzerland with income subject to AHV/AVS contributions who did not use up the maximum pillar 3a amount in previous years and have not yet drawn any retirement

benefits.

Top-up payments can be made for the first time in the 2026 tax year for contribution gaps from 2025. The ordinary pillar 3a maximum amount for the current year must first be paid in before previous contribution gaps can be closed.

Like regular payments, top-up payments are fully deductible from taxable income. If you have already paid in the maximum annual pillar 3a amount, you can make an additional purchase to close contribution gaps from 2025.

Top-up 3a pillar payments

Find out more about pillar 3a top-up payments here.

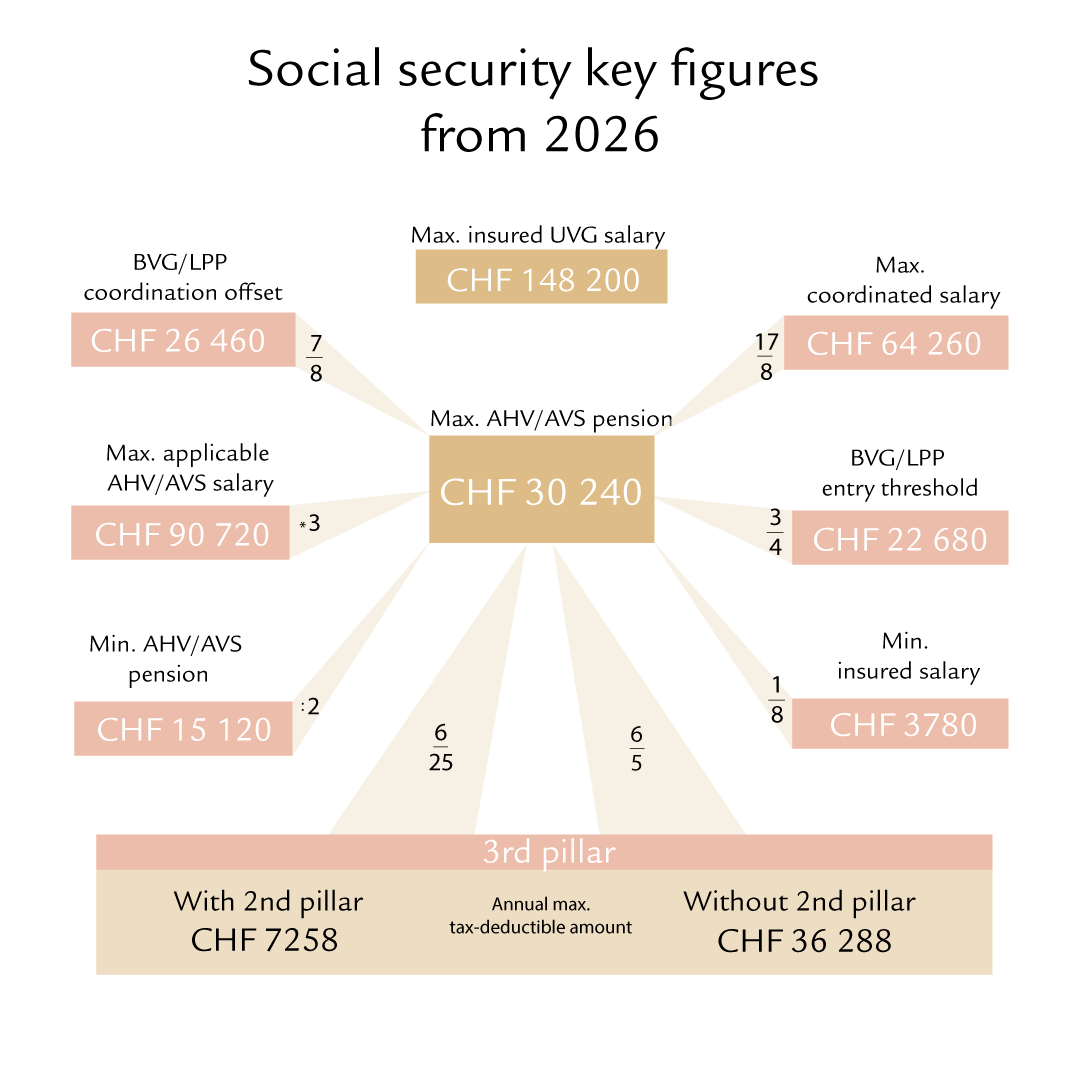

Maximum pillar3a contribution

In 2026, the maximum pillar 3a contribution will remain the same as in 2025.

If you are affiliated to a pension fund, you can pay in up to CHF 7258. Those who do not belong to a pension fund can pay in up to 20% of their earned income, up to a maximum of CHF 36 288.

- People with a pension fund

Maximum amount: CHF 7258 - People without a pension fund (self-employed, part-time workers, etc.)

Maximum amount: 20% of earned income, up to a maximum of CHF 36 288

13th AHV/AVS pension

The 13th AHV/AVS pension will be introduced in 2026. It will be paid in December as an additional month’s pension. This change is the result of the popular initiative “For a better life in old age (13th AHV/AVS pension)”, which was adopted by the Swiss electorate in March 2024. No cost-of-living adjustment is planned for the AHV/AVS in 2026.

Change in the reference age for women

Having entered into force in 2024, the AHV/AVS 21 reform will gradually raise the reference age for women and standardise it at 65 for both men and women.

The following rules will apply from 2026: the reference age for women born in 1962 is being raised by six months. For example, a woman born in March 1962 now has to work for another six months, i.e. until the end of September, before she reaches the reference age. This increase will continue until 2028:

- 2027: women born in 1963 reach the reference age at 64 years and 9 months.

- 2028: the reference age will be raised to 65 for all women born in 1964.

The AHV/AVS 21 reform provides for the 1st They will benefit from either a lifelong pension supplement if they do not draw their retirement pension early or a lower reduction rate if they do draw their retirement pension early.

Social security key figures

The amount of the maximum AHV/AVS pension, the BVG/LPP entry threshold, the coordination offset and the maximum pillar 3a contributions will remain the same in 2026 as in 2025.

Here is an overview:

Increase insurvivors’ and disability pensions

From 1 January 2026, survivors’ and disability pensions that commenced in 2022 or later under the mandatory occupational pension scheme (2nd pillar) will be adjusted to the cost of living. The adjustment rate is 2.7%.

The change is based on inflation between 2022 and 2025 and will apply until the reference age. For pensions that commenced before 2022, the next adjustment will take place on 1 January 2027 at the earliest, as soon as AHV/AVS pensions are increased again.

There is no obligation to make adjustments for survivors’ and disability pensions exceeding the BVG minimum or for retirement pensions; the employee benefits institutions decide themselves in accordance with their financial resources.

Insurance

Increase in health insurance premiums

In 2026, premiums for basic insurance in Switzerland will increase by an average of 4.4%. Premium adjustments may be higher or lower depending on the canton.

Reasons for the increase

- Rising healthcare costs: new treatments, higher demand for medical services and tariff increases

- Demographic change: an older population on average leads to an increased need for medical care.

Ways to reduce premiums

- Switching model or provider: alternative insurance models (switch from free choice of doctor to family doctor model or tele-model) or a change of provider can reduce monthly costs.

- Increase in deductible: a higher deductible can reduce premium costs.

Tip: compare offers early in order to find the right model for your individual needs and avoid unnecessary costs. Here you will find everything you need to know about health insurance in Switzerland.

Taxes andfinances

Interest rate cut for consumer loans

From 1 January 2026, the maximum interest rate for consumer loans will be reduced by 1 percentage point. A maximum interest rate of 10% for cash loans and 12% for overdrafts (e.g. credit cards) will apply. The cut will be carried out in accordance with the calculation formula set out in the Ordinance to the Consumer Loan Act (VKKG/OLCC), as interest rates have fallen further. Intended to guarantee customer protection, the maximum interest rate is thus at its lowest possible level.

Would you like a consultation?

We provide comprehensive advice tailored to your goals at a place of your choice.