Missing pillar 3a contributions can now be paid retroactively for up to ten years. This allows you not only to benefit from tax advantages, but also to close any pension gaps. We provide an overview of how top-up payments to pillar 3a work and what you need to bear in mind.

In 2024, the Federal Council decided that pillar 3a top-up payments would be possible in future. From 2026, people in employment will be able to make retroactive payments into their pillar 3a for 2025 and subsequent years if the maximum annual amount has not been paid in.

What are the advantages of making top-up paymentsinto my pillar 3a?

Making a pillar 3a purchase offers several advantages. As with regular deposits, subsequent contributions can also be deducted from your taxable income. This will enable you to save on taxes in the year you make the payment.

At the same time, top-up payments offer flexibility: if you are unable to fully cover the maximum amount in a given year, you will have the opportunity to do so in subsequent years, allowing you to close any pension gaps.

The retirement capital also grows as additional payments are made, which in the long term gives you greater financial self-determination in retirement. Another plus point is that all your pillar 3a assets remain tax-exempt throughout the entire term.

Would you like a consultation?

Our experts can answer all your questions about pillar 3a.

What do I need to bear in mind when making top-up

payments?

As a general rule, for years in which the maximum amount has not been fully paid into your pillar 3a, retroactive payments can be made for up to ten years afterwards. In addition to the current maximum annual amount, this allows you to supplement any amounts missing from previous years.

This requires you to be / have been entitled to pillar 3a savings both in the year you make the purchase and in the year for which the purchase is being made. In addition, no retirement benefits in accordance with Art. 3, cl. 1 BVV/OPP 3 may have been withdrawn to date.

Validity: the new rule applies to contribution gaps from 2025. From 2026, the amount not fully paid into your pillar 3a in 2025 can be topped up for the first time. Contribution gaps from years prior to 2025, however, can no longer be topped up.

Example: if you do not pay in the maximum amount in 2025, you can top up the difference within the following ten years, i.e. by 2035 at the latest. To do so, the maximum amount that applies to you must have already been fully paid into your pillar 3a in the year in which the top-up payment is made.

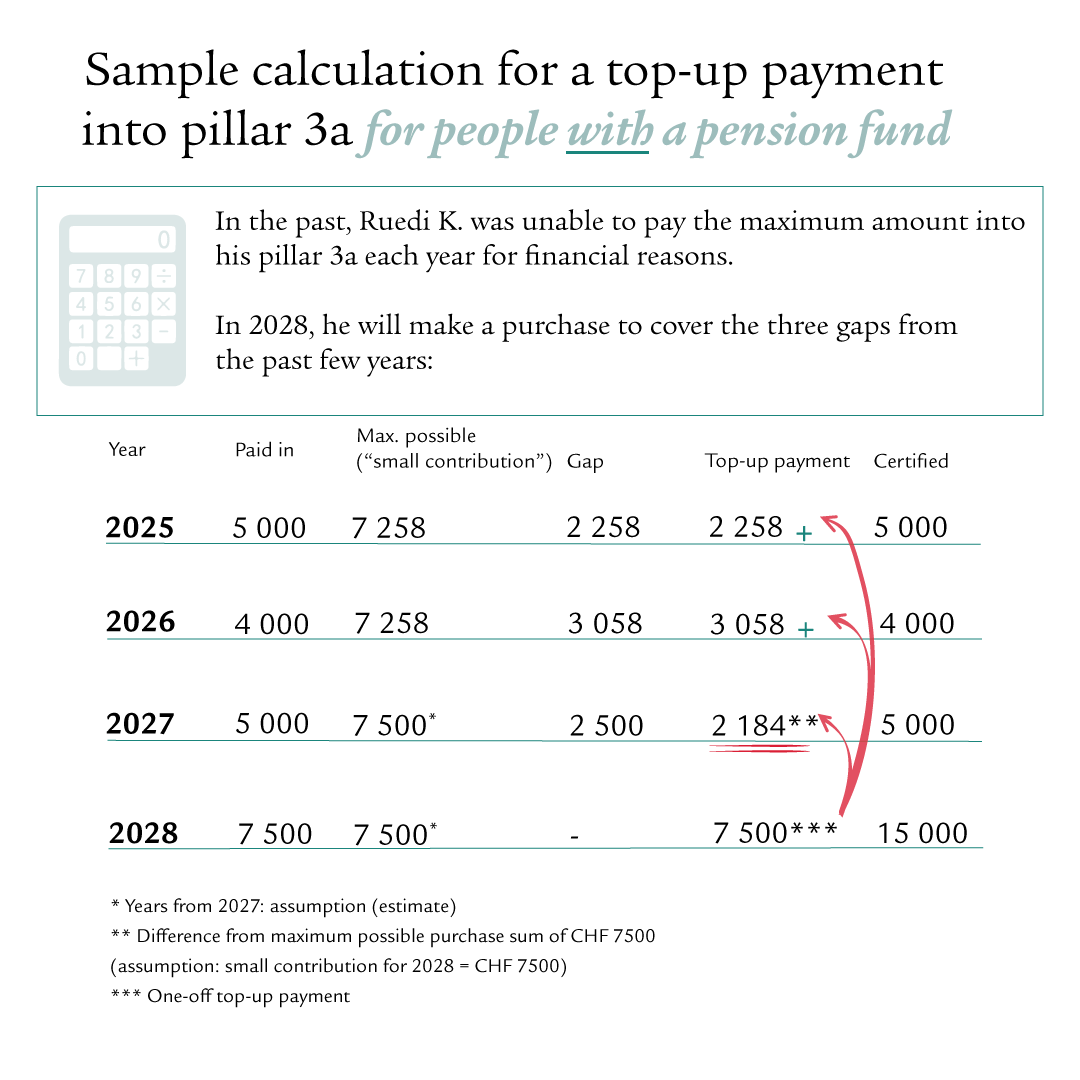

Note the maximum amount: the maximum purchase amount may not exceed the existing contribution gap nor exceed the applicable “small maximum contribution”. In aktuelles-jahr, this amount is abzug-3a. This maximum amount applies to everyone – regardless of whether they are affiliated with a pension fund.

Are top-up pillar 3a payments tax-deductible?

Yes. You can deduct your pillar 3a contributions from your taxable income. If you have already paid in the maximum annual pillar 3a amount, you can make an additional purchase to close contribution gaps (from 2025).

Note the maximum amount: the purchase may not exceed either the existing contribution gap or the so-called “small contribution”. In aktuelles-jahr, this amount is abzug-3a.

Following the purchase, you will receive a statement showing the total amount paid in. This can be deducted from tax in the year in which the top-up payment is made. This reduces your tax burden, while at the same time your retirement capital increases.

How can I make top-up payments into my pillar 3a?

There are clear requirements applicable to pillar 3a top-up payments. First, the standard maximum amount for the current year must have been fully paid in. Only then may any missing contributions from previous years be made – and only for years in which you earned income subject to AHV/AVS contributions.

To be taken into account: only one top-up payment is permitted per contribution gap. However, a single payment can also top up multiple years of outstanding amounts at the same time, provided this does not exceed the applicable maximum amount.

Who can make top-up payments into their pillar3a?

Top-up payments will be possible to cover contribution gaps from 2025 at the earliest and only for people who work in Switzerland, earn an income subject to AHV/AVS contributions and who have not fully paid in the maximum pillar 3a amount in the past ten years.

Advantages for self-employed workerswithout an occupational pension

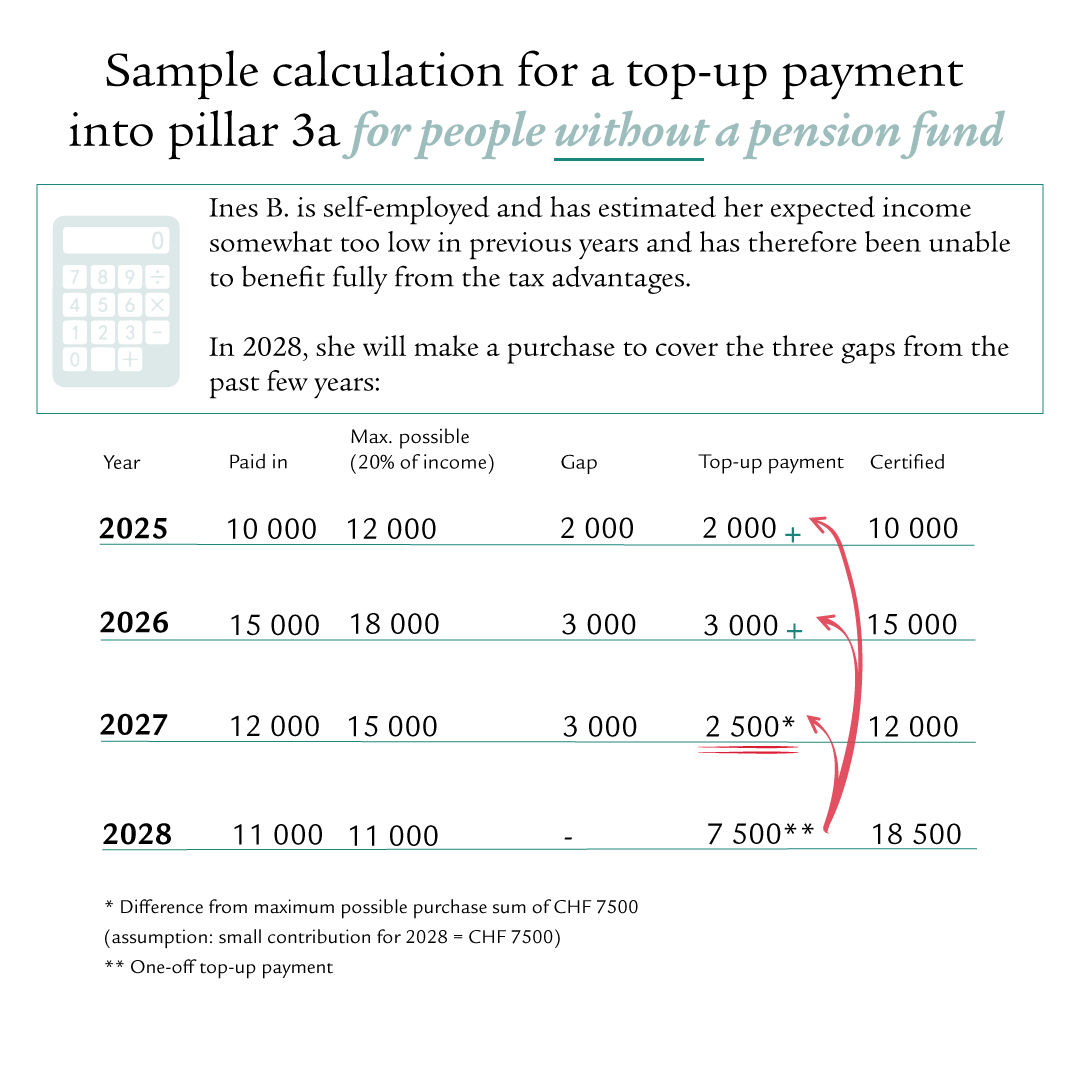

In particular, self-employed people without a pension fund have a clear advantage: by making subsequent payments into their pillar 3a, they can significantly reduce previous tax disadvantages.

As self-employed people have to estimate their annual income in advance, it is often difficult for them to pay in the full maximum amount – and therefore enjoy the full tax benefit. Those who estimated their income too low were unable to make up for the unused tax deduction for previous years.

The new purchase option offers more flexibility and fairness: anyone who confirms in the year of purchase that they have paid in full the individual maximum contribution – i.e. 20% of their expected net income up to a maximum of abzug-3a-selbststaendige (in aktuelles-jahr) – can make retroactive payments for up to ten years in the future. These top-up payments are limited to the actual contribution gaps and must be made in the form of a one-off payment. In addition, the so-called “small contribution”, which currently amounts to abzug-3a (aktuelles-jahr), may not be exceeded.

The ten-year deadline gives them the flexibility to decide in which year they make a top-up payment, meaning they can optimise their tax burden in this particular year. Instead of making purchases to cover individual contribution gaps spread over several years, you can also make up multiple contribution gaps at one time – taking into account the maximum possible purchase amount per year, which corresponds to the pillar 3a smallcontribution”.

The new regulation is particularly advantageous for people who have recently become self-employed. If you did not have enough money to make full use of pillar 3a after becoming self-employed, you will now have the opportunity to top it up at a later date.

Good to know

It is not only the self-employed who can find themselves without a pension fund: even part-time workers with an income below the BVG/LPP entry threshold or with several part-time positions whose combined salaries do not reach this threshold are often not affiliated with a pension fund. They are subject to the same rules as for self-employed peoplewithout a pension fund.

Conversely, there are also self-employed people who are affiliated with a pension fund – the provisions apply to them as they would to employees.

The decisive factor for the maximum permissible contribution to pillar 3a is therefore whether a person is a member of a pension fund, not their professional status.

Would you like a consultation?

Our experts can answer all your questions about pillar 3a.

From when can I make top-up payments into my pillar 3a?

Top-up payments will be possible from 2026 and relate to payments that have been fully or partially missed from 2025. From then on, you will have ten years to make up the gaps. Gaps in pillar 3a prior to 2025 can no longer be filled.

Why is my pillar 3a so important?

Pillar 3a is a key part of your private provisions. It supplements the AHV/AVS and your pension fund and closes any income gaps in old age. Payments are tax-deductible and reduce your tax burden. Pillar 3a also allows assets to be accumulated over the long term, with attractive potential returns and flexibility: under certain circumstances, you can withdraw your assets early, for example to purchase a home or become self-employed.

What happens if you pay too much into your pillar3a?

If you pay more than the legally permitted maximum amount into pillar 3a, you do not benefit from any additional tax advantages. The excess amount is not tax deductible and must be repaid, which causes additional administrative work. It is not possible to offset it against subsequent years.

Would you like a consultation?

Our experts can answer all your questions about pillar 3a.